Question

Answer

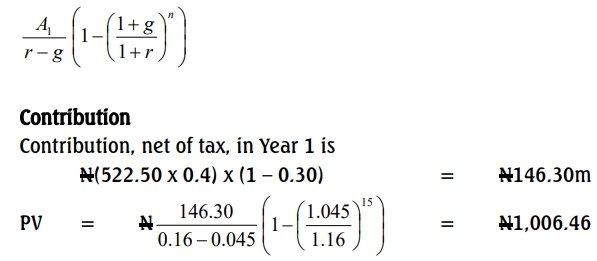

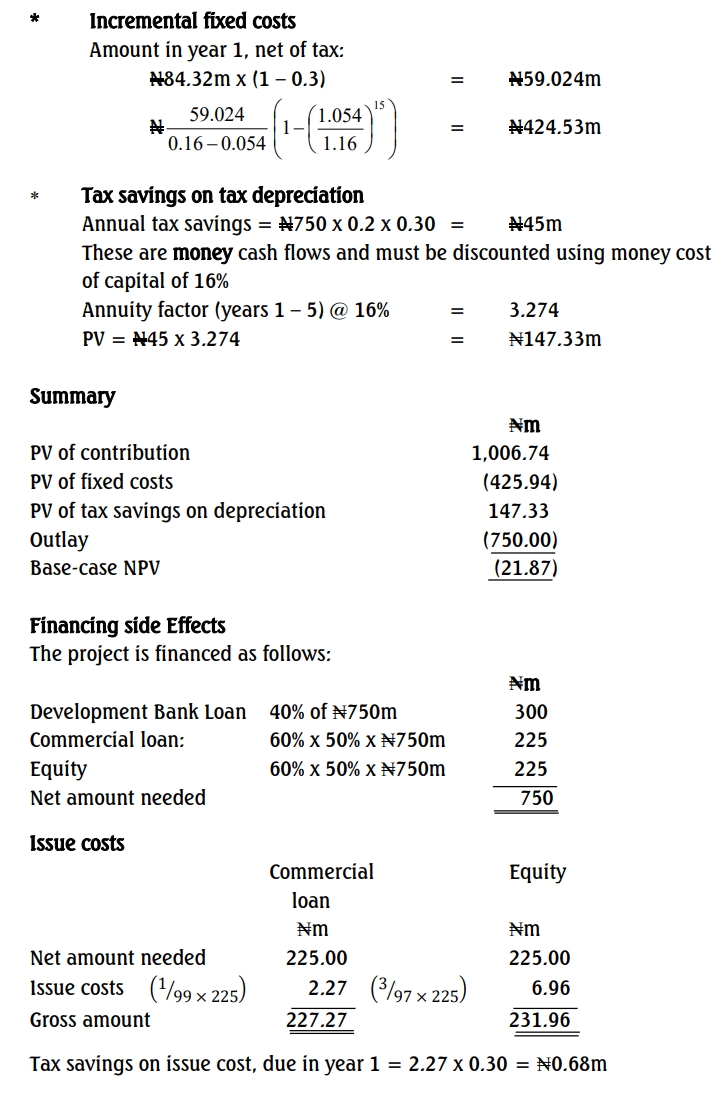

Growing annuity can be used to calculate the present value of each of the items involving growth (inflation). As given in the formula sheet, the present value of growing annuity is given by:

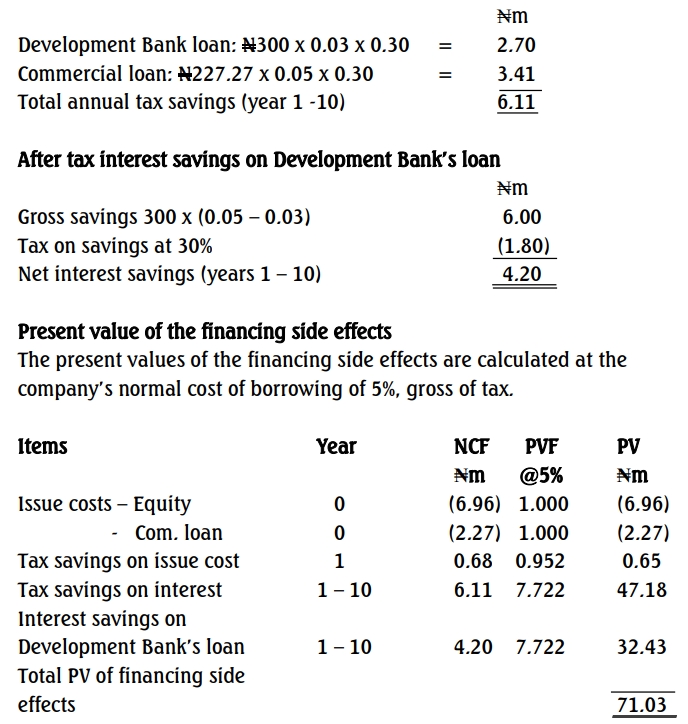

Note: In calculating the present values of the financing cash flows, the

discount factor used is 5% to reflect the normal borrowing/default risk

of the company.

Alternatively, the risk-free rate of 4% could be used depending on the

assumption made. Credit will be given where these are used to

estimate the discount factor.

Recommendation

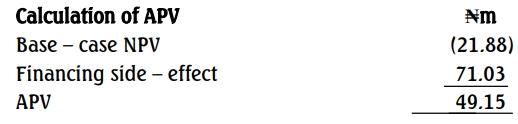

The project has a negative NPV when financed purely by equity, but the financing side effects make the APV positive. Therefore, the project should be accepted as it is expected to increase shareholder wealth by N49.15 million.

(b) Explanation:

i. Circumstances for Using APV

- When a project permanently changes the company’s gearing level.

- Projects involving unusual financing arrangements like subsidized loans.

- When the project significantly alters the company’s debt capacity.

- When considering multiple project-specific financing options.

ii. Advantages of APV

- Provides a clear distinction between operating cash flows and financing side effects.

- More accurate assessment of real project worth.

- Fewer recalculations needed for capital structure changes.

Limitations of APV

- Requires precise identification and quantification of all financing side effects.

- The methodology assumes perpetuities for cash flows, which may not always apply.

- The M&M-based approach ignores bankruptcy costs, tax exhaustion, and agency costs.