Question

Answer

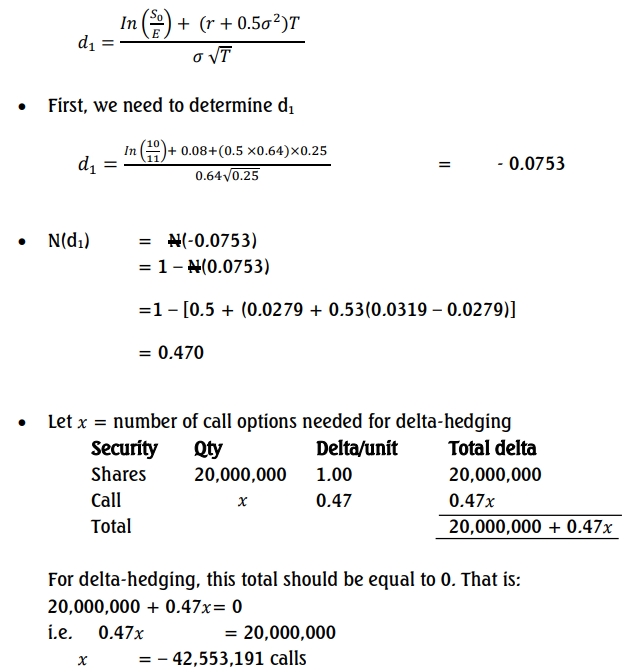

a) The Black – Scholes Option Pricing Model formula given as

Thus, the bank needs to sell 42,553,191 calls for delta-hedging.

a) The Black – Scholes Option Pricing Model formula given as

Thus, the bank needs to sell 42,553,191 calls for delta-hedging.