Question

Answer

a. The rules of IFRS 9 provide guidance on when and how financial assets should be derecognized, with the aim of ensuring that financial assets are removed when the transfer of rights and risks occur, providing transparent and accurate reporting of an entity’s financial position. According to IFRS 9, a financial asset can only be derecognized under the following conditions:

- Contractual right to receive cash flows: Derecognition generally occurs when an entity no longer has the contractual rights to receive cash flows from a financial asset. This can happen through a sale, securitization, or other forms of transfer.

- Transferring of substantial risks and rewards: If an entity retains substantially all the risks and rewards associated with a financial asset despite transferring the contractual rights, derecognition is not appropriate. In such cases, the asset continues to be recognized on the entity’s statement of financial position. For derecognition, the entity must transfer the risks and rewards attributed to the financial asset. Factors such as the extent of exposure to losses or benefits, variability in outcomes, and control are considered in determining retained risks and rewards.

- Loss of control: Derecognition may also occur when the entity no longer controls the financial asset. This typically involves transferring the asset to a third party and relinquishing control over it.

- Continuing involvement: Even if control is lost, the company may still have continuing involvement. In such scenarios, the asset may be recognized either fully or partially on the statement of financial position.

- Exchange of the financial asset: Derecognition may occur if the financial asset is exchanged for another asset or liability.

- Conversion to equity: If a financial asset is converted to an equity item, such as ordinary shares, derecognition may be appropriate.

- Other circumstances: Specific scenarios, such as repurchase agreements and collateralized financing transactions, may also dictate derecognition treatments according to IFRS 9.

b. In this scenario, Royal Business Limited (RBL) entered into a factoring agreement with Hexlinks Bank Limited (HBL) to transfer receivables in exchange for N36 million. The rules of derecognition affect RBL’s financial statements as follows:

- Initial derecognition: When RBL transferred the trade receivables to HBL, it derecognized them from its financial statements. Thus, the carrying amount of N40 million is removed from RBL’s statement of financial position, with a loss of N4 million recognized in profit or loss.

- Continued involvement and potential liability: Despite the transfer, RBL agreed to reimburse HBL for any shortfall between the amount collected and N36 million, retaining a potential liability. The treatment of this liability depends on the factoring agreement and accounting standards.

- Subsequent repayment: Once receivables are collected, any amount above N36 million, less interest, will be repaid to RBL, typically as a separate cash inflow or liability reduction.

- Considerations: The factoring agreement and repayment arrangement may require additional analysis based on standards like IFRS or GAAP, considering the terms of the agreement.

In summary, derecognition removes the assets from RBL’s statement of financial position, with a loss recorded in profit or loss. However, RBL’s potential liability and repayment arrangement with HBL may need further analysis based on applicable standards.

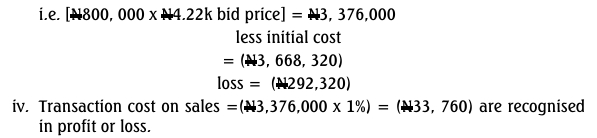

c. Accounting treatments of share transactions in the financial statements of Pelumi Company Limited as at December 31, 2021:

- Initial Measurement: The shares are initially measured at fair value, calculated as the purchase price plus transaction cost:

![]()