Question

Answer

ECOBAF Consult Services

Plot 8, Ahmadu Road, Bauchi

April 13, 2022

The Managing Director

Maigona Agro Limited

99, Eyimba Road

Bauchi

RE: ADVICE ON TAX IMPLICATIONS OF PROFIT MADE BY BAM TEXTILE MILLS, UK

We refer to our discussion of April 6, 2022 on the above subject-matter and our comments are as follows:

(a) Tax implications of the overseas branch- BAM Textile Mills, UK are:

i. The provisions of Nigerian tax laws as set out in the Companies Income Tax Act 2004 (as amended) on profit of an overseas branch of a Nigerian company is that such profit is deemed to be derived in Nigeria and is therefore liable to tax in Nigeria;

ii. Any foreign tax suffered is not allowable in determining the overseas profit;

iii. Assets in use in such a branch will be entitled to capital allowances claimed in Nigeria;

iv. Losses incurred from such a branch can be set off against profit in Nigeria provided the losses were incurred from the same source; and

v. Double taxation relief is available for any foreign tax suffered either based on bilateral agreement or based on tax relief available under the Commonwealth.

Since it is a fact that BAM Textile Mills, UK is a branch of a Nigerian company, the above provisions of the Act are applicable, and profit made is fully liable to tax in Nigeria.

(b) Computation of tax liabilities of the corporation:

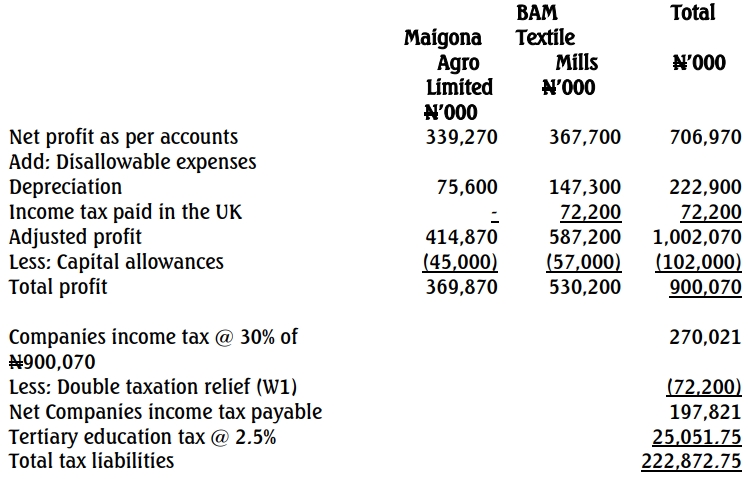

i. Following the provisions of the Act in respect of the status of BAM Textile Mills, the adjusted profit of N587.2 million from its operations is liable to tax in Nigeria.

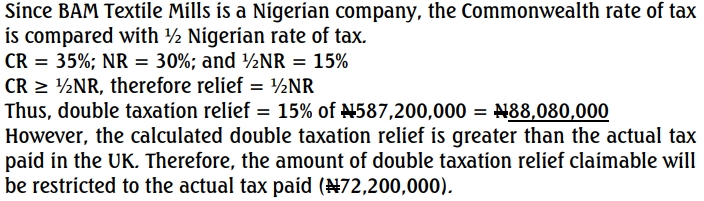

ii. However, due to existing Commonwealth taxation relief between Nigeria and the UK, the profit is available for double taxation relief of N88.080 million (but restricted to actual tax paid in the UK, N72.2 million).

iii. The relief helps in reducing the companies income tax liability from N270.021 million to N197.821 million. All these computations are shown in the attached Appendix 1.

Please do not hesitate to contact us if you need any further clarification on the above subject.

Yours faithfully,

Oluyemi Ukah

Principal Partner

For: ECOBAF Consult Services

Appendix 1: Computation of tax liabilities of the corporation

Workings

(1) Computation of double taxation relief