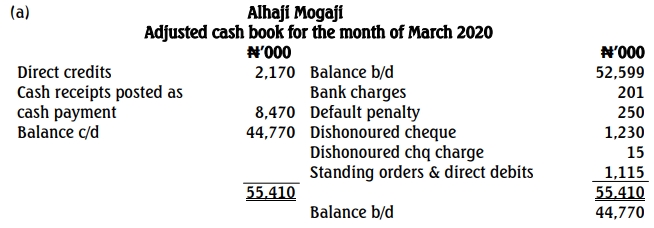

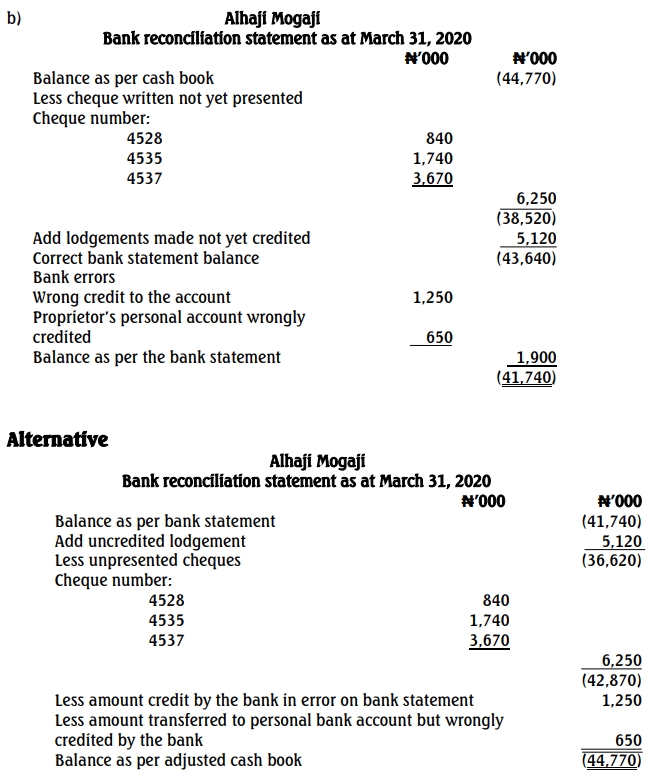

Question

Answer

c. Reasons for preparing a bank reconciliation statement on a regular basis:

- To detect errors on either the cash book or bank statement.

- To ensure that the balance used in the financial statements is accurate by determining the final cash book balance.