Question

You are the Financial Controller of Gongon Group. On January 2, 2021, you are busy preparing the financial statements for the year ended December 31, 2020. You are under a lot of pressure as you have been asked to present the draft financial statements to the Board of Directors in two days’ time.

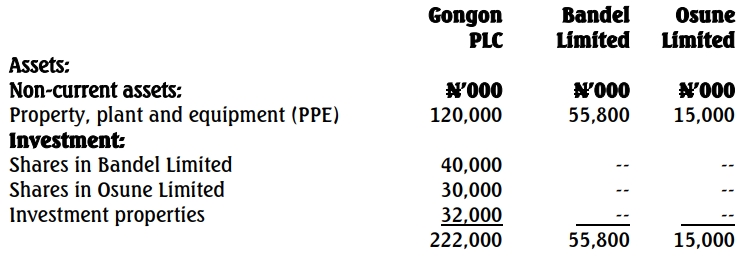

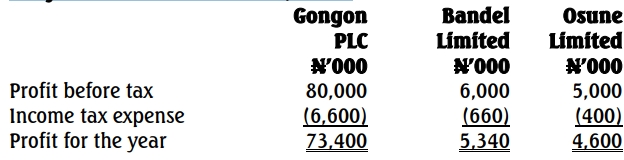

The first draft of the financial statements for each of the three companies has been prepared and is now on your table. You have also compiled a list of outstanding issues that you need to consider before presenting the financial statements to the Board.

Outstanding Issues:

Answer

(a) First Issue

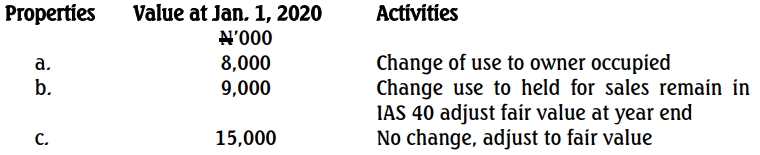

There are three properties to consider. These are:

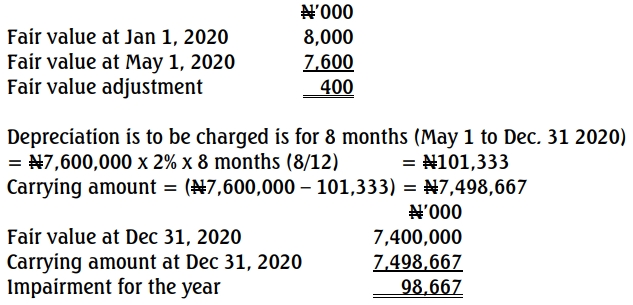

Property „A‟

– In accordance with IAS 40, a transfer from investment property carried at fair value to owner occupied property, the fair value at the date of change of use is deemed to be the „cost of the property under its new

classification.

– The cost will then be depreciated in accordance with the company‟s

accounting policy.

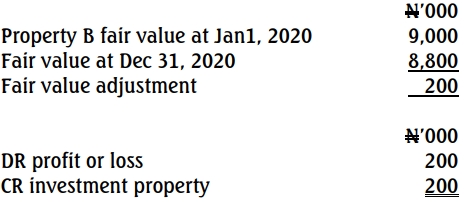

Property „B‟

– Property „B‟ held for sale as at December 31, 2020. Property „B‟ should continue to be presented as Investment property under IAS 40 until it is disposed of IFRS 5 – Non-Current Assets Held for Sale and Discontinued Operation does not apply here.

– However, property „B‟ will be adjusted to fair value as at December 31,

2020 as follows:

Being loss on fair value adjustment taken to profit or loss Property „C‟

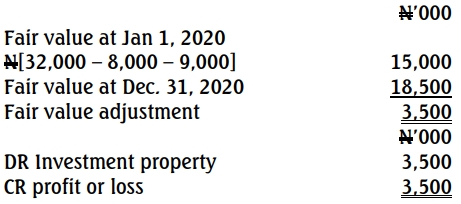

– There is no change in the use for property „C‟

– It only needs to be restated to fair value at the year end

Being gain on fair value adjustment on reinstatement transfer to profit or

loss

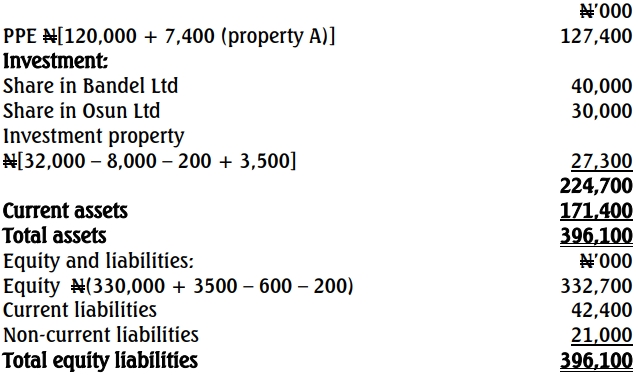

Gongon PLC

Revised adjustments to draft statement of financial position

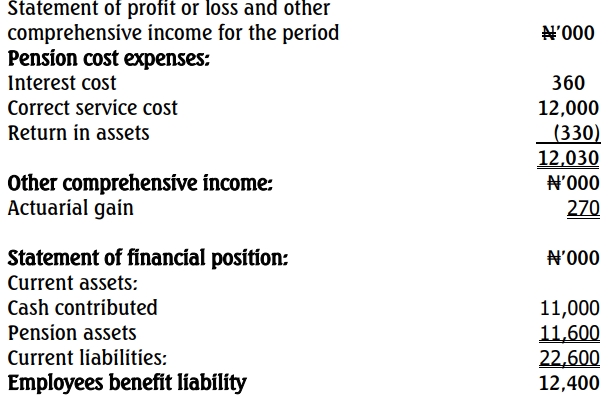

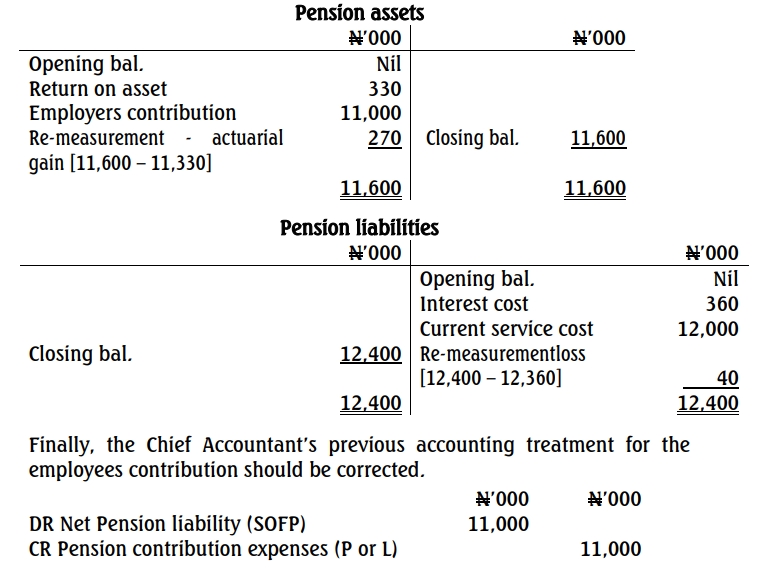

b. Second issue

- The applicable accounting standard is IAS 19 (Employee Benefits).

Gongon’s pension scheme qualifies as a defined benefit plan since the company has an obligation to provide agreed post-employment benefits and assumes both actuarial and investment risks associated with the scheme. - The accountant has incorrectly accounted for the scheme by simply recognizing the employer’s contribution in the statement of profit or loss.

- Under IAS 19, defined benefit liabilities and assets must be recognized on the statement of financial position at the net amount of:

Present Value of Obligation – Fair Value of Plan Assets (at the reporting date).

- A defined benefit plan also incurs current service costs and net interest expenses, which should be recognized in the profit or loss.

- Additionally, any actuarial gains or losses arising from remeasurement of the defined benefit liabilities or assets must be recognized in other comprehensive income (OCI).

Being correction on the acquisition treatment of pension contribution

Financial statements extract