Question

Answer

a) Financial evaluation of the two options.

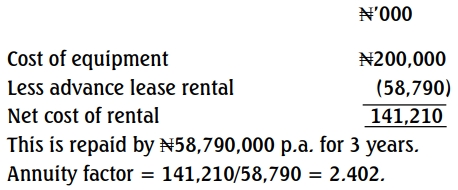

Scheme A. The relevant cost is simply the cost of the equipment i.e. ₦200million

Scheme B. Finance lease – a number of steps are needed here:

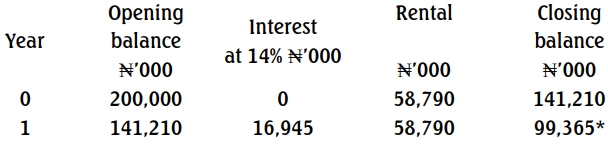

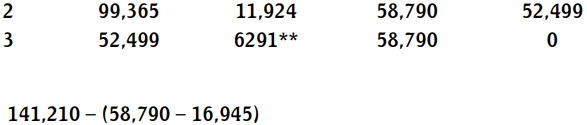

i) Implied interest rate

The implied interest rate on the lease is computed as follows:

From the annuity tables, a 3-year cumulative present value of 2.402

corresponds to approximately 12%. Therefore, the implied interest on the lease is 12%.

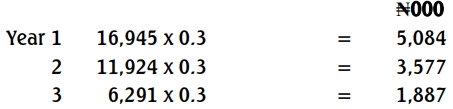

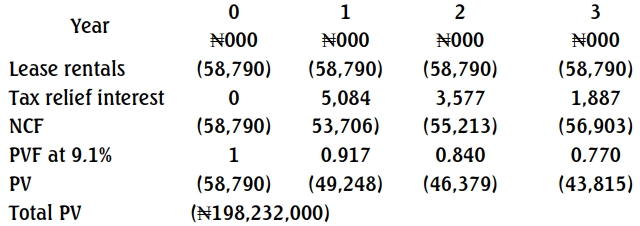

iii) Tax savings on interest

iv) Discount rate. The discount rate to use is the cost of borrowing, net of tax = 13 (1 – 0.30) = 9.1%

v) NPV of lease option

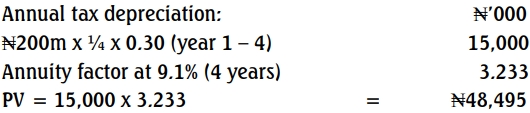

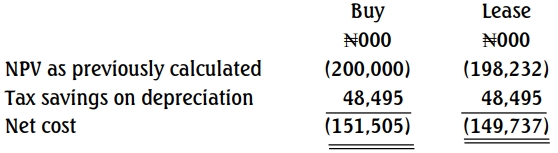

Note: The above calculations are based on differential cash flows. We have therefore ignored tax savings on tax depreciation. Whether the company buys the equipment by borrowing or adopts a finance lease, it is entitled to tax depreciation on the equipment. If the relevant tax savings are incorporated into the analysis, the result will be as follows:

It is clear that the relative position of the two alternatives remains the same.

Conclusion: The leasing option offers a cost savings of ₦1,768,000 relative to the purchase option and it is therefore the preferred option.

b) Discount Rates for Financing Decision:

The two primary discount rates to consider are:

When evaluating the investment in the equipment, project-specific risks will already have been accounted for. The analysis in part (a) is intended to support the financing decision, not the investment decision. Therefore, cash flows should be discounted using either the WACC or a project-specific discount rate when evaluating the investment decision. This is because the project is financed through a mix of the company’s debt and equity resources. However, the financing decision is separate, and the discount rate should be chosen accordingly.

For financing decisions, we typically use the cost of debt as the baseline. Other financing options, such as leasing, should be compared against the cost of debt, which serves as the discount rate. The post-tax cost of debt reflects the opportunity cost of leasing and can be used to discount the incremental cash flows that arise from leasing, in comparison to buying the equipment outright.

Alternatively, leasing could be used as the baseline for comparison, and the post-tax implied cost of leasing could be used as the discount rate. However, in practice, it is generally simpler to discount cash flows using the post-tax cost of debt.