Question

Answer

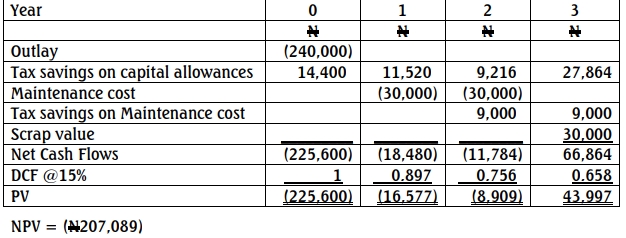

(a)

3-Year Life

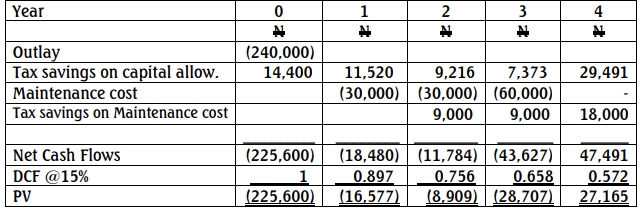

4-Year Life

Summary:

Recommendation: A four-year life is marginally more economical and should therefore be adopted.

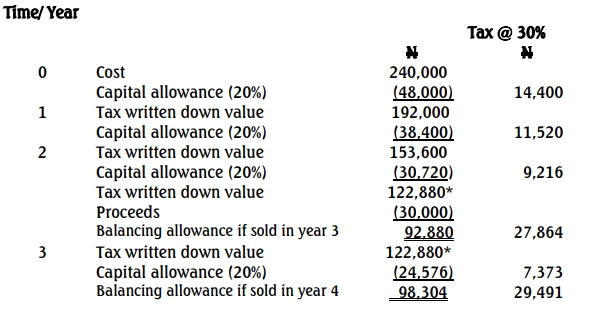

WORKINGS

*Represents tax written down value if machine is not sold at the end of the 3rd year.

b. Relevant Issues

- Price Changes: The analysis in (a) ignores price changes of all descriptions as a change in the price of a new machine could easily alter the conclusion. The same applies to all input factors.

- Machine Replacement Assumptions: The approach assumes that replacement will occur with an identical machine. The machine may become technologically outdated, or the company may no longer need such a machine. Realistically, not many assets are replaced with identical models continually.

- Timing of Cash Outflows: Payments every fourth year might pose fewer cash flow challenges than payments every third year.