Question

Answer

(a) Accounting Treatment of Agbinye Farms.

The relevant standards for consideration here are:

IAS 41- Agriculture

IAS 2 – Inventory

IAS 16 Property, plant and equipment

IAS 41 Agriculture outlined assets that are outside of its scope. This includes

– Bearer plants

Bearer plants are used to produce agricultural produce for more than one period. Examples include grape vines or tea bushes. Bearer plants are accounted for in accordance with IAS 16 Property, Plant and Equipment. However, any harvested produce growing on a bearer plant, such as grapes on a grape vine, is a biological asset and so it is accounted for in accordance with IAS 41.

– Land related to agricultural activity.

Land is not a biological asset. It is treated as a tangible non-current asset and accounted for under IAS 16-Property, Plant and Equipment. When valuing a forest, for example, the trees must be accounted for separately from the land that they grow on. As explained above Agbinye farms operates a plantation, this should be accounted for in accordance with property plant and equipments.

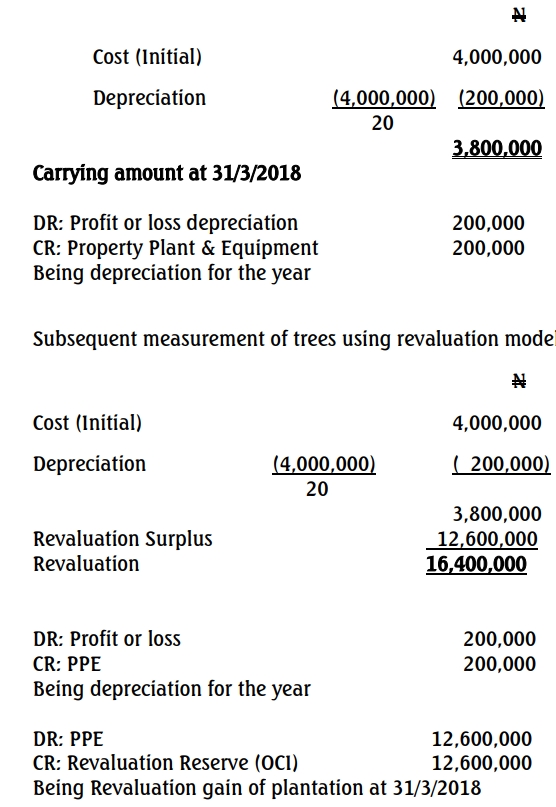

Accounting Treatment

Initial Measurement of Land

The initial cost of land is N12m

– Subsequent Measurement of Land

For land it remains the same at N12m in the statement of financial position

as at 31 March, 2018 since land cannot be depreciated.

– Initial Measurement of Trees (Plantation)

The N4m operating cost of planting the trees should be taken as the initial

cost of PPE i.e the Plantation.

– Subsequent Measurement of Trees (Plantation) using cost model

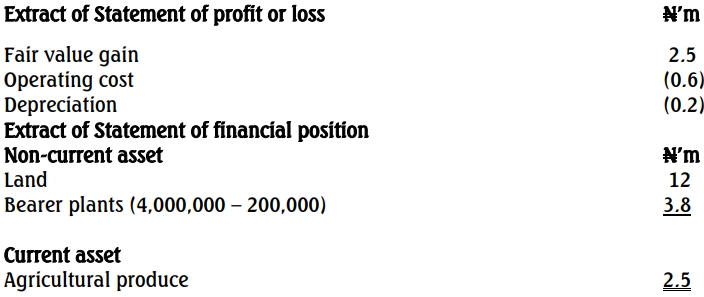

Agricultural Produce

The produce growing from the trees in the plantation are biological assets. They should initially be recognised at fair value less costs to sell. Any gain or loss on initial recognition is reported in Statement of profit or loss and be revalued at the year end to fair value less costs to sell with any gain or loss reported in profit or loss

Therefore, in Agbinye farms, the harvested produce are agricultural produce and should be accounted for in line with provisions of IAS 41.

Initially recognised at N1.9m (2.5m – 0.6m), with a gain of N1.9m reported in profit or loss, the harvested grapes are now accounted for under IAS 2 Inventories and will have a deemed cost of N1.9m.