Question

Answer

ToksBlaqy & Co. (Tax Consultants)

20, Camp Road, Abeokuta

January 22, 2021

To: The Managing Director, COLENDS Nigeria Limited, Abeokuta

Subject: Connected Persons, Artificial Transactions, and Tax Computation

We refer to your memo dated January 10, 2021, and our meeting with the company’s management on January 12, 2021, seeking our services as tax consultants to address the subject matter. Our comments are as follows:

a. Connected Persons and Artificial Transactions

The concept of connected persons and artificial transactions in tax practice is explained as follows:

- Connected Persons: Certain persons are treated as so closely involved that transactions between them need to be viewed as if they are the same person or considered differently from those at “arm’s length.”

- Artificial or Fictitious Transactions: Transactions between connected persons may be considered artificial for determining tax liability, allowing tax authorities to make necessary adjustments to prevent reduced tax liability.

- Adjustments by Revenue Service: The Revenue Service may counteract reductions in tax liability from such transactions by making necessary adjustments.

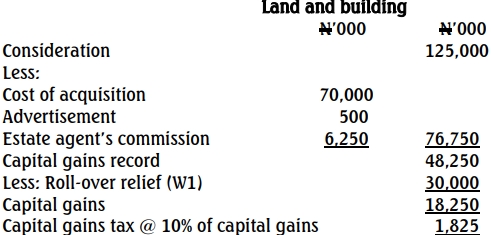

- Capital Gains Tax Act Provisions: Section 23 of the Capital Gains Tax Act 2004 (as amended) specifies that transactions between connected persons must be treated as occurring outside the “bargain at arm’s length” principle, with considerations adjusted to market value.

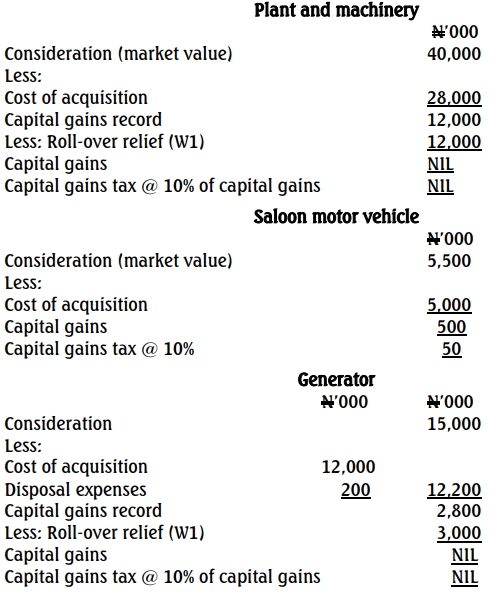

- Specific Company Transactions: The disposal of Colends Nigeria Limited’s plant and machinery to a subsidiary and the saloon vehicle to the General Manager are clear examples of artificial transactions, as these persons are connected to the company. The Revenue Service therefore substituted the proceeds received (₦32 million for machinery and ₦3.5 million for the car) with their market values (₦40 million and ₦5.5 million, respectively).

b. Tax Implications on Transactions Executed

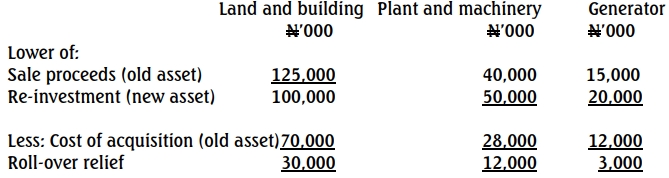

- Roll-over Relief Eligibility: Section 32 of the Capital Gains Tax Act allows for roll-over relief on qualifying assets. Relief is granted if consideration from the disposal of an old asset, used exclusively for trade, is reinvested in a similar new asset.

- Roll-over Relief Deduction: The roll-over relief is deducted from capital gains before determining capital gains tax payable.

- Asset Eligibility for Roll-over Relief: All disposed assets, except the motor vehicle, qualify for roll-over relief.

- Tax Liabilities Summary:

- Land and Building: ₦1,825,000 as capital gains tax

- Plant and Machinery: ₦0 (roll-over relief applied)

- Saloon Motor Vehicle: ₦50,000 capital gains tax

- Generator: ₦0 (roll-over relief applied)

Total Tax Payable: ₦1,875,000.

If further clarification is needed, please contact us.

Yours faithfully,

Abiodun Bambam

Senior Tax Consultant

For: ToksBlaqy & Co. (Tax Consultants)

Schedule 1: Computation of Capital Gains Tax Liability

(ii) Computation of roll-over relief