Question

Answer

(b)

(ii) Opinion:

- Since the transaction between Dr. Alexander Bold and his wife was a gift, the consideration is deemed to be the amount that would secure the disposal, meaning that no gain or loss would accrue to Dr. Bold. However, since Mrs. Bold later disposed of the property to a third party, a Chargeable Gain arises based on the period of ownership by both Dr. Alexander Bold and his wife.

- When an option is exercised, the consideration paid for the option is incorporated into the total consideration for the asset itself, forming a single transaction for both parties involved. However, if the grantee (buyer) incurs a loss on the disposal of the option, it will not be considered an allowable loss unless the disposal is made at arm’s length to a person not connected to the grantee.

- When consideration (or part of it) is paid in instalments over a period exceeding 18 months from the date of disposal, the Chargeable Gain is deemed to accrue proportionally over the period of the payments. The Chargeable Gain deemed to accrue in each year of assessment is calculated as follows:

Consideration payable in the period× Total Chargeable Gain/ Total Consideration

It should be noted that the Capital Gains Tax Act stipulates that the full amount of consideration for the disposal should be brought into account, without any discount for postponement of payment, the risk of non-recovery of the consideration, or the right to receive any part of the consideration.

- If part of the consideration becomes bad debt, adjustments must be made to the tax liability. If it is later proven to the satisfaction of the relevant tax authority that part of the consideration was not recoverable, a discharge or repayment of tax may occur.

- When a property is acquired by a creditor in satisfaction of a debt, the property is not considered disposed of by the debtor, nor is it acquired by the creditor (in this case, Mr. Saxon) for a consideration greater than its market value at the date of acquisition.

- If the creditor (Mr. Saxon) later disposes of the property, and no Chargeable Gain arises from the initial acquisition of the property by the creditor, the gain on the disposal will be adjusted, so that it does not exceed the gain that would have accrued if the creditor had acquired the property for a consideration equal to the amount of the debt.

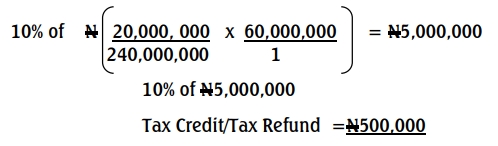

(iii) Bad Debt Payment by Mr. Clyde:

On the issue of the bad debt payment by Mr. Clyde, Bold and Wife Limited would need to demonstrate to the Federal Inland Revenue Service that the N20 million of the sales proceeds has become bad debt. If accepted, the company would be entitled to a tax credit or a tax refund of N500,000, which represents the Capital Gains Tax on the Chargeable Gain arising from the bad debt of N20 million.

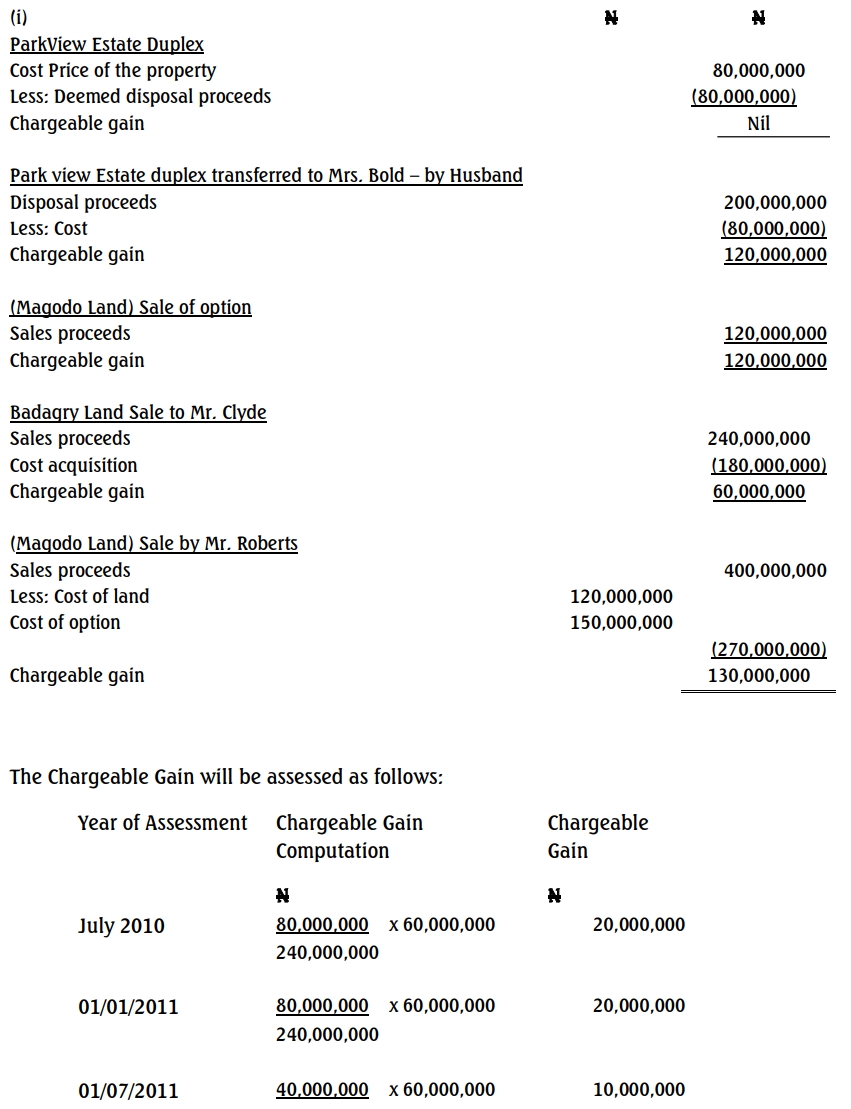

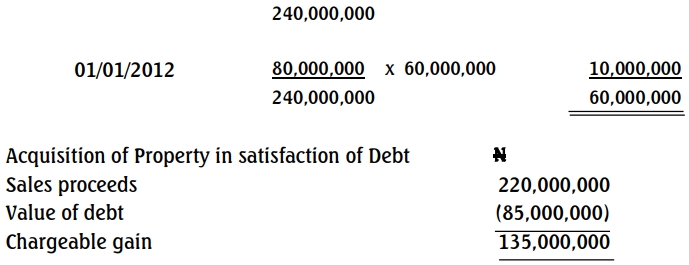

Workings: