Question

Answer

The managing director

Sadiq Corporation

Sweden

Through:

The managing director

Omologede Ventures Nigeria Limited

Akure, Nigeria

Subject: Tax Implications of Renovation Contracts in Benue and Ebonyi States, Nigeria

Dear Sir,

Based on the provided contractual details and financial statements submitted by Omologede Ventures Nigeria Limited for the fiscal year ending December 31, 2017, we advise as follows regarding the tax obligations:

- Nature of Project:

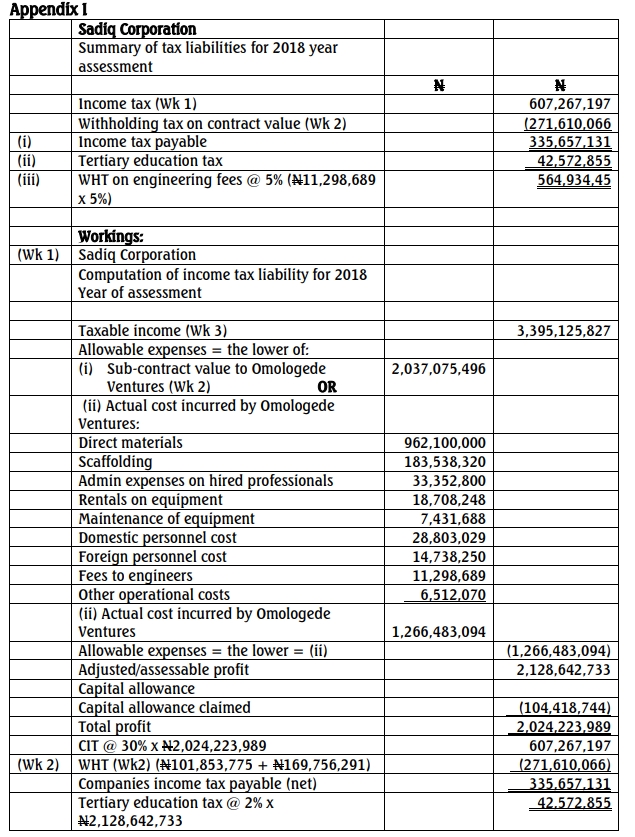

The contract awarded by Peniel Nigeria Plc to Sadiq Corporation is a turnkey project, which implies a single contract encompassing design, delivery, and installation within Nigeria. As a result, the entire revenue earned on this project is taxable in Nigeria, irrespective of the contractor’s residence status. - Taxable Profit:

Since the whole profit earned on the contracts in both Benue and Ebonyi states is deemed Nigerian-sourced income, it is subject to taxation in Nigeria. The expenses associated with the subcontract work assigned to Omologede Ventures Nigeria Limited will be recognized for tax purposes. However, allowable expenses will be capped at the actual costs incurred by Omologede Ventures as stipulated by Nigerian tax laws. - Withholding Tax (WHT):

- Peniel Nigeria Plc deducted 5% WHT on the total contract payment to Sadiq Corporation, which will serve as a tax credit.

- Sadiq Corporation, in turn, is responsible for deducting 5% WHT from its subcontracted payments to Omologede Ventures.

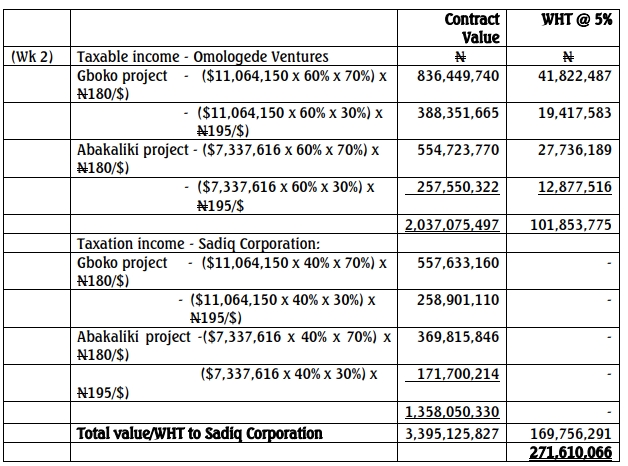

- Exchange Rate Adjustments:

The exchange rate was initially N180 to $1 but rose to N195 by August 2017. The fluctuating rates affected the contract payments and must be factored into the tax calculations to accurately determine the assessable income. - Capital Allowance and Depreciation:

The agreed capital allowance of N104,418,744 and depreciation (N69,902,092) on the equipment utilized by Omologede Ventures should be incorporated to reduce the taxable profit further.

Since a withholding tax of 5% would have been deducted on the total contract value by Peniel Nigeria Plc, the same total withholding tax credit will be utilized by Sadiq Corporation. Also, Sadiq Corporation is obliged to deduct withholding tax from the sub-contract to Omologede Ventures because it was an entirely fresh contract to Omologede Ventures and only the tax withheld on the contract fee to nOmologede Ventures shall be utilized by Omologede Ventures. Therefore, the withholding tax to be utilized against the total income tax on the contract is the aggregate of tax withheld by Peniel Nigeria Plc and Sadiq Corporation as shown above.