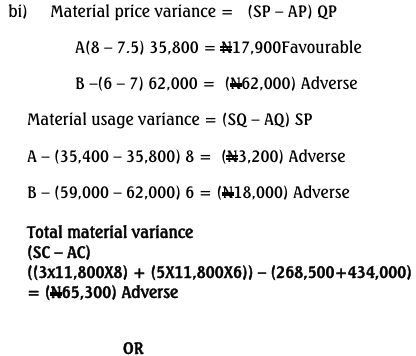

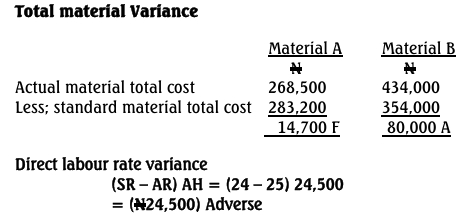

Question

Answer

Material price variance

– Changes in market conditions that cause a general price increase for the

material.

– Failure of the purchasing department to seek most advantageous source

of supply

– Purchase of inferior quality materials bought at lower price

– Shortage of material necessitating buying at higher prices.

Material usage variance

– Careless handling of materials – Purchase of inferior quality materials

– Pilferage

– Changes in quality control requirements

– Changes in method of production

Direct labour rate variance

– Negotiated increase in rates not yet reflected in standard

– Unexpected overtime

– Use of a wrong standard rate for operations performed by workers paid with different rates

– Assignment of skilled labour to work normally performed by unskilled

labour.