Question

Answer

a) Gaps Plc‟s cost of capital on December 2019 = 3 + (1.1 × (8 – 3)) = 8.5%

b) i) A 1 for 2 rights issue will require 320/2 = 160 million new shares to be issued.

The price per share = ₦560 million/160 million = ₦3.50

A discount on the current market price of (₦5 – 3.50)/5 = 30% (or ₦1.50).

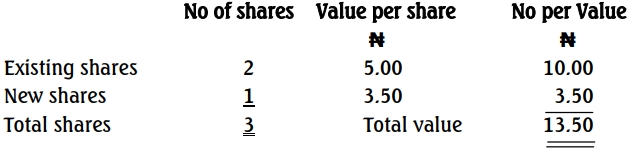

ii) The theoretical ex-right price is:

Theoretical ex-rights price = ₦13.50/3 = ₦4.50

iii) The actual share price will depend on the market‟s reaction to the rights issue e.g. whether it is fully taken up, and whether the proceeds are invested in positive net present value projects. If we were told the net present value of the projects, this could be incorporated in the theoretical ex-rights price of ₦4.50, giving a more realistic estimate of the actual share price post rights issue.

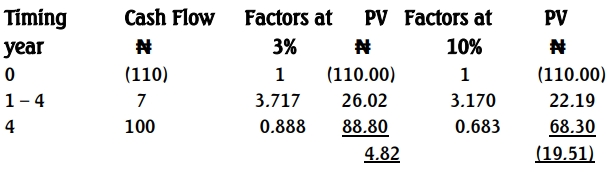

c) (i) The yield to maturity of the Eko Ventures bonds is calculated as follows:

IRR = 3 + (4.82/(4.82 + 19.51) × 7 = 4.39% say 4%

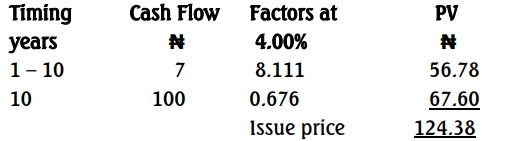

The issue price is:

The total nominal value will be = 560/(124.38/100) = ₦450.23 million

ii) EV has similar risk to GP so it may be reasonable to assume that bond holders would require the same yield to maturity (YTM) in return for investing with either company. But how similar is similar? Eg, how comparable is EV to GP in terms of gearing? However, the EV bonds have only four years until redemption, whilst the GP bonds mature in ten years. It is likely that bond holders would require a higher yield to redemption for investing in the GP bonds to compensate them for the risk of investing for a further six years.

d) The Gearing and Interest Cover Ratios of GP Immediately After the Bond Issue

Interest Cover:

- Interest: ₦450.23 × 7% = ₦31.52m

- Interest Cover: (₦200 / ₦31.52) million = 6.35 times

Gearing by Market Values Assuming the Current Market Price Per Share:

- Market Capitalisation: 320 × 5 = ₦1,600 million

- Gearing (D/E): 560 / 1,600 = 35%

In Time:

Both interest cover (more operating profits) and gearing (greater equity value) are likely to improve with:

- Acceptance of positive NPV projects

- Any favourable market reaction to the issuance of debt and its tax shield

An Outline of General Advantages and Disadvantages of Debt vs Equity

- Control: If all the rights are not taken up by the existing shareholders, there will be dilution of control. Debt issuance has a neutral effect on control.

- Cost: Debt should have a lower cost of capital due to:

- Lower risk (both income and capital repayment)

- The fact that interest on debt is allowed for corporate tax

- Security: Providers of debt finance will usually require some form of tangible security for any debt capital.

- Cash Flows: While debt finance is cheaper than equity, it places mandatory payment obligations on the company for interest. Payment of dividends depends on the availability of cash flow.

- Issue Cost: Generally, it is cheaper to issue equity (especially rights issue) than bonds.

EPS (Earnings Per Share) Calculations

- Current EPS: ₦160m / 320 = 50k

- EPS with Rights Issue: ₦160m / 480 = 33k

- EPS with a Bond Issue:

- Adjusted earnings after tax: ((₦200m – 31.52) × 0.80) = ₦134.78m

- EPS: ₦134.78m / 320 = 42k

Addressing the Concerns of the Board

The company will have:

- A gearing ratio of 35%, which is between the industry maximum (40%) and average (30%).

- An interest cover of 6.35 times, which is slightly above the industry average of 6.

- Since this is the first time GP has borrowed, both shareholders and the stock market might be concerned. They might prefer these ratios to be around or better than the industry averages.

- Borrowing should reduce the current 8.5% cost of capital, since:

- Debt is generally less expensive than equity as it is less risky for debt holders.

- The company receives tax relief on interest paid.

- Increased financial risk may cause shareholders to require a higher return, but this is unlikely to offset the cheaper proportion of debt finance.

- Company Value: The value should increase due to:

- Reduction in the cost of capital

- New funds being invested in positive NPV projects

Advice

It would be prudent for the company to:

- Restrict its borrowing to the industry average gearing level, especially since its interest cover is slightly above the industry average.

- Avoid borrowing the full ₦560 million.

- Revise its plans for raising the finance, such as:

- Issuing both debt and equity to ensure gearing and interest cover ratios are more favourable.

- Selling surplus assets.