Question

Answer

(a)

i. Capital Gains Tax

Capital Gains Tax is a charge on capital gains accruing to an individual or organization on the disposal of a capital asset (chargeable asset). The current rate, as provided for in the Capital Gains Tax Act Cap CI LFN 2004 (as amended), is 10%. The tax is charged on the gains on an actual or current year basis.

The tax is administered by the Federal Inland Revenue Service (FIRS) for individuals resident in the Federal Capital Territory and corporate bodies, while the State Board of Internal Revenue administers the tax for individuals resident in the respective states.

ii. Withholding Tax

This is an advance payment of tax, used as a tax credit for settling the income tax liability of the particular year to which the income suffering the deduction relates.

Withholding Tax is deductible at the point of payment or when credit is taken, whichever comes earlier. Tax withheld must be remitted within 30 days from the date the duty to deduct arises.

The Federal Government, through the Federal Inland Revenue Service, collects Withholding Tax from residents of the Federal Capital Territory and corporate bodies, while State Governments, through their respective State Internal Revenue Boards, assess and collect Withholding Tax from individuals only.

Penalty for Non-Deduction/Non-Remittance of Withholding Tax:

For failure to deduct or remit within 30 days, a company or individual shall be liable to:

- A penalty of 10% of the tax not deducted/remitted.

- Interest at the prevailing Central Bank of Nigeria minimum rediscount rate.

- Imprisonment for a period not exceeding three years.

iii. Double Taxation Treaty

When a Nigerian company earns foreign income, such income is included in its Chargeable Profit for the year of assessment and subjected to Nigerian tax. However, in many cases, the foreign income would have already been taxed in the country where it was derived. This results in double taxation, as the same income is taxed in two jurisdictions.

To minimize the negative effects of double taxation on international trade and attract foreign investment, Nigeria has signed bilateral tax treaties with various countries. These treaties provide reliefs to Nigerian companies earning foreign income that has already been taxed abroad.

iv. Multiple Taxation

This occurs when more than one tier of government imposes taxes or levies on the same income, assets, or financial transactions.

(b) Government’s Efforts to Reduce Cases of Multiplicity of Taxes:

i. The Federal Government issued Decree No. 21 (now an Act) under the Laws of the Federation of Nigeria 2004 on Taxes and Levies (Approved List for Collection) No. 21 of September 30, 1998.

ii. The schedule outlines the taxes and levies to be collected by the Federal Government, State Governments, and Local Governments.

iii. The Constitution provides that no tax should be imposed on the same person by more than one State or in respect of the same income by more than one Local Government.

(c) Legislative Powers on Tax Matters:

The power to legislate on taxation rests with:

- The National Assembly (consisting of the Senate and the House of Representatives).

- State Governments (through their respective State Assemblies).

The National Assembly can delegate assessment and collection duties to a State Government, while a State Assembly may delegate the power to administer and collect any tax, fee, or rate to a Local Government. However, there must be an assurance that no tax or fee at a stipulated rate is levied on the same person in respect of the same income by more than one Local Government.

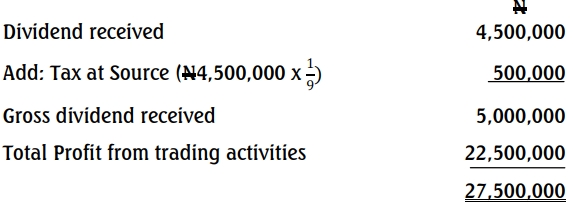

(d) Since Rex Pharmaceuticals Limited received N4,500,000 from Laiketop Limited net of tax, the amount received is regarded as Franked Investment Income and is not subject to further tax