Question

Answer

- Reasons Yield May Not Be Realized:

- Timely receipt of cash flows: Delays in receiving coupons and redemption values reduce the effective yield due to time value effects.

- Reinvestment risk: If coupons are reinvested at rates below 5.44%, the actual yield will fall; higher reinvestment rates would increase yield.

- Price risk: Selling the bond before maturity could lead to capital gains or losses, altering the realized yield.

- Price Expectation After One Year

- Since this is a premium bond, the price is expected to decrease over time, approaching face value by maturity. With stable interest rates, the bond price will likely fall by the end of Year 1.

The bond is a premium bond, meaning its current price is above its face value. Generally, the price of a premium bond declines as it approaches maturity (assuming interest rates remain constant) because at maturity, the bond’s market value and face value must converge – as the face value will be the final amount paid. Therefore, at the end of Year 1, the bond’s market value is expected to be lower than its current market value.

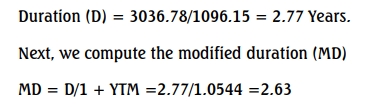

(b)(iii) Modified Duration of the Bond

Step 1: Calculate Duration of the Bond

| Year (n) | Cash Flow (₦) | Present Value (at 5.44%) (₦) | PV × n (₦) |

|---|---|---|---|

| 1 | 90 | 85.36 | 85.36 |

| 2 | 90 | 80.95 | 161.90 |

| 3 | 1090 | 929.84 | 2,789.52 |

| Total | 1096.15 | 3036.78 |

Interpretation of Modified Duration: Modified duration measures the sensitivity of a bond’s price to a 1% (100 basis points) change in interest rates. For this bond, a 1% increase in interest rates would cause the bond’s price to decrease by approximately 5.44%, and conversely, a 1% decrease in interest rates would cause the bond’s price to increase by around 5.44%.

Limitations of Modified Duration: Modified duration is a linear approximation and does not fully capture the bond’s price convexity. Key limitations include:

- Convexity: Modified duration does not account for the bond’s convexity, which is influenced by factors like maturity date, coupon amounts, and call/put options.

- Conditions for Accurate Use:

- Assumes a flat yield curve.

- Works best for small changes in interest rates.

- Assumes a parallel shift in the yield curve.

- Assumes an instantaneous change in interest rates.

These limitations mean that while modified duration is useful for estimating price sensitivity, it is most accurate under specific, stable conditions and may not reflect actual price changes in volatile or non-parallel interest rate shifts.