Question

The managers of a pension fund follow an active portfolio management strategy. They try to purchase shares and bonds that show a positive abnormal return (positive alpha factor in the case of shares). The pension fund is required by law to hold at least 40% of its investments in bonds. N100million is currently available for

investment. Three shares and three bonds are being considered for purchase. The required return on bonds may be measured using a model similar to the capital asset pricing model, where beta is replaced by the relative duration of the individual bond (Di) and the bond market portfolio (Dm) i.e. Di/Dm.

Note: Assume the risk-free rate is 4 percent per year.

Required:

a. Evaluate whether or not any of the shares or bonds is expected to offer a positive abnormal return. (10 Marks)

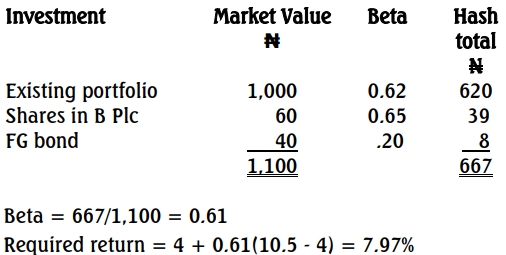

b. The pension fund currently has the maximum permitted investment in shares and wishes to continue this strategy. It has a market value of N1,000 million and a beta of 0.62.

Required:

Calculate the required return from the pension fund if any shares and bonds with positive abnormal returns are purchased. State clearly any assumptions that you make. (4 Marks)

c. Discuss possible problems with the pension fund’s investment strategy. (6 Marks)

Answer

a) A positive abnormal return will exist if the expected return from a security is

higher than the required return. This may be established by using the Capital

Asset Pricing Model (CAPM).

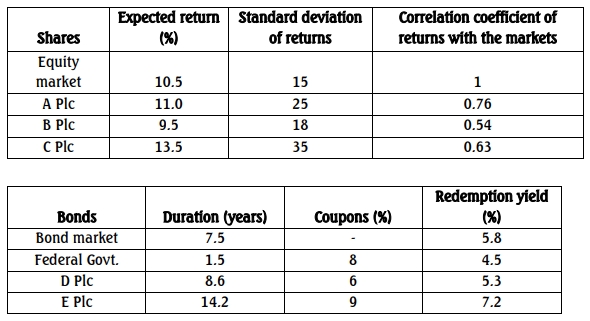

The beta of the individual share may be found using:

If these data are accurate, the shares of B Plc. and the Federal Government bond offers a positive abnormal return.

b) The beta of the revised portfolio is the weighted average of the betas of the components of the portfolio.

c. Discussion of Possible Problems with the Strategy

- Regulatory Constraints:

- The fund must hold at least 40% in bonds, limiting flexibility to maximize returns from shares.

- Interest Rate Risk:

- Bonds are highly sensitive to interest rate changes, which could impact valuation and returns adversely.

- Active Management Costs:

- Active portfolio management incurs higher transaction and research costs, potentially offsetting gains from abnormal returns.

- Market Timing Risk:

- The strategy assumes the ability to consistently identify securities with positive alpha, which is inherently uncertain.

- Diversification Limitations:

- Over-reliance on shares with high alphas and limited bonds could expose the fund to sector-specific or systematic risks.