Question

KK, a company quoted on the Stock Exchange, has cash balance of ₦230 million which are currently invested in short-term money market deposits. The cash is intended to be used primarily for strategic acquisitions, and the company has formed an acquisition committee with a remit to identify possible acquisition targets. The committee has suggested the purchase of ZL, a company in a different industry that is quoted on the AIM (Alternative Investment Market). Although ZL is quoted, approximately 50% of its shares are still owned by three directors. These directors have stated that they might be prepared to recommend the sale of ZL, but they consider that its shares are worth ₦220 million in total.

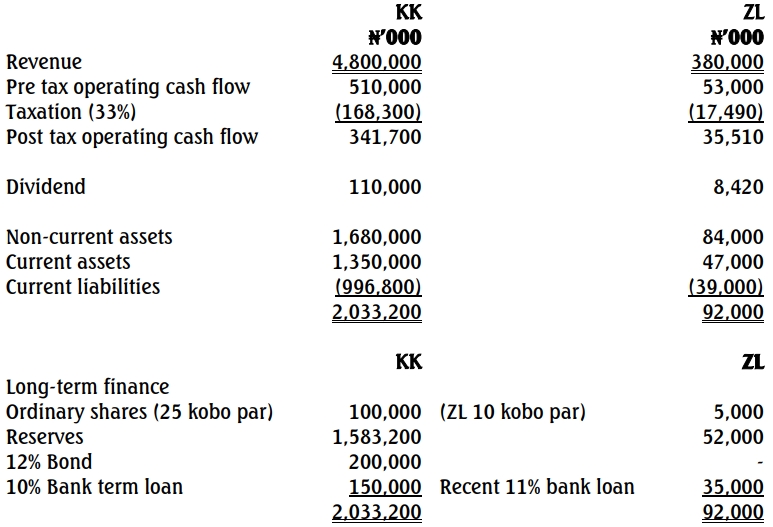

Summarised financial data:

Economic data:

- Risk-free rate of return: 6% p.a.

- Market return: 14% p.a.

- Inflation rate: 2.4% p.a., expected to remain stable.

Expected effects of the acquisition:

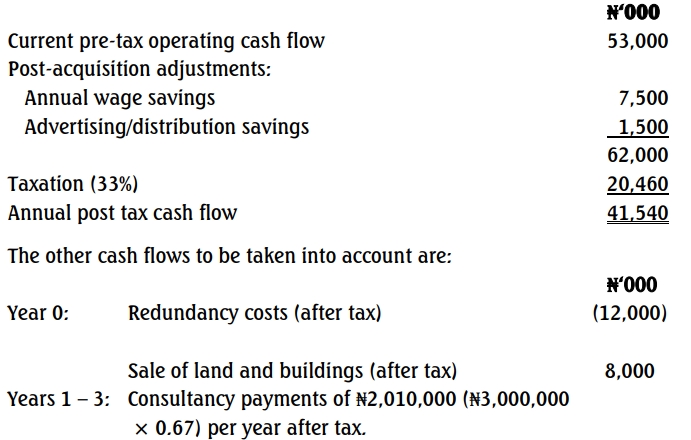

- 50 employees of ZL would immediately be made redundant at an after-tax cost of ₦12 million. Pre-tax annual wage savings are expected to be ₦7.50 million (at current prices) for the foreseeable future.

- Some land and buildings of ZL would be sold for ₦8 million (after tax).

- Pre-tax advertising and distribution savings of ₦1.50 million per year (at current prices) would be possible.

- The three existing directors of ZL would each be paid ₦1 million per year for three years for consultancy services. This amount would not increase with inflation.

Required:

a. Calculate the value of ZL based upon:

i. The use of comparative P/E ratios (3 Marks)

ii. The dividend valuation model (4 Marks)

iii. The present value of relevant operating cash flows over a 10-year period (10 Marks)

iv. Provide an evaluation of each of the three valuation methods in (i) to (iii) above. (7 Marks)

v. Recommend whether KK should go ahead with the offer for ZL. (2 Marks)

Answer

a) Valuation Methods for ZL

i) Valuation Using Comparative P/E Ratios

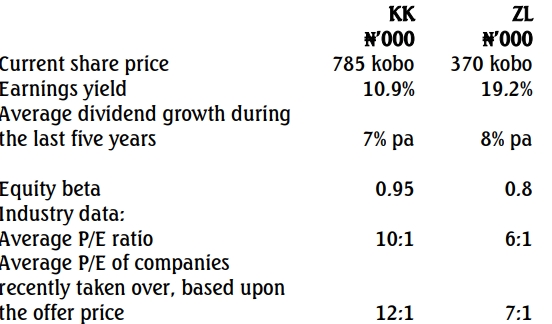

Since ZL operates in a different industry, the comparative P/E ratio valuation must be based upon the average P/E ratios in that industry. The P/E ratio of 7:1 will therefore be used.

Calculation:

- Current share price = 370 kobo

- Earnings yield = 19.2%

- Earnings per share = 71.04 kobo (370 × 19.2%)

- Price per share = 497.28 kobo (71.04 × 7)

- Value of ZL = ₦248.64m (₦4.9728 × 50m shares)

Issues with Calculations:

- The approach is based on historical performance and doesn’t consider the impact of the takeover or current earnings projections.

- Comparability of companies is a challenge; it’s unclear if the companies used for the P/E ratio are similar to ZL. Adjustments may be required for ZL’s unique situation.

ii) Dividend valuation model

The dividend valuation method (including growth) for share valuation is:

P0 =d0(1 + g)/Ke − g

In the case of ZL:

d0 = ₦8,420,000

g = 8%, assuming that this rate of dividend growth will continue

Ke = can be estimated using the Capital Asset Pricing Model CAPM :

E (ri) = R𝑓 + βi(E (rm) − Rf)

Where E(ri ) = cost of equity

R𝑓 = risk free rate of return (6%)

βi = beta factor (0.8)

E (rm) = market rate of return (14%)

E (ri) = 6% + 0.8(14% – 6%) = 12.4%

P = ₦8,420,000 (1 + 0.08)/ (0.124 − 0.08) = ₦206.67m

Weakness of DVM:

- Relies on historical growth rates, which may not reflect future performance, especially post-acquisition.

- Attempts to relate share price to future earnings, offering a more realistic valuation than P/E ratios.

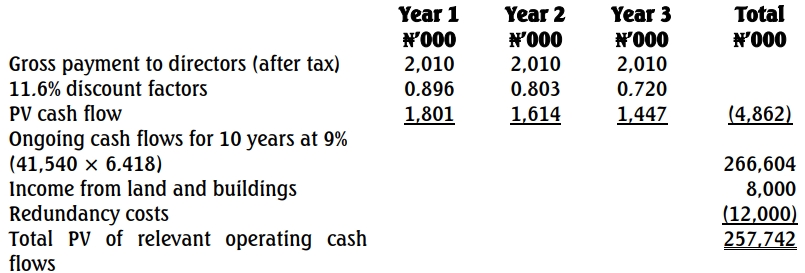

iii) Operating cashflows

The first stage is to estimate what the operating cash flows will be following the acquisition.

Discount rate

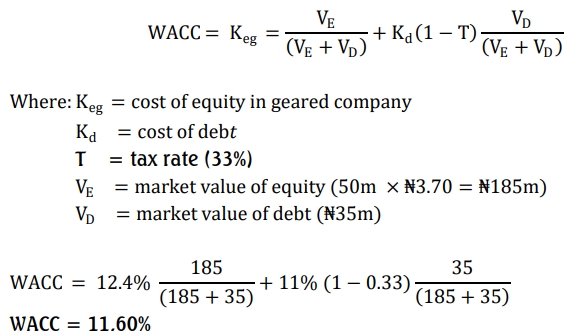

The discount rate used will be the existing weighted average cost of capital (WACC) for ZL, although it must be recognised that this could be different after the acquisition since KK is a much larger company and its shares are quoted on the main market rather than the AIM. The cost of equity has already been calculated above as 12.4%, and the cost of debt is 11% as per the statement of financial position. The following expression will be used.

This discount rate has been calculated on the basis of market values, and

therefore, will incorporate inflation. The cash flows (with the exception of the consultancy fees) all exclude inflation and therefore, either the nominal discount rate that has been calculated must be adjusted to the real rate, or the cash flows must be adjusted to include inflation.

If we adjust the discount rate to exclude the expected 2.4% rate of inflation: 1.116 ÷ 1.024 = 1.0898, i.e. the real discount rate to be used is 8.98%, say 9.0%.

PV of cash flow

The present value of the cash flows can now be found.

Problems with calculations

Although this is theoretically the best method of valuation to use, the

calculations are in reality quite crude. Any likely changes in the pattern of the cash flows following the acquisition are ignored, as are any strategic plans that the company may have for such a long time frame. Ten years is a long period over which to estimate cash flows, inflation rates and discount rates, and there will inevitably be a large margin for error in the figures.

End of period

In addition, the question of what happens at the end of the ten year period is not addressed. Is there an appropriate terminal value that could be used in the calculations to reflect the ongoing value of ZL as a business?

v) Comparison with offer price

Two of the valuation methods used, including the present value of the

operating cash flows (which is possibly the best of the three approaches)

give a valuation greater than the proposed offer price of ₦220m. If KK can successfully complete negotiations at this price, and if the acquisition of ZL would be in line with KK‟s long-term strategic objectives, then it is recommended that the offer should go ahead.