Question

Answer

a. Reasons why a firm might reasonably choose not to hedge its exposure to exchange rate risk include:

- Costs (direct and implicit);

- Materiality of the exposure;

- Attitude to risk – the firm may prefer to leave the upside potential open;

- Portfolio effect; and

- If shareholdings are fully diversified, shareholders’ exposure to systematic risk remains unaffected, providing no hedging benefit.

Alternative 1 – Do not hedge

If the company does not hedge, the receivables will be converted at the spot rates in three months.

Alternative 2 – Forward Contract

Under this option, the receivables are converted at the agreed forward rate of 1.1508, regardless of future spot rates.

- Amount due:

70,000,000 Kudi/1.1508 Kudi/N=N60,827,251

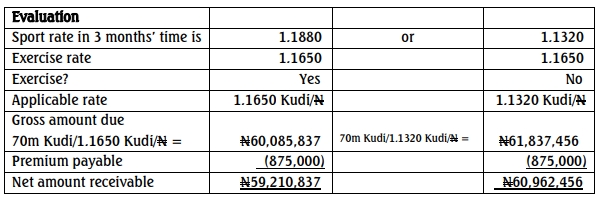

Alternative 3 – Currency Option

As Alpha Plc. is hedging a foreign asset, a put option (the right to sell) is needed. The premium cost is N1.25 per 100 Kudi:

- Premium payable:

(70,000,000 Kudi / 100) ×N1.25=N875,000

c. Methods to reduce foreign exchange risk without using financial contracts:

- Choice of invoice currency;

- Matching payments and receipts in the same currency;

- Matching assets and liabilities (e.g., using overdraft borrowing in the same currency as receivables);

- Leading and lagging payments; and

- Maintaining currency accounts