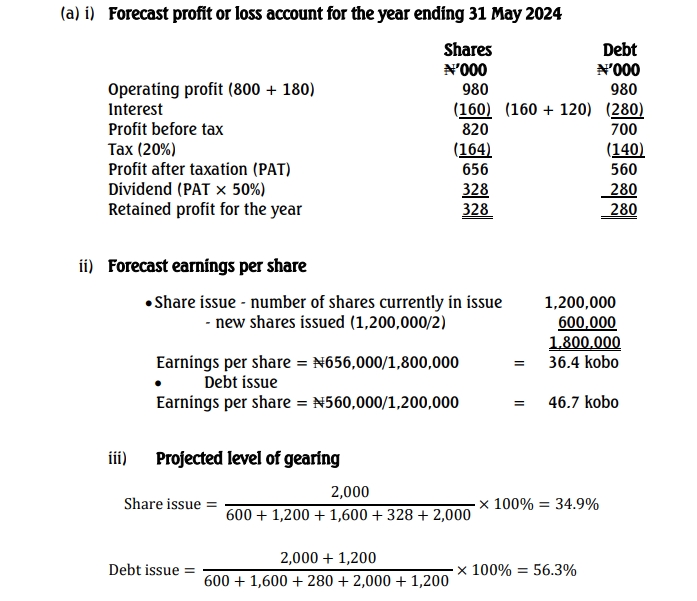

Question

Answer

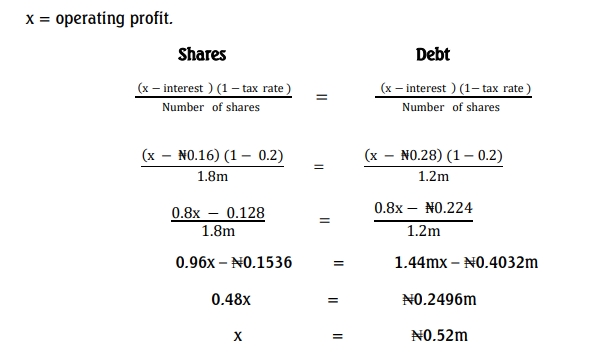

(b) Operating Profit for Equal EPS under Each Financing Option

To calculate the operating profit where EPS is the same for each option:

Let x represent the operating profit.

(c) Evaluation of Each Financing Option from the Shareholder’s Viewpoint

Impact on EPS:

The calculations in part (a) indicate that for existing shareholders, issuing debt would result in a higher earnings per share (EPS) than the share issuance, and it would also increase EPS above the current level of 42.7 kobo. This would enhance shareholder value in terms of profitability per share.

Impact on Risk:

The debt issuance would significantly raise the gearing level from the current 47.6%, increasing the financial risk for equity shareholders. This heightened risk due to the debt could be a concern, as it may affect the stability of earnings if financial obligations become burdensome. The shareholders’ tolerance for this additional risk should be evaluated.

Impact of Share Issuance:

Opting for a share issuance would lower the gearing level, reducing financial risk, but it would also dilute existing shareholders’ control as it increases share capital by 50%. A third of the new shareholding would belong to the supplier, who already holds equity, potentially altering the balance of ownership power. This dilution of control may be undesirable for current shareholders who prefer to retain their influence in the company.

(d) Factors Influencing Financing Decisions: Debt vs. Equity and Long-term vs. Short-term Debt

Equity vs. Debt Considerations

- Cost of Debt Capital:

Interest on debt is tax-deductible, reducing the effective cost of debt capital compared to equity. This tax advantage makes debt financing generally cheaper, often making it the preferred option. - Gearing Targets:

Companies typically aim to maintain gearing within a range considered acceptable by shareholders and lenders. Exceeding this range might be viewed negatively by the market and can lead to higher perceived risk. - Retained Profits Policy:

Companies with high retained profits may require less external financing, resulting in lower gearing levels. When retained earnings are sufficient, companies might avoid both debt and equity financing. - Management’s View on Interest Rates:

If market interest rates are high, management might avoid debt financing, particularly if borrowing at a variable rate. When interest rates are expected to rise, the company may opt for equity or delay financing.

Long-term vs. Short-term Debt Considerations

- Financing for Asset Types:

Traditionally, long-term assets should be financed by long-term debt, while short-term assets are financed by a mix of long-term and short-term sources. Financing illiquid assets with short-term debt could lead to insolvency if refinancing becomes difficult. - Transaction Costs:

Transaction costs vary by financing type; for example, arranging a medium-term bank loan is generally cheaper than a public issuance of loan stock. Short-term debt requires frequent refinancing, which increases recurring transaction costs. - Interest Rate Differences:

Long-term loans usually carry higher interest rates than short-term loans due to the greater risk over time. Market expectations of interest rate movements also influence these rates. - Ease of Raising Funds:

It is generally easier to secure short-term financing with lower security requirements compared to long-term financing, which may require substantial collateral. - Refinancing Risk:

With short-term debt, there is a risk that the company might not be able to refinance on favorable terms or may be unable to refinance at all when the debt matures. Long-term loans reduce this refinancing risk. - Flexibility and Early Repayment:

Short-term debt offers flexibility, allowing the company to adjust to interest rate changes. Long-term loans may have early repayment penalties, limiting the company’s ability to refinance if better financing options arise.