ABC & CO. (Tax Consultants)

ABC Avenue, Lagos.

April 10, 2020

The Managing Director

Sunchi West Africa Holdings

Ibadan

Dear Sir,

RE: TAXATION OF RESIDENT AND NON-RESIDENT COMPANIES IN NIGERIA

I refer to your mail of April 5, 2020 on the above subject, requesting us to unravel the issue of payment of companies income tax by resident and non-resident companies operating in Nigeria. Please find below relevant issues that will facilitate your understanding of the situation:

a) Resident company

A company is resident in Nigeria under the extant law, if it is incorporated or registered in Nigeria. This means that the taxpayer is liable to tax on the income or profits accruing in, derived from, brought into, or received in Nigeria Non-resident company

This is a company that is not registered or incorporated in Nigeria, but which derives income or profits from Nigeria. A non-resident corporation or individual is liable to tax only on the profit or income deemed to be derived from Nigeria.

b) Circumstances under which a non-resident company will be liable to tax in Nigeria

These include:

Fixed base of business: If a non-resident company has a ―fixed base‖ from which it carries on its business or trade in Nigeria, the profits from such activities would be deemed to be derived from Nigeria;

Agency operation: Where a non-resident company does not have a fixed base but habitually operates a trade or business through a person in Nigeria who:

– is authorised to conclude contracts on its behalf or on behalf of some other companies controlled by it or which has controlling interest in them or

– habitually maintains a stock or goods or merchandise in Nigeria from which deliveries are regularly made by a person on behalf of the company, then an agency arrangement is deemed to have arisen.

The profit deemed to have been derived from Nigeria is the profit

attributable to the business or trade or activities carried on through the

agent.

Turnkey projects: This is a trade or business or activity which involves a single contract for the surveys, deliveries, installations or construction.

For Nigerian income tax purposes, the profit from such a tunkey project is considered as derived from Nigeria and this will be liable to tax.

Income derived by non-resident company from professional consultancy, management and technical services rendered in Nigeria.

Income derived from supervisory activity that lasts more than three (3) months.

Income derived by a non-resident company from investment, such as

dividend, interest, rent and royalties. The withholding tax deducted from

these incomes is taken as the final tax.

Income derived from a contract awarded to a Nigerian company, but subcontracted to a non-resident company

c i) Relationship between a Nigerian branch and a foreign parent company

Under the Companies Income Tax Act Cap C21 LFN 2004 (as amended) citizens of other countries, that are foreign nationals can incorporate a company or corporation (other than a corporation sole). This is regarded as a resident company that is a Nigerian company.

However, a Nigerian branch of a foreign company is treated as a

corporate entity. Income or profits derived by such company in Nigeria is

taxable in Nigeria.

The conditions under which such a Nigerian company will not be liable to Nigerian tax are where:

The branch of the foreign company is used solely for the storage or

display of goods or merchandise; and

The branch is used for collection of information.

c ii) Nigerian subsidiary and a foreign parent company

Under the Nigerian tax laws, the subsidiary of the foreign parent

company must be incorporated in Nigeria.

The foreign equity participation may be 100% (wholly-owned) or less

than 100% (partly owned), this will not affect the residence status in

Nigeria.

Dividends distributed by the Nigerian subsidiary of the parent company is a franked investment income and shall be exempted from tax in the hands of the parent company. But it will be subjected to withholding tax of 7.5% in Nigeria.

d) Overseas branch of a Nigerian company

For tax purposes, the profit of an overseas branch of a Nigerian company is deemed to be derived in Nigeria and is therefore fully liable to tax in Nigeria.

It is essential to know that the foreign tax suffered is allowable as a

deduction in determining the overseas profits.

Assets in such a branch are eligible for capital allowances claim in

Nigeria.

Losses incurred can be set off against profit in Nigeria provided such

losses were incurred from the same source.

Double Taxation Relief (DTA) is available for any foreign tax suffered.

e) Overseas subsidiary of a Nigerian company

For tax purposes, the profit of an overseas subsidiary is not deemed to be derived in Nigeria and will therefore not be liable to tax in Nigeria.

It is only dividend received from such overseas subsidiary that will be

considered for Nigerian tax purposes.

Technical and management fees paid to the Nigerian company by the

overseas subsidiary will be subjected to tax in Nigeria.

Capital allowances will not be claimable on the assets of the overseas

subsidiary.

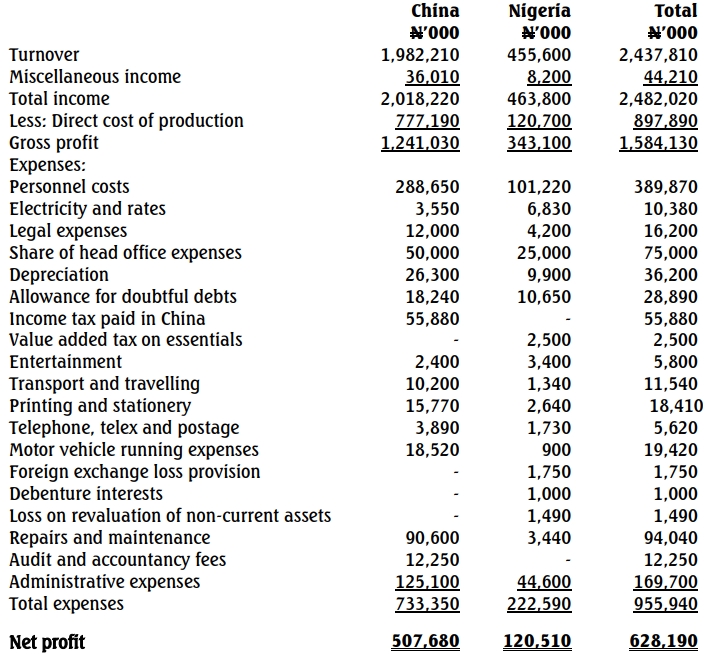

f) Computation of companies income tax payable by the Nigerian

subsidiary The companies income tax payable by the Nigerian subsidiary is N31,415,100, while the tertiary education tax is N2,899,400 (See Appendix I). The China operation is not liable to Nigerian tax, hence no computation of adjusted/assessable profit. We have commented on areas deemed necessary. Nevertheless, if you should still need further clarification(s), please do not hesitate to contact us.

Yours faithfully,

Chukwu, A. O

Senior Consultant