Question

DIY Limited was incorporated on June 12, 2010, and commenced commercial activities on October 1, 2011.

The primary activities of the company are the manufacture, distribution, and sale of solar panels for domestic use. DIY Limited has its main factory in Daura, Katsina State, Northern Nigeria, and distributors in Kaduna, Abeokuta, Onitsha, and Ilorin.

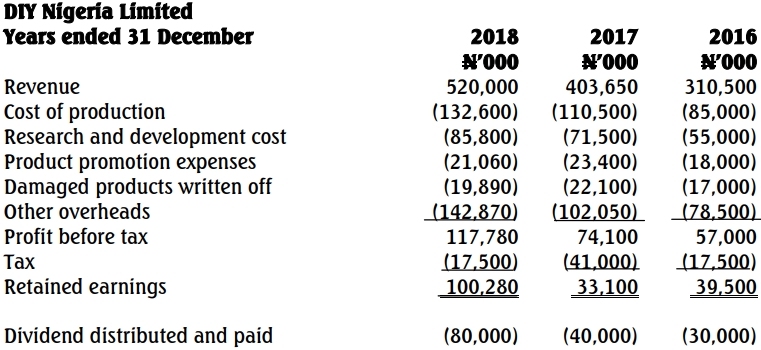

Extracts from the company’s audited financial statements for 2016 to 2018 are as follows:

Note:

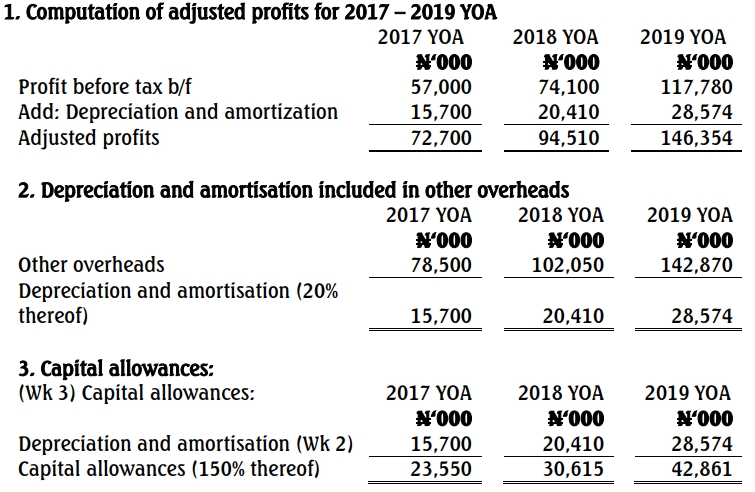

- 20% of “other overheads” represent depreciation and amortization for each year.

- Capital allowances for the respective years represent 150% of depreciation and amortization.

Chief Musa Jugula (MJ), the owner and founder of DIY Limited, owns 70% of the shares of the company while the remaining 30% shares are currently held by his three children and two wives.

Chief MJ is considering expanding into Ghana, exploring either a branch or a subsidiary model. He is also interested in the African Continental Free Trade Area agreement and its implications compared to the ECOWAS region.

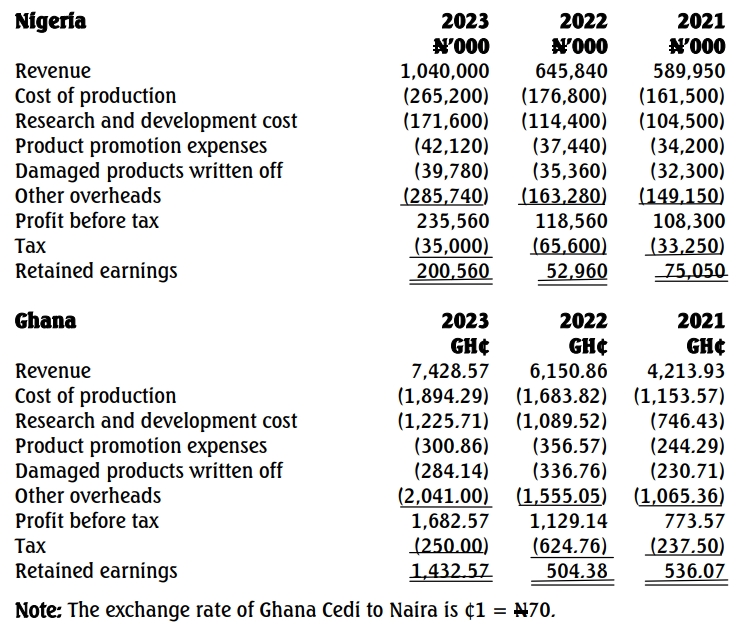

Forecast financial performance for 2021 to 2023:

Required:

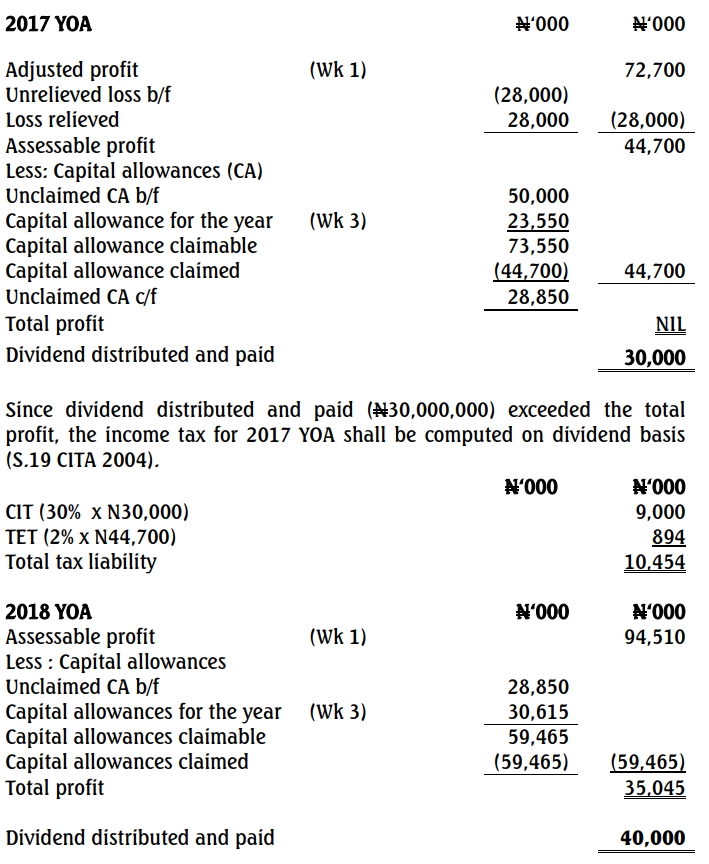

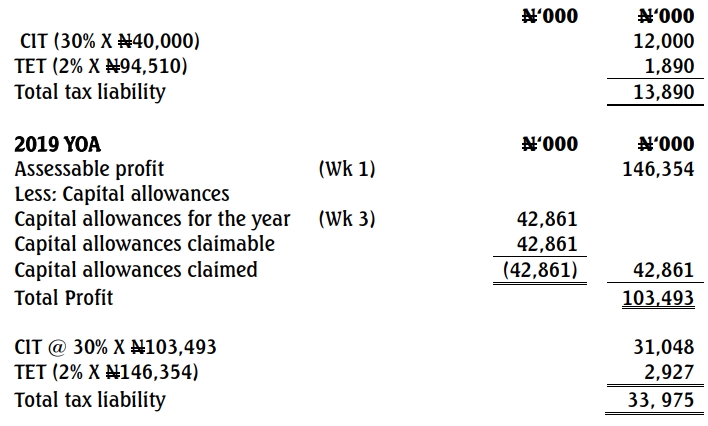

a. Compute the Companies Income Tax (CIT) and Tertiary Education Tax (TET) payable by DIY Limited for 2017 to 2019 years of assessment and comment on any issues you consider as enablers or hindrances to investment promotion in Nigeria. Assume a tax written-down value of qualifying capital expenditure (QCE) of ₦230 million, unutilized losses of ₦28 million, and capital allowances brought forward of ₦50 million for the 2017 year of assessment.

b. As the Managing Partner of Poknos & Co, write a brief advice to Chief Musa Jugula about the African Continental Free Trade Area agreement and how the treaty compares to that of Economic Community of West African States (ECOWAS) region from the perspective of trade in goods. Your advice should cover both opportunities and challenges that may arise from the implementation of the African Continental Free Trade Agreement. (10 Marks)

c. Advise with reasons:

i. If DIY Limited is liable to prepare and submit Country-by-Country Reports (CbCR). (5 Marks)

ii. The relevant tax authority where the Country-by-Country Reports (CbCR) should be submitted, assuming it is applicable to the company. (5 Marks)

Answer

(a) DIY Limited

Computation of tax liabilities for 2017 – 2019 years of assessment (YOA)

Dividend distributed and paid (N40,000,000) exceeded the profit (N35,045,000) therefore, income tax for 2018 YOA shall be computed on dividend basis (S19 CITA 2004)

Workings

- Comments on Enablers and Hindrances to Investment in Nigeria:

- Enablers:

- Tax holidays and pioneer status incentives.

- Existence of free trade zones with tax exemptions.

- Political and economic stability (relatively).

- Hindrances:

- Multiple taxation at different levels.

- Corruption and bureaucratic inefficiencies.

- Infrastructural deficits, particularly in power supply.

- Enablers:

(b)

Poknos & Co

Suite 104 Mea Shopping Mall, Lagos

May 24, 2021

The Founder

DIY Limited

1 Lagos Road, Daura

Katsina

Dear Sir,

RE: AFRICAN CONTINENTAL FREE TRADE AREA (AfCFTA) AGREEMENT AND ECONOMIC COMMUNITY OF WEST AFRICAN STATES (ECOWAS) TREATY

We refer to your letter of May 8, 2021, requesting a brief advice on the above subject and hereby make submission as follows:

AfCFTA and ECOWAS

The Africa Continental Free Trade Area (AfCFTA) is an example of a “free trade area,” one of the four main types of regional economic integration.

- Free Trade Area: Member countries remove all barriers to trade within themselves but are free to independently determine trade policies with non-member countries.

Similarities and Dissimilarities Between AfCFTA and ECOWAS:

- Both are examples of customs union.

- Common External Tariff (CET) is only applicable in ECOWAS.

- Both harmonize customs practices.

- Both promote the use of non-tariff barrier reporting mechanisms.

- Both promote related institutional structures that are part of the ECOWAS free trade zone.

- Both are relevant in the areas of trade and customs integration.

Opportunities and Challenges from Implementation of AfCFTA Agreement

Opportunities:

- Trade Creation: More opportunities for member countries to trade by removing barriers to trade and investment.

- Employment Opportunities: Expansion of job opportunities through removal of restrictions on labor movement.

- Consensus and Cooperation: Easier agreements between nations due to regional understanding and similarities.

- Impetus for Private Sector Planning and Investment: Reduces uncertainties, improves credibility, and facilitates private sector planning and investment.

- Non-Economic Benefits: Improved peace and security within the region.

Challenges:

- Trade Diversion: Increased trade with less efficient or more expensive member producers.

- Investment Diversion: Foreign investors from non-member countries may avoid member states due to higher tariffs and regulations.

- Employment Shifts and Reduction: Relocation of production to cheaper labor markets, causing job migration and wage disparity.

- Loss of National Sovereignty: Nations may relinquish political and economic rights.

- Barrier for Non-Members: Non-members face trade barriers within the free trade area.

We hope the above provides insight into the agreement among member nations. Thank you for the opportunity to advise on this subject matter. Please do not hesitate to contact us for further clarification.

Yours faithfully,

Baba Tee

Principal Partner

(c) Country-by-Country Reports (CbCR):

i. Liability to Prepare and Submit CbCR:

- DIY Limited is not liable as it does not meet the definition of a Multinational Enterprise (MNE) group. Specifically:

- It does not operate across jurisdictions as a part of a consolidated group with revenues exceeding €750 million or ₦160 billion.

ii. Relevant Tax Authority:

- Federal Inland Revenue Service (FIRS) for Nigeria as the reporting entity.

- If a surrogate entity in Ghana were involved, the Ghana Revenue Authority would be applicable.