Question

Answer

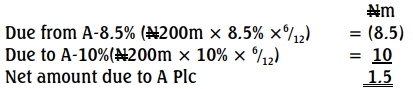

Suppose that on the first re-set date for the swap, at the end of month 6

in the first year, 6-month NIBOR is 10%. The payment due to each party to

the swap will be as follows:

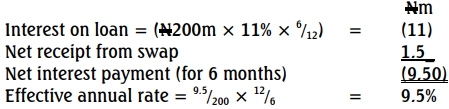

A Plc will receive this amount six months later at the end of 12 months of

the first year- rates are fixed in advance and payments made in arrears. A

plc will pay interest on its cash market loan at NIBOR + 1% which for this six-month period is 11% (10% + 1%). Taken with the amount received under the swap agreement, the net cost to A Plc is equivalent to interest payable at 9.5%.

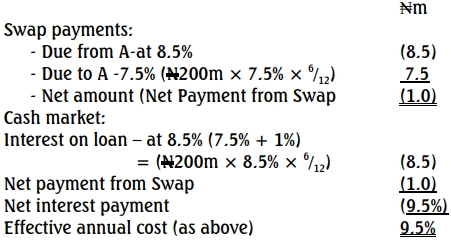

ii) NIBOR 7.5%

With the principles set up above, we can speed up the calculations as

detailed below: