Question

Answer

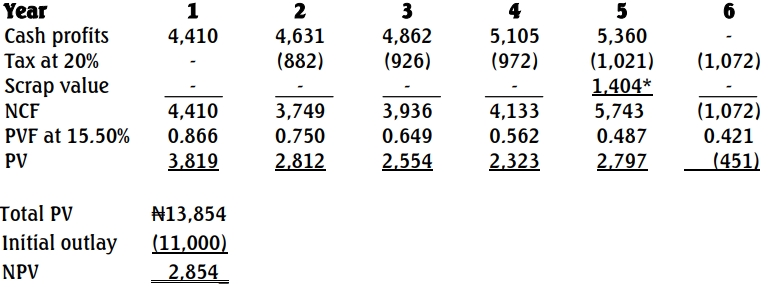

a) i)

Expected annual sales (₦000) = (16,000 × 0.25) + (12,000 × 0.5) + (8,000 × 0.25) = ₦12,000

Expected annual contribution = ₦12,000 × 0.5 = ₦6,000

Expected annual cash profit = ₦6,000 – 1,800 = ₦4,200

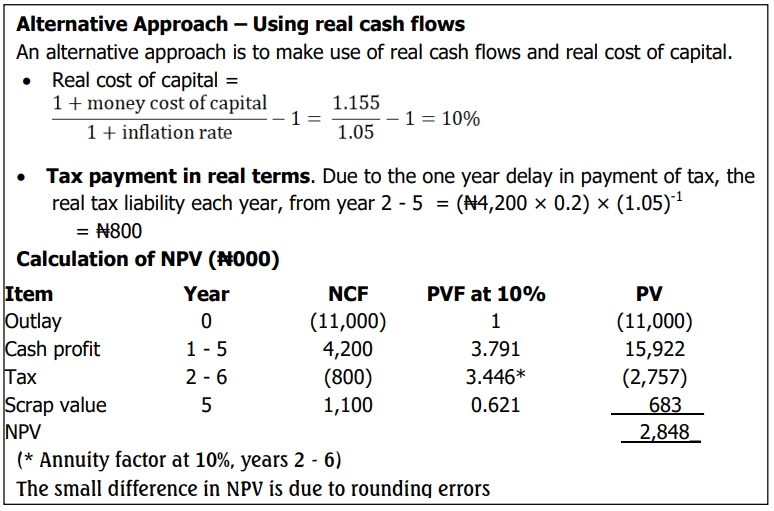

All the above figures are in real terms. Due to the one-year delay in the

payment of tax, the cash profits will be converted to money cash flows and

tax calculated on the money cash profits. The money cash profits are

expected to grow annually by the rate of inflation of 5%.

Calculation of NPV (₦000)

(* = 1,100 × (1.05)5 = ₦1,404)

Recommendation

The project has a positive NPV and if other factors are held constant, it should

be accepted.

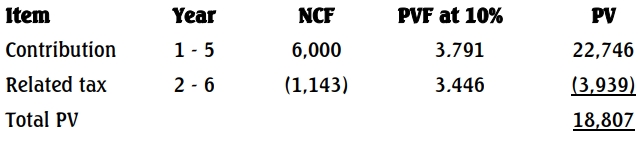

ii) Sensitivity – contribution

– Using real cash flows approach (₦000)

Annual real contribution = ₦6,000

Related annual real tax (Years 2 – 6) = ₦6,000 × 0.2 × (1.05)-1 = ₦1,143

Calculation of present value

Sensitivity = NPV/PV of contribution = ₦2,848/₦18,807 = 15.14%

This means that the total annual contribution can drop by maximum of 15.14% to avoid negative NPV.

Thus, the minimum annual contribution = ₦6,000,000 × (100% – 15.14%) = ₦5,091,600.

Sensitivity – tax rate

– Using real cash approach (₦000)

Sensitivity = NPV/PV of tax

= ₦2,848/2,757 = 103.30%

This means that the tax rate can increase by maximum of 103.30% if the project is to remain viable. The maximum tax rate is therefore: 20% × (100% + 103.30%) = 40.66%.

This means that if the project is to remain viable, the maximum tax rate allowed is 40.66%

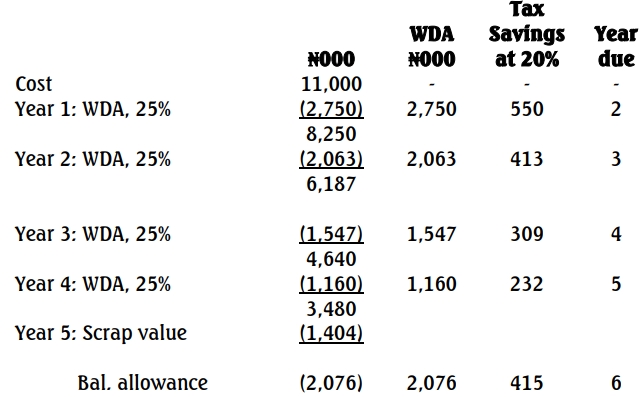

b) Computation of written down allowances

Calculation of PV (₦000)

Total PV = ₦1,143 or ₦1,143,000

This means that the NPV of the project will increase by ₦1,143,000 as a result of tax savings associated with written down allowances.