Question

Answer

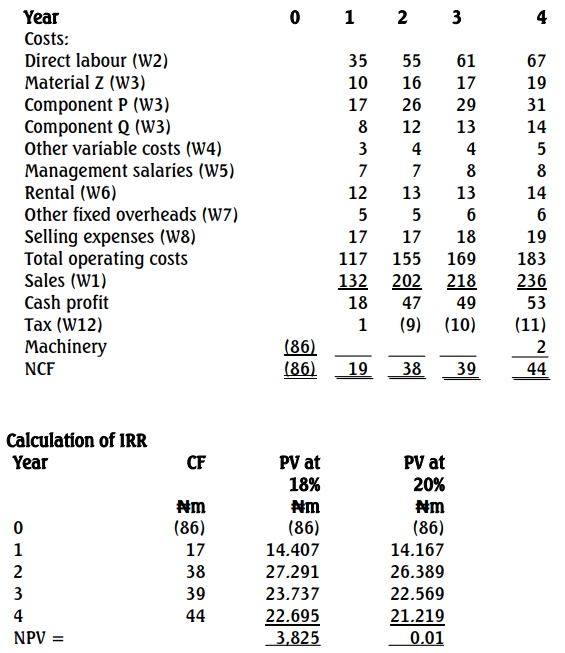

a. Project‘s Cash Flows (₦ million)

At 20%, the NPV is zero and therefore the IRR is approximately 20%.

Working notes

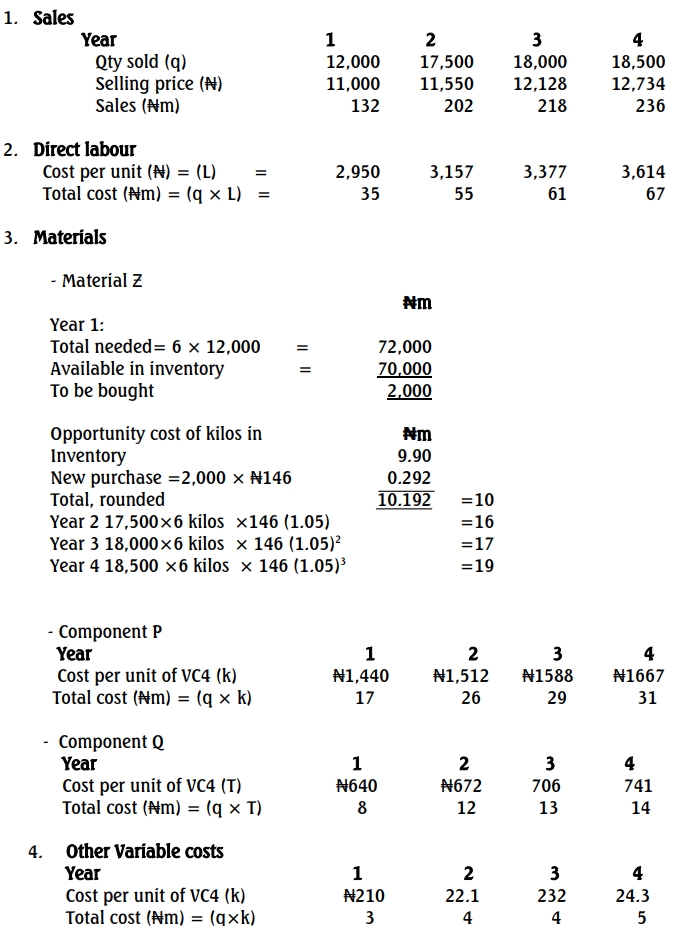

5. Management salaries

Only incremental management salaries are relevant, the two new managers plus the replacement deputy manager, costing total ₦6,700,000

(₦5,000,000 + ₦1,700,000) in year 1, increasing by 7% per year

subsequently.

6. Rental

The opportunity rental of ₦12 million is the relevant cost in year 1,

increasing by 5% per year subsequently.

7. Other fixed overhead

The only relevant cost is the amount given (₦7millon) less the apportioned building rates of ₦2m (i.e. ₦5 million in year 1). This will rise by 5% per year subsequently.

8. Selling expenses

These will be ₦16.60 million (rounded to ₦17 million in year 1 and then

rising by 5% per year subsequently.

9. Interest cost

This is ignored as the cost of finance is encompassed within the discount

rate.

10. Apportioned head office costs do not involve cash flow and therefore

irrelevant.

11. Advertisement cost

No incremental cash flow is involved and therefore irrelevant.

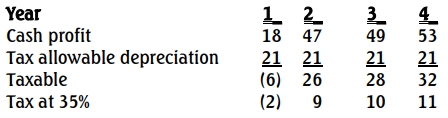

12. Tax

b(i). Explanation of Asset Beta vs. Equity Beta

An asset beta reflects the company’s systematic business risk and is the weighted average of the beta of equity and debt, accounting for tax effects if relevant. It captures only the inherent business risk, excluding the financial risk associated with a company’s capital structure. Thus, it measures the company’s exposure to market risk that cannot be diversified away, based solely on the assets.

On the other hand, an equity beta accounts for both systematic business risk and financial risk, as it represents the risk taken on by equity holders in a leveraged company. This beta includes the impact of financial leverage (the proportion of debt financing) on the overall risk profile.

Using the Capital Asset Pricing Model (CAPM), the required return (RiR_i) is calculated as:

![]()

b(ii). Analysis of the Project’s Acceptance Based on Required Return and Other Considerations

Given that the internal rate of return (IRR) for the project is 19%, which exceeds the required return of 16.4%, it initially appears that the project is financially viable. However, other considerations should be evaluated:

- Cost of Equity vs. WACC: The required return calculated (16.4%) reflects the cost of equity alone, which is suitable only if the company is entirely equity-financed. However, the project is expected to be funded via a bank loan, introducing financial leverage and financial risk. Thus, the appropriate metric for evaluation should be the weighted average cost of capital (WACC), which accounts for both equity and debt financing costs.

- Beta of Project vs. Beta of Company: The beta used (1.2) is based on the company’s overall risk profile, not the specific risk of the new project. If the new project belongs to a different risk class, both in terms of business and financial risk, then the current beta may not accurately represent the project’s risk, making the required return potentially inappropriate.

- Level of Diversification: If the company lacks sufficient diversification, unsystematic risk may still be a factor for the company. In such a case, management may need to account for some level of unsystematic risk, as the beta derived from CAPM assumes only systematic risk.

- Problems with CAPM: The CAPM model, while widely used, has both theoretical limitations and practical issues in terms of data collection. As a result, the calculated required rate of return might not perfectly reflect the true return needed for this project, leading to potential misalignment with the actual cost of capital.

- Non-Financial Factors: Non-financial considerations could also significantly impact the investment decision. Factors such as strategic positioning, brand value, environmental impact, and long-term company goals may justify undertaking the project even if financial metrics alone suggest otherwise.

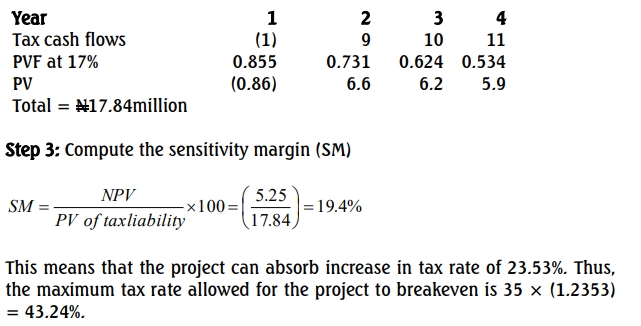

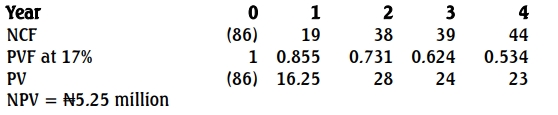

c) Step 1: Compute the NPV of the project, using discount rate of 17%.

Step 2: Calculate, at 17%, the present value of tax liability.