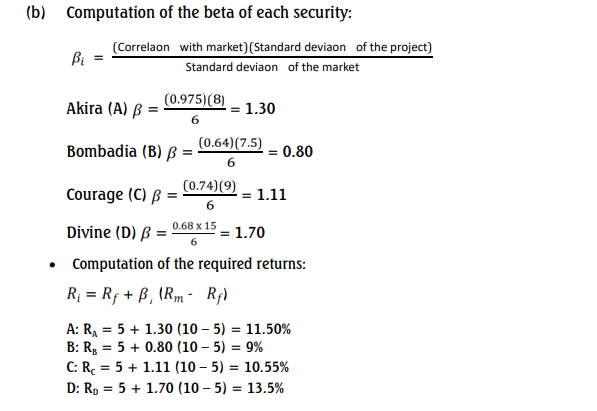

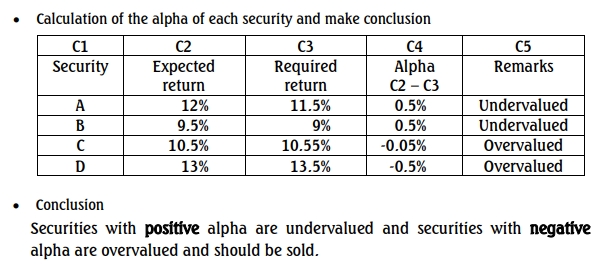

Question

Answer

a Basic Assumptions of CAPM

- Investors are Rational and Risk-Averse: Investors aim to maximize returns for a given level of risk or minimize risk for a given level of return.

- Markets are Perfectly Competitive: No investor can influence market prices. There are no transaction costs or taxes.

- Homogeneous Expectations: All investors have the same expectations of risk and return for a given security.

- Single Period Horizon: All investors plan for the same single period investment horizon.

- Free Borrowing and Lending: Investors can borrow or lend unlimited funds at a risk-free rate.

- Risk is Measured by Variance: Risk of securities is determined by the variance or standard deviation of returns.

(6 Marks)