Question

Answer

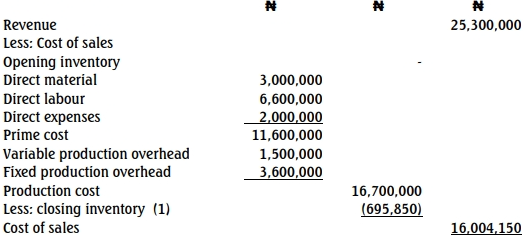

a. Absorption costing

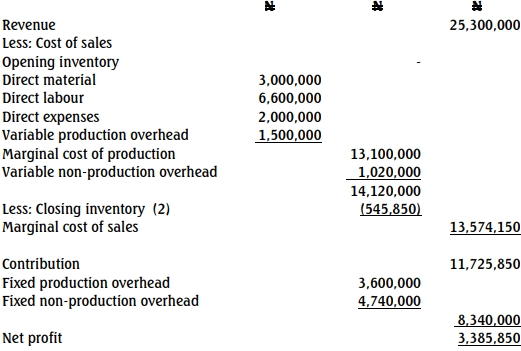

b. Marginal costing

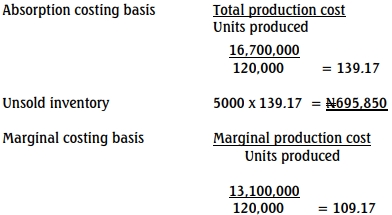

c. Closing inventory valuation

![]()

d. Explanation of Differences between Absorption and Marginal Costing

The difference is as a result of the difference in the closing stock.