Question

Answer

(a) Mr Eket

Computation of capital gains tax for 2012 year of assessment

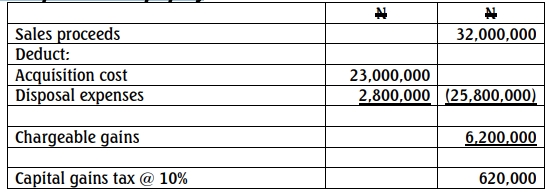

Disposal of Kano property

Mr. Eket

Computation of capital gains tax for 2014 year of assessment

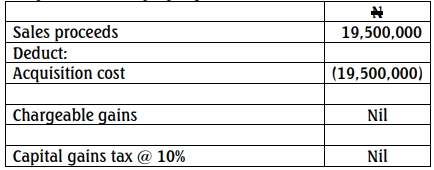

Disposal of Benin property to Emem

Mr. Eket

Computation of capital gains tax for 2014 year of assessment

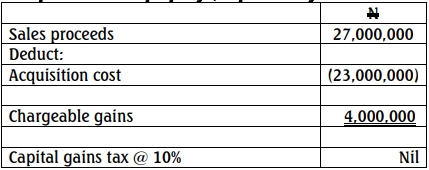

Disposal of Benin property (Acquisition by the Edo State Government)

(b) The relevant tax authority to which the Capital Gains Tax (CGT) is payable for the property in Kano is Akwa Ibom State Internal Revenue Service, while that of Benin is also the same Revenue Service.

c. Reasons for the solutions in 5a & 5b

(i) Basis for determining the capital gains tax in (a) above:

The disposal of property in Kano by Eket is liable to capital gains tax at 10% of the chargeable gain because it is not established that the Kano property is a private residence of Mr. Eket. Therefore, the property is a chargeable asset liable to CGT in 2012 year of assessment on actual year basis. The disposal of Benin property to Emem is by way of gift, therefore the consideration must be such amount that is sufficient to secure the disposal. Therefore, neither gain nor a loss shall accrue to the executors for Eket‟s Will in 2014 year of assessment.

However, the disposal of Benin property to Edo State Government was through forced acquisition. Assets disposed due to compulsory or forceful acquisition are specifically exempted from capital gains tax, provided the owner has not taken any prior step to dispose such asset. The chargeable gain of N4 million on disposal of Benin property in 2016 YOA shall be exempted from CGT.

(ii) The relevant tax authority to which the capital gains tax is due is Akwa-Ibom State Internal Revenue Service. The reason is that Mr. Eket and Emem (Mrs Eket) are native of Akwa-Ibom State and reside in Oron, Akwa-Ibom State.