Question

The following is the statement of financial position of Lagos Plc as at 31 December, 2013, with its immediate two comparative years.

The management of Lagos Plc is not sure of the impact of IAS 12 (Income Taxes) on its retained earnings as at 31 December, 2013, as well as what the new deferred tax balance will be on migrating to IFRS.

The following information was also available as at the year-end:

| Details | Value (N’000) |

|---|---|

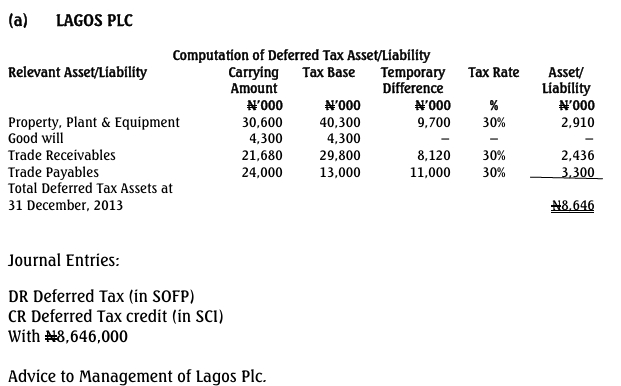

| Tax written down value of PPE | 40,300 |

| Tax written down value of goodwill | 4,300 |

| Tax base of trade receivables | 29,800 |

| Tax base of trade payables | 13,000 |

Assume that current tax has been correctly computed in line with the applicable tax laws at 30%.

Required:

Using relevant computations, advise the management of Lagos Plc on the impact of deferred tax calculated on retained earnings in accordance with IAS 12.

Answer

Deferred Tax Computation and Impact

- Deferred Tax Asset:

- Temporary differences in Lagos Plc’s deferred tax computation resulted in deductible temporary differences, creating a total deferred tax asset of N8.646 million as at 31 December 2013.

- Required Treatment:

- The deferred tax asset should be debited to Deferred Tax Assets (DR) and credited to Retained Earnings (CR), provided it is probable that future taxable profits will be available to utilize this deferred tax asset.

- Effect on Financial Statements:

- The deferred tax asset will increase the Non-Current Assets of Lagos Plc in the Statement of Financial Position by N8.646 million as at 31 December 2013.

- Retained earnings will increase by the same amount in the Statement of Changes in Equity.

- Classification:

- The deferred tax balance will be classified as a Non-Current Asset in the Statement of Financial Position.

This advice ensures compliance with IAS 12 while accurately reflecting the financial position and equity of Lagos Plc.