Question

Answer

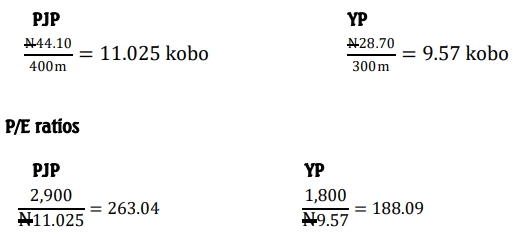

a) PJP currently has 400 million ordinary shares, and Fader 300 million.

Earnings per share:

b) A 2-for-3 share exchange will result in the issue of 300 million x 2/3 new shares, or 200 million shares, giving a total of 600 million shares.

Increasing earnings per share alone is not enough. The effect on the market value is the crucial factor. When a relatively high P/E company acquires a company with a lower P/E, the expected earnings per share will increase, but not necessarily the total market value of the companies.

c) i) The current combined value of the two companies is:

(400m shares x ₦29) + (300m shares x ₦18) = ₦17 billion.

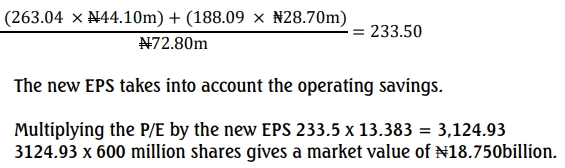

If the market is efficient, ignoring any synergistic or other effects of the

takeover, the post-acquisition P/E will be the weighted average (by earnings) of the current P/E ratios.

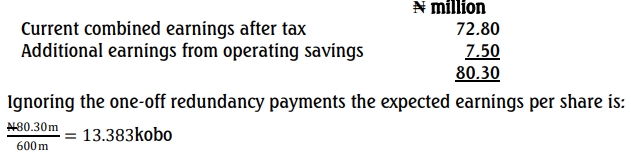

However, this ignores the impact of the redundancy costs, ₦7,000,000 after tax.

When this is included the combined value of the companies is still expected to substantially increase.

ii) Changes in expected cash flows as a result of the takeover are as follows:

If the market is efficient the market value of the combined company should increase by ₦55,500,000 as a result of the expected increase in NPV, much less than the estimate using P/E based valuation.

d. Limitations of Estimates:

- P/E ratios may not accurately capture post-acquisition integration issues.

- Cash flow assumptions assume perpetual savings without variability.

- Market sentiment and risk factors influencing share prices are not fully captured.

e. Strategic Implications of a Hostile Bid:

- Hostile Takeover: May lead to resistance from YP’s management, negatively impacting morale and integration efficiency. Risk of overpayment due to premium.

- Organic Growth: Although slower, it allows for strategic control and reduces the risks associated with forced integration. Organic growth can also maintain positive stakeholder relations and a stable corporate culture.