Question

Answer

(a) Circumstances under which a non-resident company will be assessable to tax in Nigeria

The circumstances include:

- Income derived through a fixed base or permanent establishment.

- Income derived in Nigeria through a dependent agent.

- Income derived from supervisory activity that lasts more than three months.

- Income derived in Nigeria from a turnkey project.

- Income derived from professional consultancy, management, and technical services rendered in Nigeria.

- Income derived from investment such as dividends, interest, rent, and royalties (with withholding tax deducted as final tax).

- Income derived from a contract awarded to a Nigerian company but subcontracted to a non-resident company.

- Where the non-resident company has a significant economic presence in Nigeriab) Computation of Tax Liabilities for Gen Power Incorporated

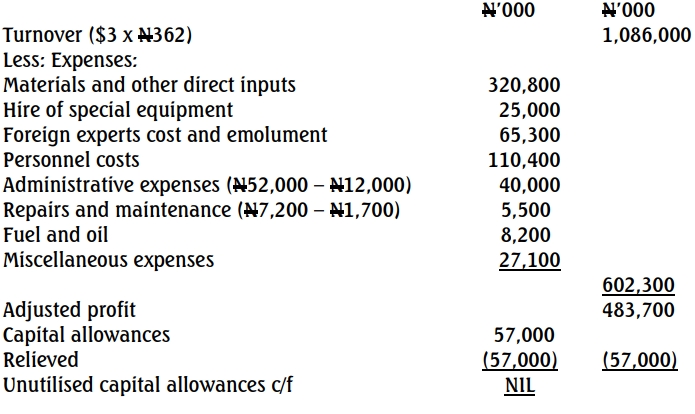

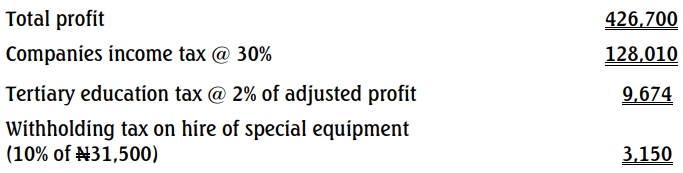

(b) Gen Power Incorporated

Computation of tax liabilities

For 2019 year of assessment