Question

Answer

24 Abbey Plaza, Ikeja Lagos

April 10, 2021

The Managing Director

DD Nigeria Limited

Colmas Road, Alabata

Abeokuta

RE: CAPITAL GAINS TAX ON DISPOSAL OF CHARGEABLE ASSETS

I refer to your mail of April 5, 2021, requesting our advice on tax matters relating to the above subject matter. We wish to comment as follows:

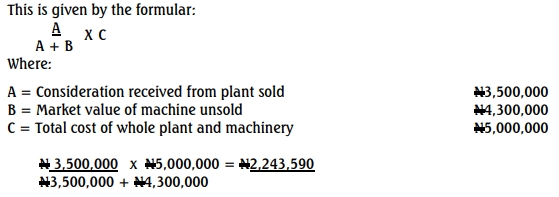

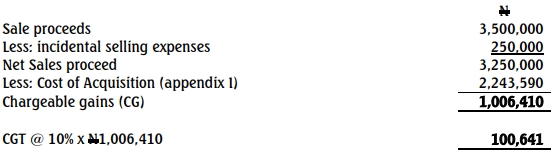

(a) Disposal of Plant on September 15, 2019

- This is a partial disposal of plant from the entire plant and machinery acquired for ₦5,000,000.

- The cost apportioned to the plant is ₦2,243,590, as per Appendix I.

- A chargeable gain of ₦1,006,410 arises, being the difference between the consideration received (₦3,500,000) and the apportioned cost.

- The chargeable gain is liable to Capital Gains Tax (CGT) at 10%, resulting in a tax liability of ₦100,641, as per Appendix II.

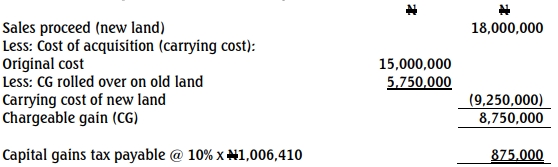

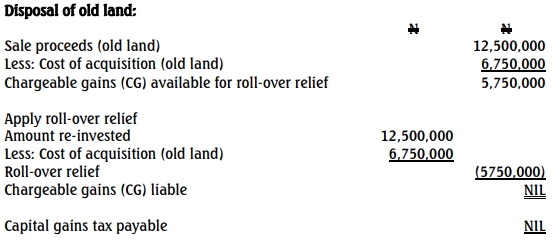

(b) Disposal of Land in May 2018 and June 2019

(i) Roll-Over Relief:

- A relief is available under CGT where the consideration received from the disposal of an asset is reinvested in acquiring another asset of the same class.

- The relief defers the CGT on the chargeable gain until the new asset is eventually disposed of.

(ii) Disposal of Old Land:

- Sale price: ₦12,500,000

- Acquisition of new land for ₦15,000,000 qualifies for a full roll-over relief of ₦5,750,000 (Appendix III).

- The roll-over relief defers the CGT on the old land until the new land is disposed of.

(iii) Cost of New Land:

- The carrying cost of the new land is ₦9,250,000 (₦15,000,000 original cost less ₦5,750,000 chargeable gain rolled over).

(iv) Capital Gains Tax:

- There is no CGT payable on the old land due to the roll-over relief.

- CGT of ₦875,000 is due on the disposal of the new land in the 2019 Year of Assessment as per Appendix IV.

(c) Tax Implication on Compensation Received for Damaged Industrial Building

- Where an asset is lost or destroyed, and the compensation is utilized within three years to purchase a replacement, roll-over relief is available.

- The ₦2,200,000 received as compensation under the insurance policy is deemed as consideration from the disposal of the old building.

- The company’s intention to utilize the compensation to acquire a new building qualifies for roll-over relief if the new building is acquired within three years of the disposal.

(d) Treatment of Gains Arising from Business Reorganization (S.49, Finance Act 2019)

- Gains from asset transfers in related-party business reorganizations are exempt from CGT if the minimum holding test is met.

Minimum Holding Test:

- The acquired company must be a member of the group for at least 365 days prior to the transaction.

- The acquiring company must hold the transferred assets for at least 365 days after the transaction.

- If the conditions are not met, the exemption is withdrawn.

Attached appendices (I-IV) provide detailed computations. Please reach out if further clarification is required.

Yours faithfully,

Sunny Kajooo

Principal Partner

APPENDIX I: Cost of acquisition for plant disposed

APPENDIX II: Computation of CGT for 2019 year of assessment

APPENDIX III: Computation of CGT for 2018 year of assessment

APPENDIX IV: Computation of CGT for 2019 year of assessment