Question

Answer

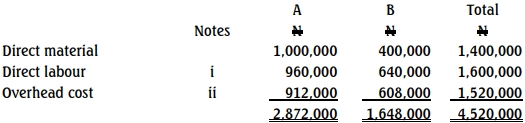

a) LADECK NIGERIA LIMITED

TRADITIONAL ABSORPTION COSTING

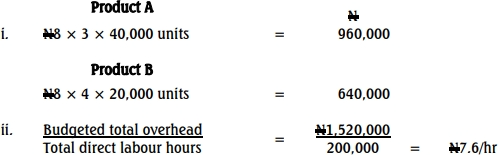

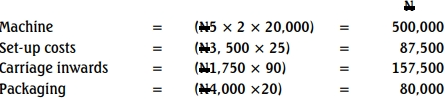

Workings

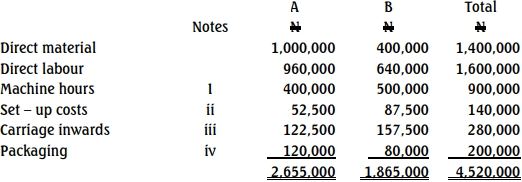

b) Production Costs using ABC Approach

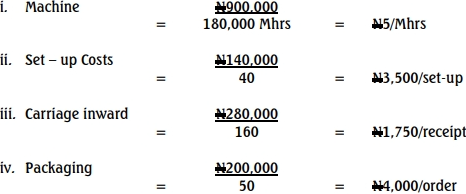

Workings

PRODUCTS A

PRODUCTS B

a) LADECK NIGERIA LIMITED

TRADITIONAL ABSORPTION COSTING

Workings

b) Production Costs using ABC Approach

Workings

PRODUCTS A

PRODUCTS B