Question

Tinko Plc (TP) repairs and maintains heavy-duty trucks, with workshops in Nigeria and several other African countries. TP is considering an expansion project in response to the government’s recent policy aimed at encouraging mechanized farming through the “Graduates Back To Land (GBTL)” program, which will likely increase demand for heavy-duty machinery.

Below are extracts from the most recent Statement of Financial Position of TP:

| Item | ₦’million |

|---|---|

| Share capital | 200 |

| Reserves | 320 |

| Non-current liabilities | 760 |

| Current liabilities | 60 |

| Total | 1,340 |

TP’s Free Cash Flows to Equity (FCFE) is currently estimated at ₦153 million, and it is expected to grow at 2.5% per annum indefinitely. The equity shareholders require a return of 11%.

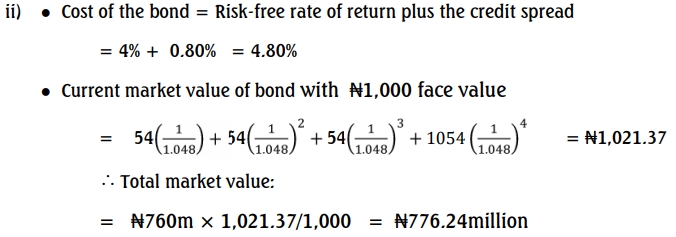

The non-current liabilities consist entirely of bonds redeemable in four years at par with a coupon rate of 5.4%. The debt is rated BB, and the credit spread on BB-rated debt is 80 basis points above the risk-free rate.

In light of the GBTL program, TP is contemplating entry into the mechanized farming support industry through a four-year project, recognizing that after four years, competition may intensify significantly.

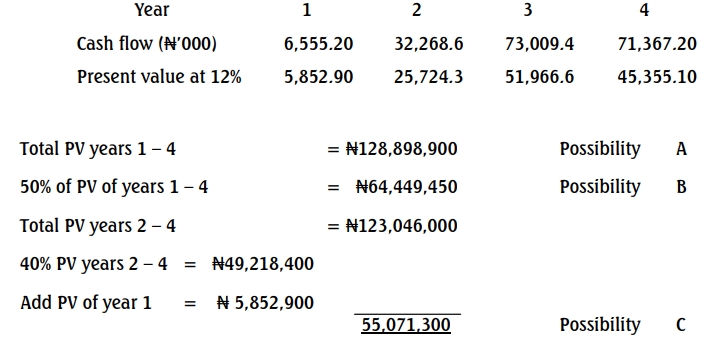

The project requires an initial investment of ₦84 million and is expected to generate the following after-tax cash flows:

Additional Information:

- Scenario Adjustments:

- There is a 25% probability that the GBTL program will not grow as expected in the first year. If this occurs, the present value of the project’s cash flows over its four-year life will be 50% of the original estimates.

- If the GBTL program grows as expected in the first year, there is still a 20% probability that growth will slow in subsequent years, reducing the present value of cash flows to 40% of the original estimates for those years.

- Sale Option: Feedwell Limited (FL) has offered ₦100 million to buy the project from TP at the start of the second year. TP is evaluating if this option adds strategic value to the project.

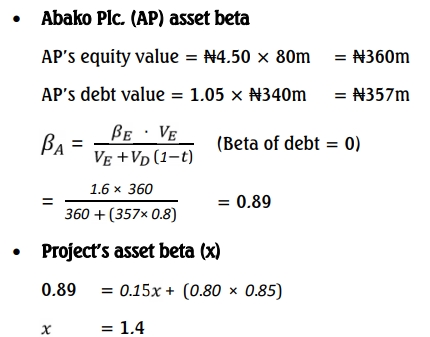

- Abako Plc, a comparable company, operates primarily in non-agricultural services, similar to TP, and has an equity beta of 1.6. Abako derives approximately 80% of its revenues from services outside agriculture, with an asset beta of 0.80. Abako’s capital structure consists of 80 million shares trading at ₦4.50 per share and debt of ₦340 million.

- The debt is trading at ₦1,050 per ₦1,000 with a zero debt beta.

- Risk-free rate: 4%; Market risk premium: 6%; Corporate tax rate: 20%.

Requirements: a. Calculate TP’s current total market value of:

- i. Equity (3 Marks)

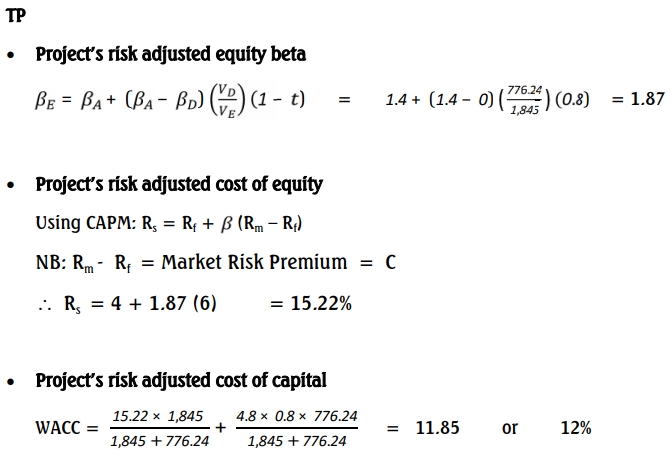

- ii. Bonds (4 Marks) b. Determine the risk-adjusted cost of capital for the new project (to the nearest percent) (10 Marks) c. Estimate the value of the project:

- i. Without factoring in the potential strategic value or synergy from the project (5 Marks)

- ii. With FL’s offer, assuming it reflects the market’s view of the project’s value (5 Marks) d. Clearly state the assumptions made in your calculations (3 Marks)

Answer

a) i) Current value of equity

Using FCFE model, the current value of equity

b) Calculation of project’s risk-adjusted cost of capital:

The cost of capital should reflect the systematic business risk of the project. This should be calculated from the information given about AP.

c) Where WACC = Weighted Average Cost of Capital

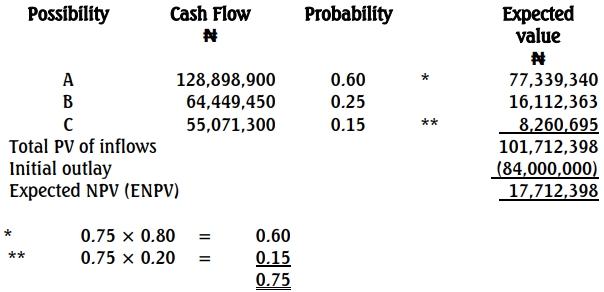

i) Value of the project without the offer from Feedwell Limited (FL)

Summary

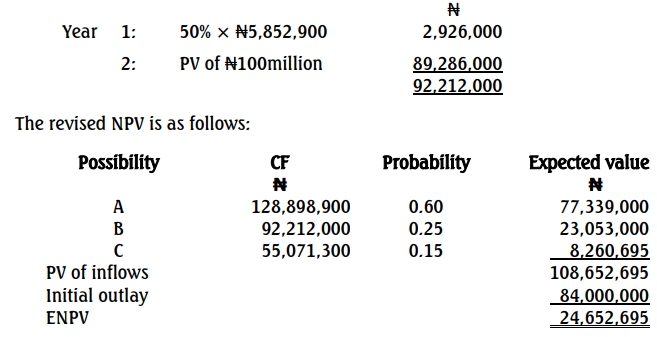

ii) Expected value of the project with the offer from Feedwell Limited (FL)

PV of ₦100m = 100,000,000/1.12 = ₦89,286,000

If the Graduate Back To Land (GBTL) does not grow as expected in the first year, then it is more beneficial for Tinko Plc. to exercise the offer made by FL, given that FL’s offer of ₦89.27 million (PV of ₦100 million) is greater than the PV of years two to four cash flows, that is, 50% × ₦(25.72m + 51.97m + 45.36m) = ₦61.53m for that possible outcome.

This figure is then incorporated into the expected net present value calculations. Thus, for possible outcome B:

Note

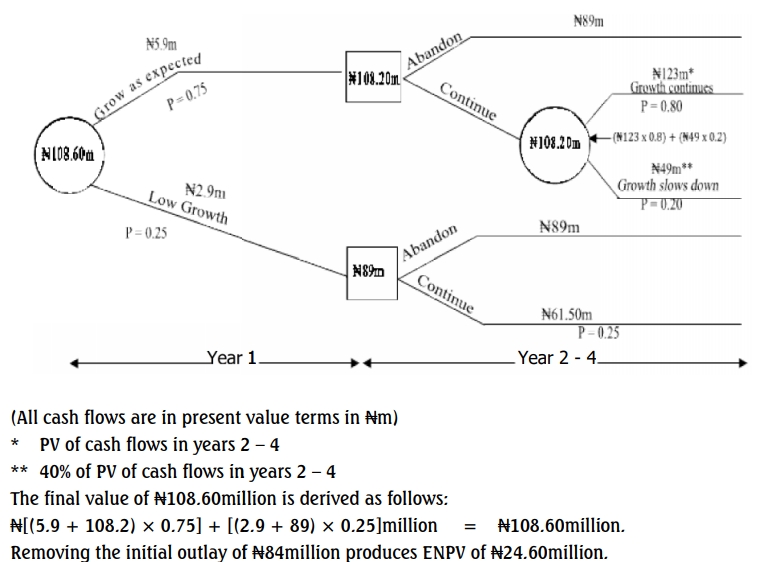

The analysis above is the intended solution. Another method is to make use of decision tree. Alhough, a longer process, it is included here for educational purposes.

(d) Key Assumptions

- Capital Structure Stability: It is assumed that the capital structure of TP will remain relatively stable and will not be significantly affected by the introduction of the new project. Given that the project’s initial investment is minor compared to the overall value of TP, this assumption is considered reasonable.

- Uncertainty in Outcomes: In reality, the project may face multiple possible outcomes beyond those presented, with uncertain financial impacts. The Black-Scholes Option Pricing Model could serve as an alternative, potentially providing a more precise method for valuing the project’s flexibility and accounting for this uncertainty.

- Reliance on Expected Cash Inflows: It is assumed with certainty that TP can depend on receiving the ₦100 million payment from FL at the start of the second year, which is crucial for cash flow projections.

- Accuracy of Financial Inputs: The analysis assumes that all provided figures, including the beta, growth rates, risk-adjusted cost of capital, and probability estimates, are accurate and reflect realistic expectations.