Question

Below is the draft financial statement of Lanwani Plc., a manufacturer of fast-moving consumer goods.

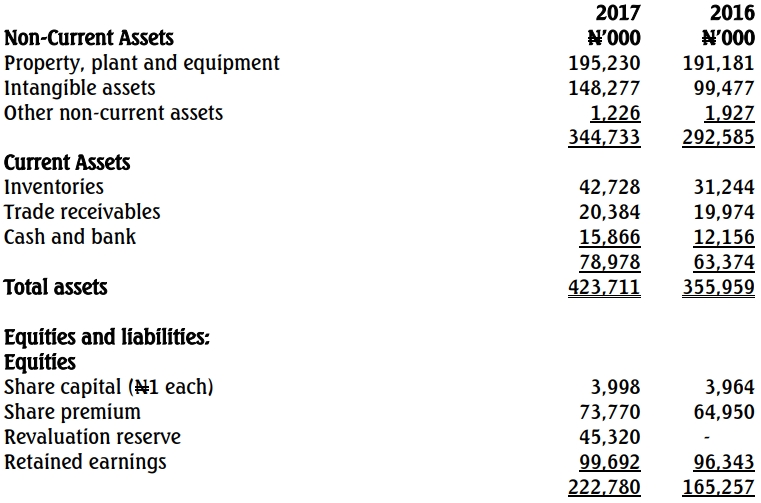

Statement of financial position as at

Statement of profit or loss

Additional Information:

- The company changed its accounting policy from the cost model to the revaluation model for its property. The revaluation reserve represents the revaluation surplus recognized in 2017. No adjustment was made for 2016.

- Development costs of ₦45 billion were capitalized during 2017. The related asset is not expected to generate economic benefits until 2020.

Required:

a. Assess the accounting treatment of the change in accounting policy and state the impact on the return on capital employed (ROCE). (3 Marks)

b. Analyze the profitability, liquidity, and efficiency of Lanwani Plc. (15 Marks)

c. Briefly discuss TWO limitations of the analysis done in (b) above. (2 Marks)

Answer

(a)

Accounting policies are the principles, rules, and conventions that guide the preparation of financial statements. Consistency in applying an accounting policy is essential, and a change can only occur if it is mandated by IFRS or if it results in more relevant and reliable information.

- IFRS Requirement for Change: When a change in accounting policy is required by an IFRS, the entity must apply the policy in accordance with that standard.

- Retrospective vs. Prospective Application: Retrospective application, which involves restating comparative figures from prior periods, is generally required unless it is impracticable. In such cases, reasonable efforts must be made to comply.

However, retrospective application does not apply when moving from the cost model to the revaluation model under IAS 16.

In the case of Lanwani Plc., the failure to apply retrospective adjustments for the policy change results in inconsistencies between the current and prior year financial statements. Specifically:

- Impact on ROCE (Return on Capital Employed): The recognition of the revaluation surplus and capitalization of development costs in 2017 increases the capital employed figure, which may lead to a lower ROCE compared to 2016. This could misrepresent the company’s operational performance by creating a perception of reduced efficiency in generating returns on its employed capital.

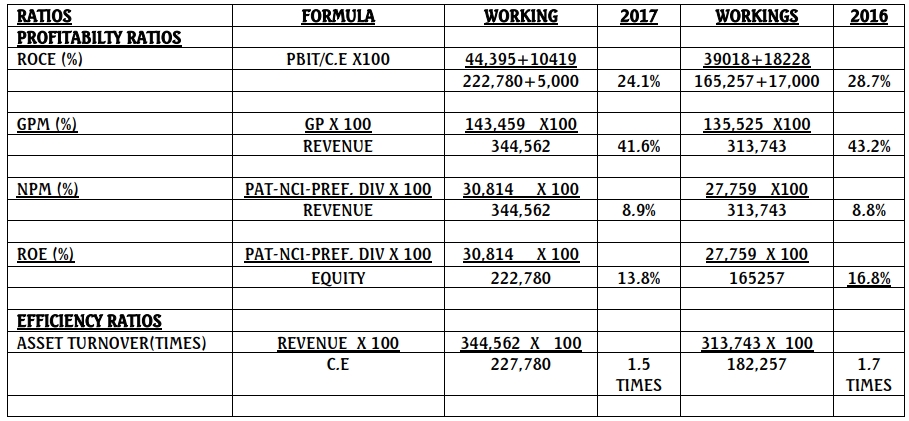

b) LANWANI PLC

COMPUTATION OF FINANCIAL RATIOS FOR THE YEAR ENDED 2017

Brief Comments on Lanwani Plc’s Financial Statement Analysis for the Year Ended 2017

The analysis evaluates the profitability, liquidity, and efficiency of Lanwani Plc, a manufacturer of fast-moving consumer goods, based on its financial statements.

Profitability

Profitability ratios assess the company’s ability to generate returns. Higher ratios indicate better performance.

- ROCE (Return on Capital Employed):

The ROCE declined from 28.7% in 2016 to 24.1% in 2017. This drop is likely due to the revaluation surplus and capitalized development costs that inflated the capital employed. Additionally, a decrease in profit margins may have contributed to the decline. - Recommendations:

Management should focus on optimizing production processes and reducing overhead costs to minimize wastage and improve profit margins.

Efficiency

Efficiency ratios measure how effectively the company uses its assets to generate revenue.

- Asset Turnover:

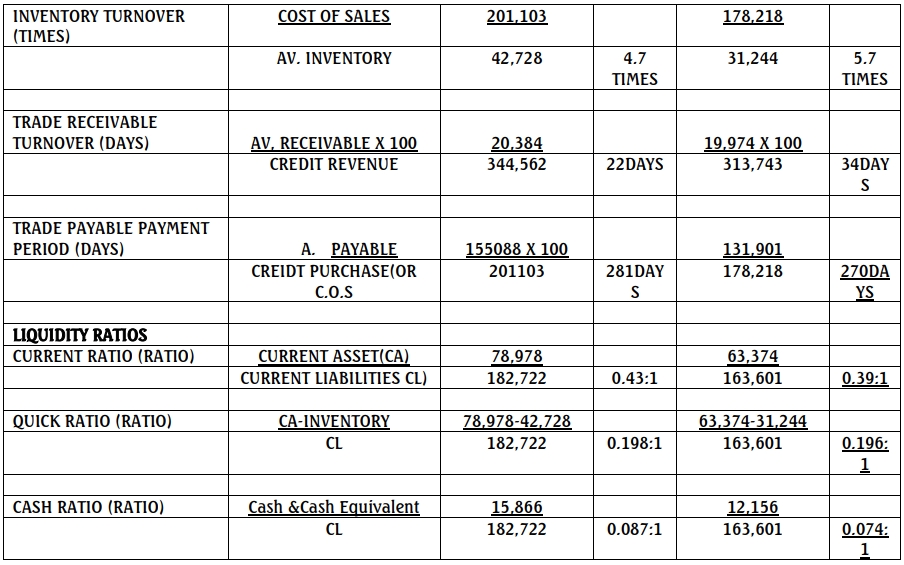

This metric slightly decreased from 1.7 times in 2016 to 1.5 times in 2017. - Inventory Turnover:

The inventory turnover dropped from 5.7 times to 4.7 times, indicating less efficient inventory management. - Receivables and Payables Management:

Despite improved receivables collection efficiency in 2017, trade payables increased significantly, resulting in extended payment periods, which may indicate liquidity challenges. - Recommendations:

Management should consider disposing of or replacing non-performing assets and adopting a Just-in-Time (JIT) inventory system to optimize inventory levels and turnover.

Liquidity

Liquidity ratios indicate the company’s ability to meet short-term obligations.

- Current, Quick, and Cash Ratios:

Although these ratios showed marginal improvement from 2016 to 2017, they remain significantly below industry averages, highlighting the company’s weak liquidity position. - Recommendations:

Management should explore options to dispose of non-performing assets to strengthen the liquidity position and support short-term obligations.

Conclusion

The financial performance, efficiency, and liquidity of Lanwani Plc are underwhelming. Implementing the above recommendations and hiring skilled professionals to manage the company’s operations could potentially turn its performance around.

(c) Limitations of Ratio Analysis

- Use of Different Accounting Policies:

Comparing financial ratios across entities or periods is misleading when different accounting policies are applied, as this creates inconsistencies in reported figures. - Geographical and Economic Differences:

Entities operating in different locations face varying economic, legal, and market conditions, which can distort the interpretation of ratios. - Different Accounting Dates:

Disparities in financial year-end dates can lead to inaccurate comparisons. - Impact of Inflation:

Inflation can skew historical financial data, making it less relevant for analysis. - Manipulation of Accounts:

Companies can manipulate financial results to present misleading ratios, affecting the reliability of the analysis.