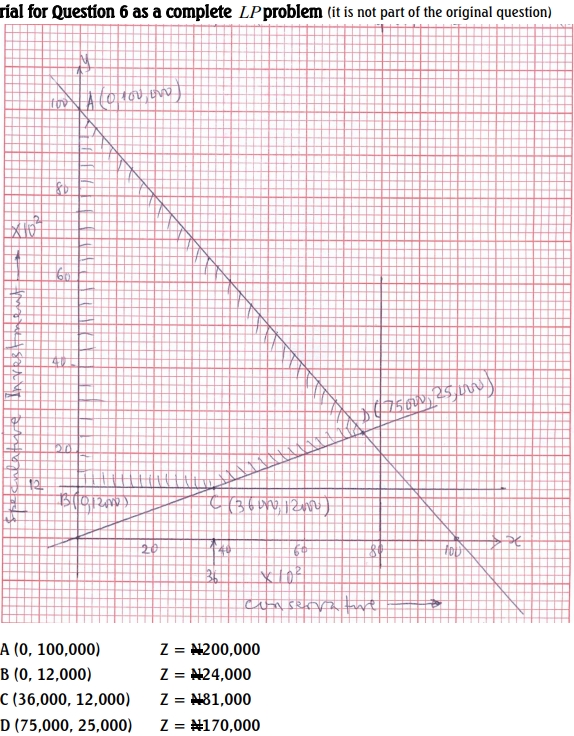

Question

Answer

(a) Type of Operations Research Problem:

The problem described is a Linear Programming Problem (LPP), which aims to optimize (maximize) returns on inventory investments under given constraints. (2 Marks)

(b) Mathematical Formulation:

Let:

- CC: Investment in conservative inventory (in naira)

- SS: Investment in speculative inventory (in naira)

(i) Objective Function:

The objective is to maximize the total return on investments in both conservative and speculative inventories.

Maximize Z=1.6C+2.0S

Where:

- 1.6C : Return on investment in conservative inventory

- 2.0S2 : Return on investment in speculative inventory

(4 Marks)

(ii) Constraint Inequalities:

The constraints can be formulated as follows:

- Total Investment Constraint:

C+S ≤ 100,000The total investment should not exceed N100,000.

- Conservative Investment Constraint:

C ≤ 80,000 The investment in conservative inventory should be at most N80,000.

- Speculative Investment Constraint:

S ≥ 12,000The investment in speculative inventory should be at least N12,000.

- Monetary Policy Regulation:

The investment in speculative inventory should be at most one-third of the investment in conservative inventory.

- Non-negativity Constraints:

C ≥ 0, S ≥ 0(8 Marks)

(iii) Investment Problem:

The investment problem is to determine the values of C and S that maximize the total return (Z), subject to the above constraints. Mathematically:

Maximize Z = 1.6C + 2.0S

- Monetary Policy Regulation:

C+S ≤ 100,000 (available fund constraint)

C ≤ 80,000 (Conservative investment policy constraint

C ≥ 12,000 (Speculative investment policy

C ≤ 1/3 x (monetary policy constraint)

Non negativity/hidden constraint C,S ≥ 0