Question

Answer

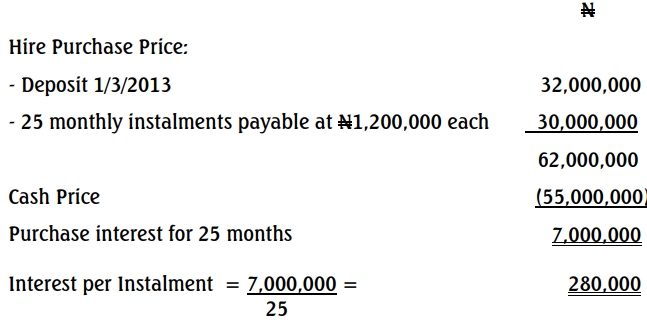

GLOBAL COMPANY LIMITED

COMPUTATION OF HIRE PURCHASE INTEREST

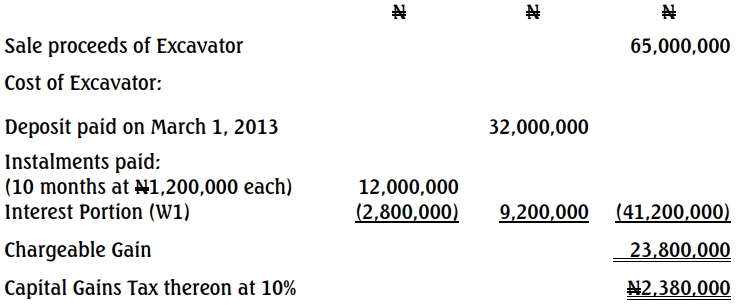

a(i) GLOBAL COMPANY LIMITED

COMPUTATION OF CAPITAL GAINS TAX

FOR ASSESSMENT YEAR 2014

(SALE OF EXCAVATOR ON 1/1/2014)

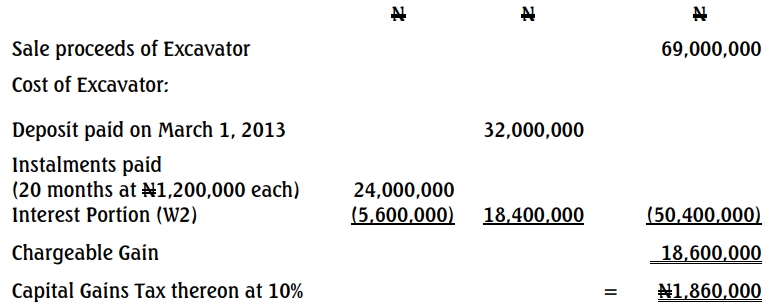

GLOBAL COMPANY LIMITED

COMPUTATION OF CAPITAL GAINS TAX

FOR ASSESSMENT YEAR 2014

(SALE OF EXCAVATOR ON 1/11/2014)

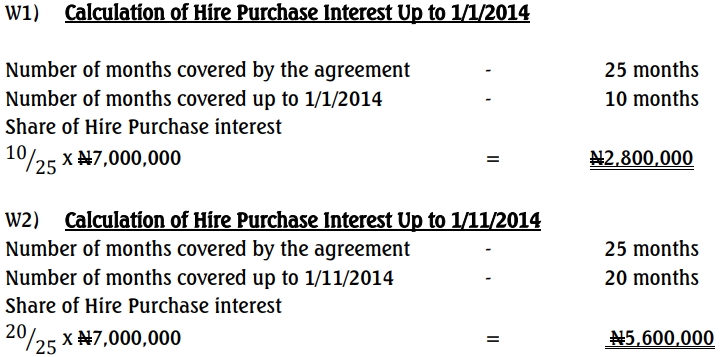

WORKINGS

Comments on Hire Purchase Interest in Capital Gains Tax Computations

- Non-Allowability of Deductions for CGT:

- Expenses or sums that are allowable as deductions in computing the profits or losses of a trade for income tax purposes are not allowable for Capital Gains Tax computations.

- Comparison of Capital Gains Tax (CGT) Liability:

- Based on the earlier computations, the company will incur a higher Capital Gains Tax liability if the property was sold on January 1, 2014, as the gain realized during that period was greater compared to a later sale.

- Treatment of Hire Purchase Costs:

- For tax purposes, the cash price of the asset under hire-purchase terms is considered the acquisition cost.

- The hire purchase charges (interest) are treated as allowable deductions under Section 20 of the Companies Income Tax Act (CITA). These deductions are applied in arriving at the assessable profits for income tax purposes.