Question

Answer

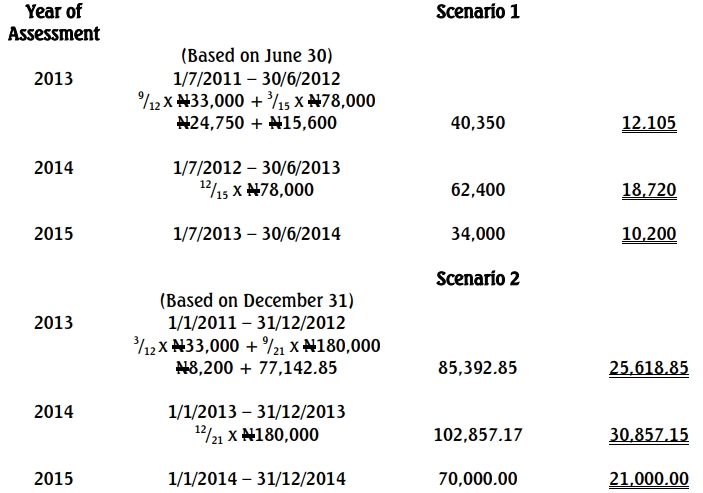

(b)

GRINGRIN NIGERIA LIMITED

COMPUTATION OF TAX LIABILITIES

ASSESSMENT YEARS 2013, 2014 and 2015

(b)

GRINGRIN NIGERIA LIMITED

COMPUTATION OF TAX LIABILITIES

ASSESSMENT YEARS 2013, 2014 and 2015