Question

Answer

(a): Differences Between Defined Contribution Plan and Defined Benefit Plan

Defined Contribution Plan

- In a defined contribution plan, both the employer and employee contribute a fixed amount to a separate entity, such as a pension fund.

- The employer’s obligation is limited to the agreed contributions.

- If the fund’s assets are insufficient to pay the promised benefits, the employer has no further liability.

- The risk and reward of the plan’s performance rest with the employee.

Defined Benefit Plan

- In a defined benefit plan, the employer guarantees a specific level of benefits upon retirement.

- The benefits are based on factors such as the employee’s final salary and years of service.

- The employer has a legal or constructive obligation to ensure the fund has sufficient resources to pay the promised benefits.

- The risk of the plan’s performance rests with the employer, as they must cover any shortfall.

Classification of CBK’s Post-employment Plan

Based on the details provided, CBK’s post-employment plan qualifies as a defined benefit plan under IAS 19. This is because:

- CBK guarantees a specific benefit to employees (150% of the annual pay at the time of retirement multiplied by years of service).

- The plan is not funded, and CBK retains the liability to pay employees directly.

- The financial risks, such as future salary increases and employee longevity, are borne by CBK.

Thus, the plan should be classified as a defined benefit plan.

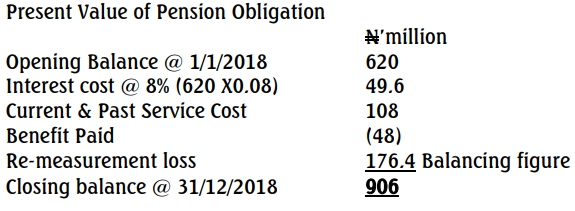

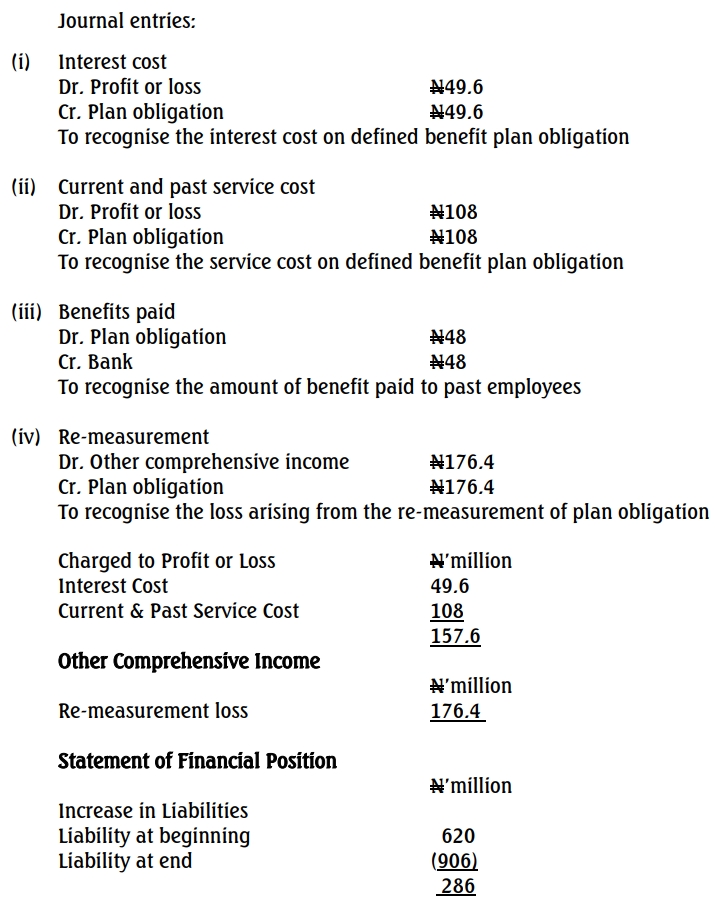

(b) Reconciliation