Question

Answer

a)

i) Amaka Pharmaceutical

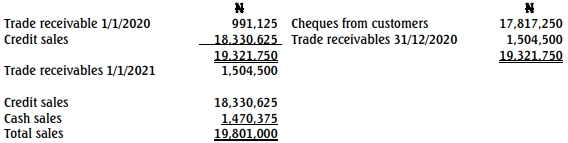

Sales for the year ended December 31, 2020

Sales ledger control account

ii) Amaka pharmaceutical

Purchases for the year ended December 31, 2020

Purchases ledger control account

b)

Amaka Pharmaceutical

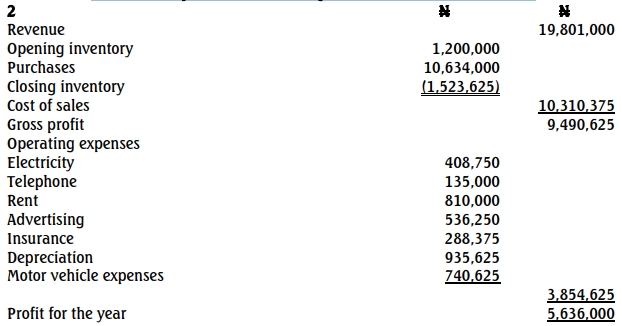

Statement of profit or loss for the year ended December 31, 2020

Workings

1. Calculation of depreciation

2. Motor vehicle expenses account

c)

Amaka pharmaceutical

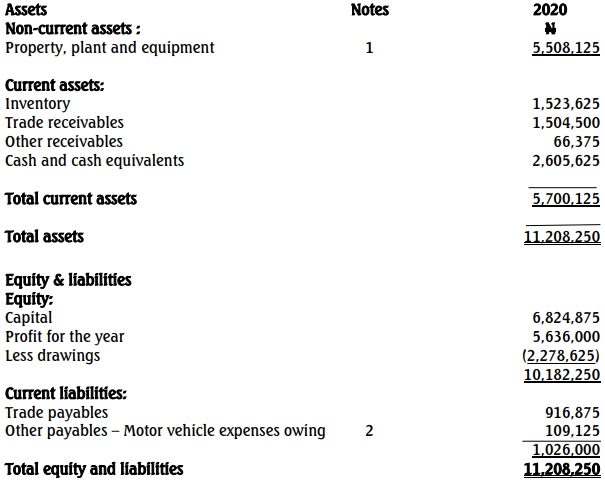

Statement of financial position as at December 31, 2020

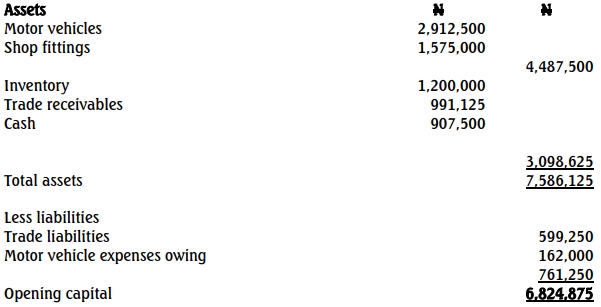

Amaka Pharmaceutical

Statement of opening capital