Question

Dadinkowa Nigeria Limited has been in business since 2009 as a manufacturer of sugar cubes. The company sources its raw materials, sugar cane, from the Northern part of the country. However, due to local security challenges, the company has faced supply disruptions since 2016.

Additionally, the company has disagreements with tax authorities regarding the treatment of certain items (e.g., donations and dividend income) in their financial statements and returns. High overhead costs, especially energy expenses, have worsened operational challenges.

At a recent board meeting, the directors proposed either a temporary closure or relocating to a neighboring country if conditions do not improve in the next fiscal year. The General Manager shared this with you during your visit as the company’s tax consultant, seeking your advice to address these issues.

A scheduled meeting with the Managing Director requires you to prepare a comprehensive tax report addressing:

- Determination of the company’s tax liabilities for the relevant tax year.

- Analysis of the treatment of donations and exemptions of dividend income under the Companies Income Tax Act (CITA).

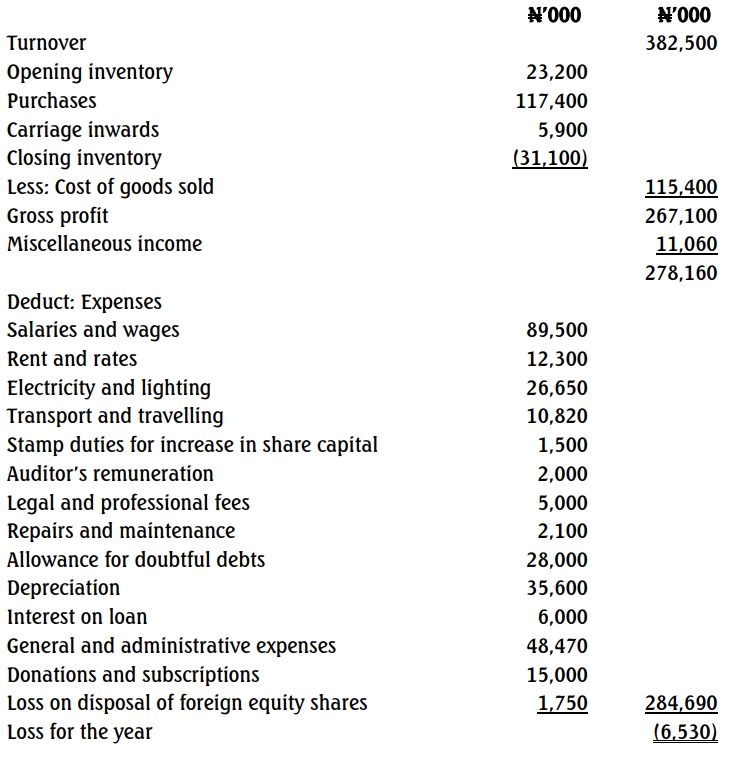

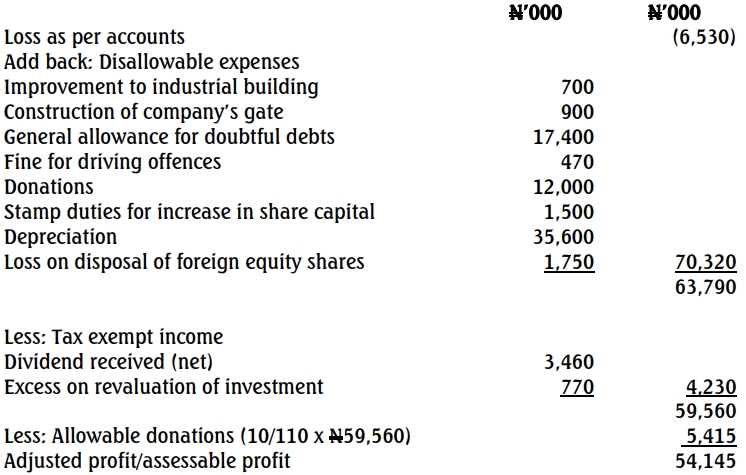

The profit or loss account for the year ended December 31, 2021, is as follows:

Profit or Loss Account:

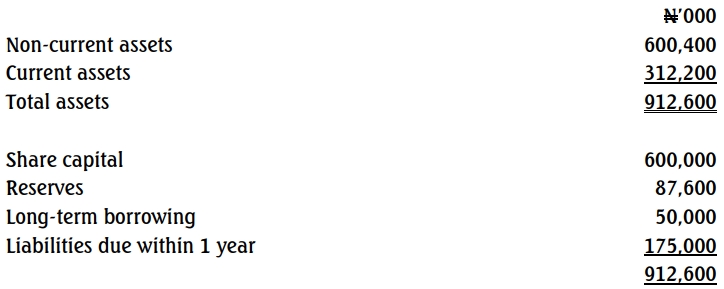

Extract from the company’s statement of financial position as at December 31, 2021 revealed:

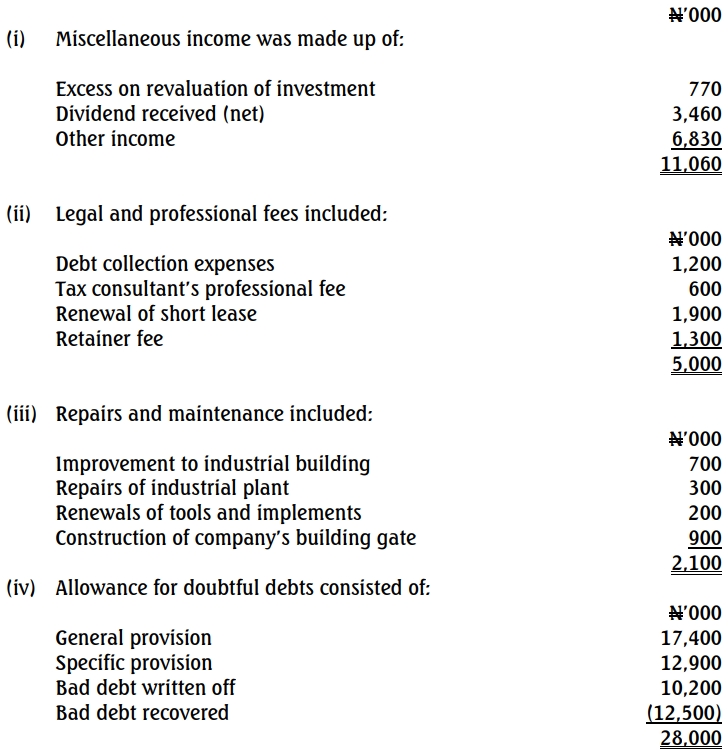

The following additional information was made available:

(v) Interest on loan was paid on a facility obtained from a licensed Nigerian deposit money bank at commercial interest rate.

(vi) General and administrative expenses were made up of:

(vii) Donations and subscriptions

Included in donations was N12,000,000 paid to a fund created by the Federal Government for victims of communal crisis that took place where the company is situated.

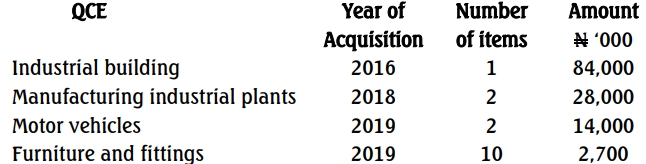

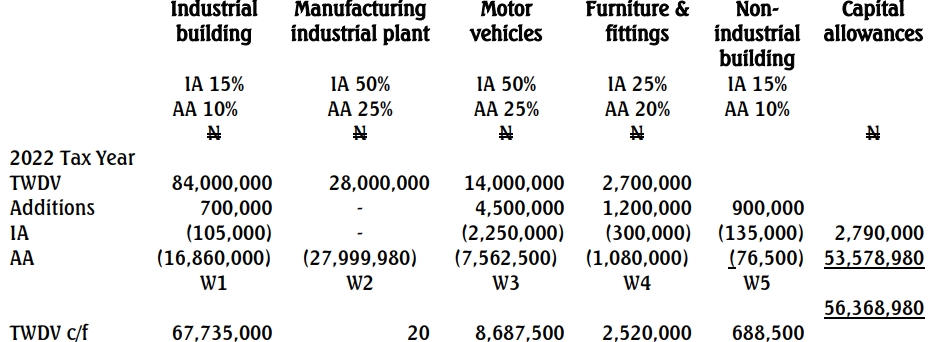

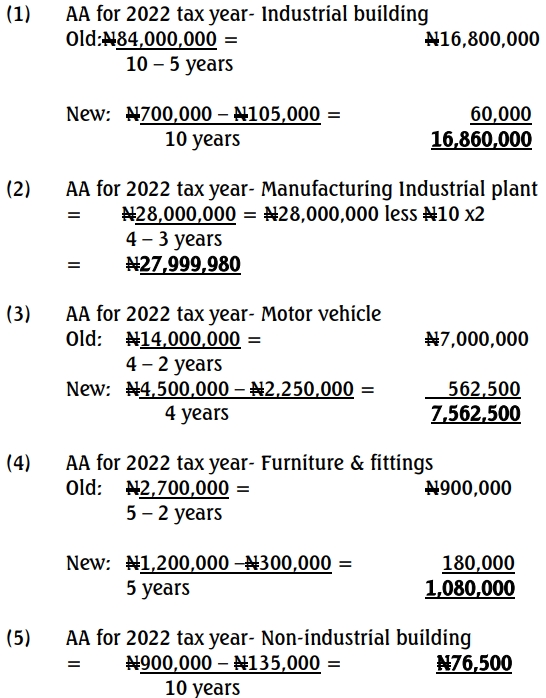

(viii) The tax written down values of the qualifying capital expenditure (QCE) items as at December 31, 2020 were:

(ix) Additions to QCEs during the year ended December 31, 2021 were:

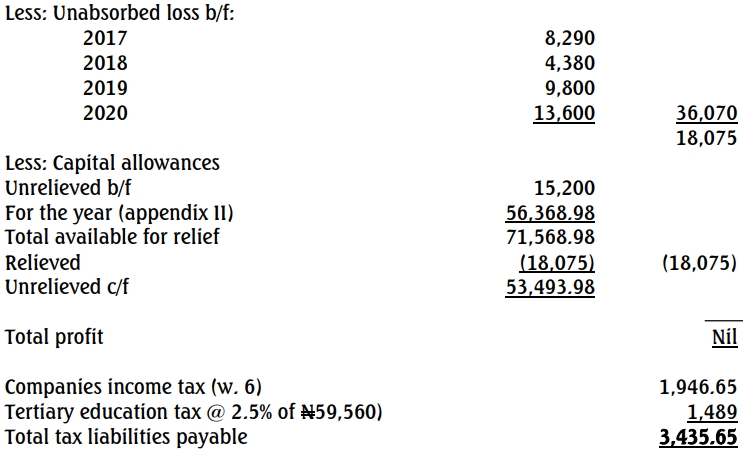

(x) Unrelieved capital allowances brought forward were N15,200,000.

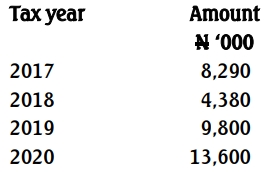

(xi) Unabsorbed losses from previous years were:

Required:

As the company’s Tax Consultant, you are to draft a report to the Managing Director for the scheduled meeting expected to hold next week. This is expected to address the following:

a. Determination of the company’s tax liabilities for the relevant tax year. (20 Marks)

b. Comment, in line with the provisions of Companies Income Tax Act Cap C21 LFN 2004 (as amended) on:

i. The treatment of donations made by the company during the year under review (5 Marks)

ii. Exemption of dividends from taxation (5 Marks)

Answer

OK & Co (Chartered Accountants)

Igbogbo Road, Lagos

Date: ……

The Managing Director

Dadinkowa Nigeria Limited

Lagos.

RE: COMPUTATION OF TAX LIABILITIES AND OTHER MATTERS THEREOF

I refer to our discussion of April 12, 2022, on your request for computation of the company’s tax liabilities for the 2022 assessment year and advice on the treatment of donations made during the year and dividends exempted from tax. I hereby present a report for your review before the same is processed for filing with the tax authorities.

(a) Determination of Tax Liabilities

Financial records of the company for the year ended December 31, 2021, revealed an operating loss of ₦6,530,000. For tax purposes and in line with the provisions of the Companies Income Tax Act 2004 (as amended), the profit or loss made by a corporate entity has to be adjusted. When this was done, the company made an adjusted profit of ₦54,145,000.

The company was able to relieve all the unabsorbed losses for the 2017, 2018, 2019, and 2020 tax years, which amounted to ₦36,070,000. However, only ₦18,075,000 out of ₦71,568,980 capital allowances available for relief was utilised, while the unutilised portion of ₦53,493,980 is deferred to next year for possible utilisation from profit.

Following the above, the company has zero total profit for the period under review. Section 13 of the Finance Act 2020 stipulates that any company that falls into this category (zero or insufficient profit) has to pay a minimum tax. Thus, the company is liable to pay a minimum tax of ₦1,946,650. There is also a tertiary education tax that is compulsory for companies operating in Nigeria to pay. The new rate is 2.5% of adjusted profit, which is ₦1,489,000. The total tax liabilities for the 2022 tax year is ₦3,435,650.

We suggest that every effort be put in place for filing of annual tax returns with the Federal Inland Revenue Service within the statutory time limit provided under the Act.

(b) Treatment of Donations and Dividends

(i) The Treatment of Donations Made by the Company During the Year Under Review

The CITA 2004 (as amended) recognises the importance of donations made by a corporate entity. However, for such donations to be allowed as expenses in the determination of total profit and subsequently tax liabilities payable in any year of assessment, it has to fulfill some conditions. These conditions are:

- It must be made to any of the funds, bodies, institutions in Nigeria contained in the Fifth Schedule to CITA.

- It must be made out of profit.

- It must not be of capital nature, except donations to a university or other tertiary or research institutions.

- It must not exceed 10% of the company’s total profits for an assessment year before any deduction for donation. In the case of donations to tertiary or research institutions, up to 15% of total profit or 25% of tax payable in the year, whichever is higher.

- Donations made by companies in cash or kind to any fund set up by the Federal Government or to any similar fund or purpose in consultation with any Ministry, department, or agency of the Federal Government, in respect of any pandemic, natural disaster, or other exigency shall be allowed as deduction provided that requisite documentation documenting the donations and the cost thereof are provided to the relevant tax authority.

- The amounts allowable for deduction in respect of the above, in any year of assessment shall be limited to 10% of assessable profits after deduction of allowable donations made by the company.

Based on the foregoing, it is evident that the ₦12 million donations made by the company to a fund established by the Federal Government for victims of the crisis was to a recognised fund. However, the amount of the donation was in excess of 10% of the company’s total profits for an assessment year before any deduction for donations. It is on the basis of the above that the tax authority will not regard the whole of ₦12 million donations made by the company as an allowable expense in the determination of tax liabilities for the 2022 tax year.

The Revenue Service will only allow the amount of donations, which is restricted to 10% of assessable profits after such deduction. This is equal to ₦5,415,000.

(ii) Dividends Exempted from Taxation

The CITA 2004 (as amended) clearly provides for the treatment of dividend income. There is no inconsistency in its treatment. The following are dividends exempted from taxation:

- Dividends received by way of a bonus issue of shares.

- Dividends received from a pioneer company.

- Dividends received from a company subjected to tax under the PIA 2021.

- Dividends received from a foreign investment, provided such dividend is received through a domiciliary account.

- Dividends received net of withholding tax by a Nigerian company from another Nigerian company.

- Dividends received from small companies in the manufacturing sector in the first five years.

- Dividends received from investment in wholly export-oriented businesses.

- Dividends received from a unit trust scheme.

- Dividends received by a company from another one, provided that the equity participation on which the dividend is paid:

- Is either wholly paid for in foreign currency or by assets brought to Nigeria.

- Is not less than 10% of the equity share capital of the company paying the dividend.

We hope that this report adequately represents the mandate assigned to us. Should you need further clarification on this, we will be glad to address it.

Yours faithfully,

Kem Adek

Principal Consultant

Appendix 1: Computation of tax liabilities

Appendix II: Capital allowances computation

Working notes

(6) Minimum tax computation

Section 13 of Finance Act 2020 provides that minimum tax = 0.5% of gross turnover of the company less franked investment income. It also states that the applicable minimum tax is reduced to 0.25% for tax returns provided and filed for any year of assessment falling due on any date between 1 January 2020 and 31 December 2021. 0.5% of gross turnover of the company less franked investment income

Minimum tax = 0.5% of (N382,500,000 + N6,830,000)

= 0.5% of (N389,330,000) = N1,946,650