Question

Answer

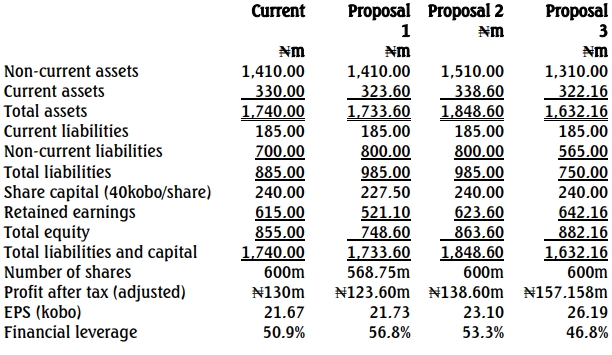

a) Forecast Financial Position – Yinko Plc

Working Notes

Proposal 1

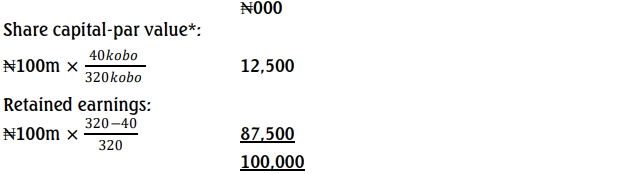

Debt is increased by ₦100million and shareholders fund reduced by the same amount as follows:

(* Only the par value can be removed from share capital. This is very important please)

This is taken from retained earnings.

Balance of retained earnings

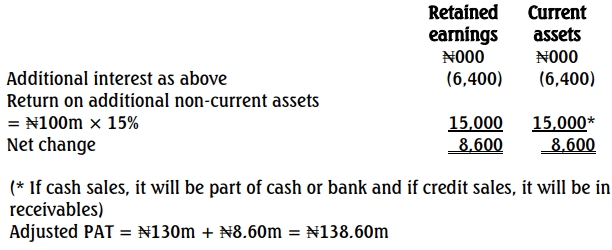

= ₦615m – (87.50m + 6.40m) = ₦521.10m

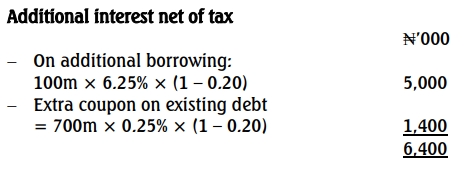

Furthermore, the additional interest of ₦6.40m is taken off current assets because presumably it is paid out of cash.

Balance of current assets = 330m – 6.40m = ₦323.60m

The alternative is to assume that the additional interest has not been paid and therefore taken to interest payable in current liabilities. That leaves current assets constant at ₦330m and increases current liabilities to ₦191.40m.

Adjusted PAT = ₦130m – 6.40m = ₦123.60m

Proposal 2

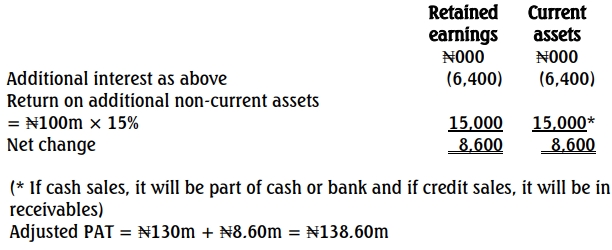

Borrowing of ₦100m increases non-current assets and non-current liabilities

by the same amount.

Retained earnings and current assets are impacted as follows

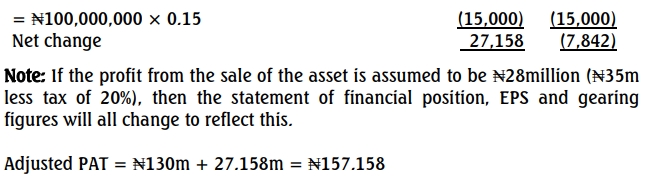

Proposal 3

Non-current assets are reduced by ₦100m (the net book value of the assets sold). The profit on disposal of ₦100m increases retained earnings (through profit and loss account). The net change in retained earnings and current assets are as follows:

b. Proposal 1 appears to produce opposite results compared to the other proposals. This proposal would lead to a small increase in the earnings per share (EPS) due to a reduction in the number of shares. However, the level of gearing would reduce substantially, by about 12%.

With Proposal 3, overall profits would increase because the profit from the sale of assets combined with interest savings outweighs the lost earnings from downsizing. This proposal also results in the lowest gearing level.

Proposal 2 would significantly boost the EPS from 21.67 kobo to 23.10 kobo, primarily due to increased earnings through extra investment. However, the amount of gearing would increase by more than 4.7%.

Overall, Proposal 1 appears to be the least attractive option. The choice between Proposals 2 and 3 would depend on the sustainability of earnings versus reduced gearing. Proposal 3 may not be sustainable because the profit from asset sales is a one-off transaction.

Other factors to consider include the capital structure of competitors, the reaction of the equity market to the proposal, the implications of the change in the company’s risk profile, and the resultant impact on the cost of capital.