- 20 Marks

Question

Niko Plc, a large equity-financed company, has a year-end of December 31. It must fulfill a contract in Abuja and has two proposals to choose from: Proposal A (purchasing new machinery) and Proposal B (using existing machinery).

Proposal A:

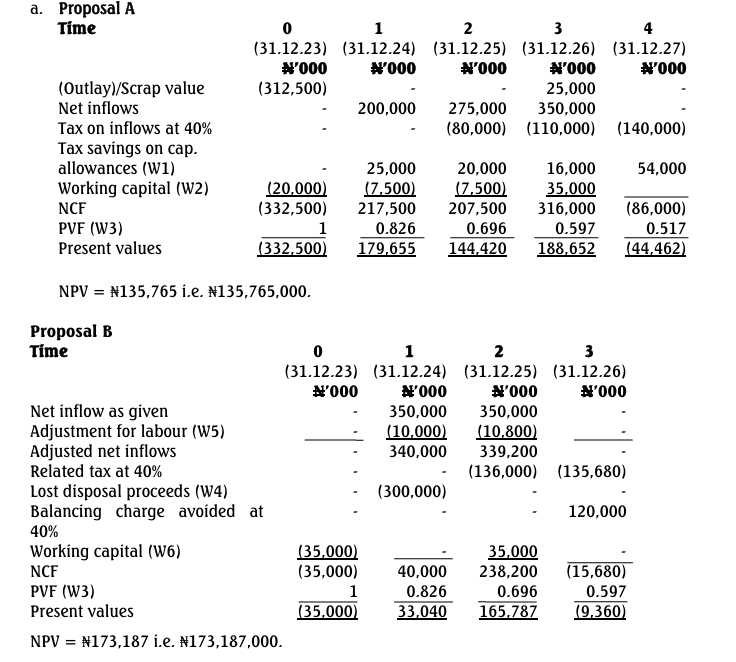

- Outlay of N312,500,000 on December 31, 2023, for new plant and machinery.

- Projected net cash inflows (before tax, in nominal terms):

- 2024: N200,000,000

- 2025: N275,000,000

- 2026: N350,000,000

- Scrap value: N25,000,000 at end of 2026.

Proposal B:

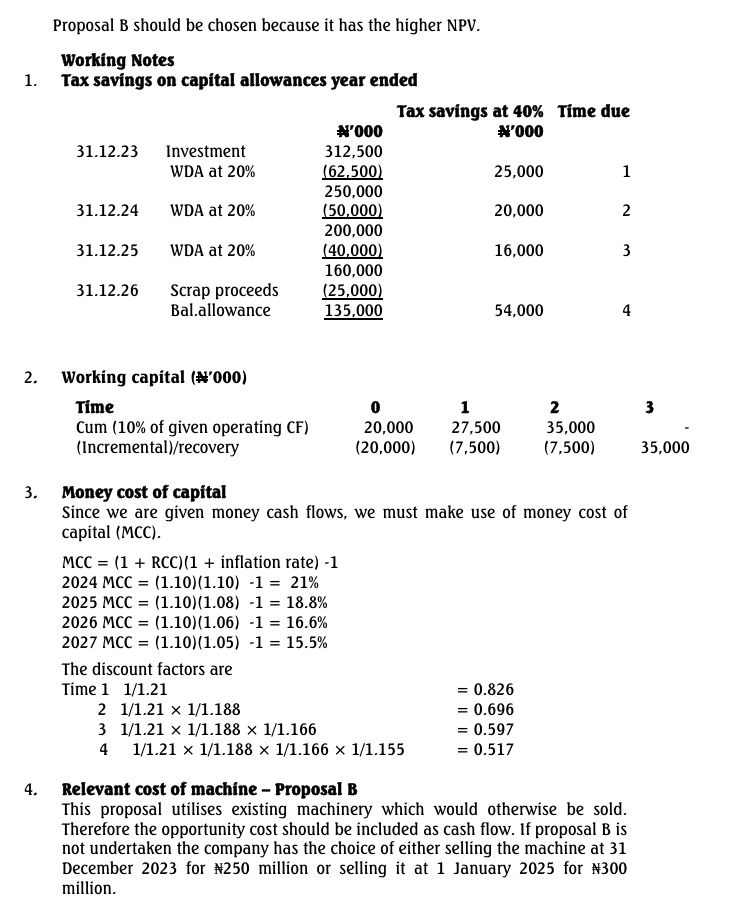

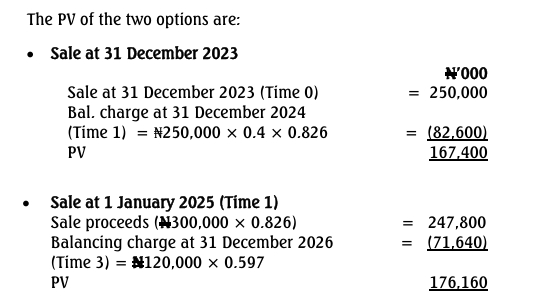

- Uses a machine with a net realizable value of N250 million, with an alternative sale value of N300 million on January 1, 2025, if unused.

- Cash inflows (in nominal terms):

- 2024: N350,000,000

- 2025: N350,000,000

- Labour costs:

- 2024: N100 million (replacement staff cost of N110 million)

- 2025: N108 million (replacement staff cost of N118.8 million)

- Machine residual value: N0 at project end in 2025.

Additional Details:

- Working capital: 10% of year-end cash inflows, released upon project completion.

- Expected annual inflation rates: 2024 – 10%, 2025 – 8%, 2026 – 6%, 2027 – 5%.

- Real cost of capital: 10%.

- Income tax: 40%, payable one year after the accounting period.

- Capital allowances: 20% reducing balance for Proposal A’s plant and machinery.

Required:

- a. Calculate the NPV at December 31, 2023, for each proposal. (17 Marks)

- b. State any reservations about making an investment decision based on these NPV figures. (3 Marks)

Answer:

Answer

- Tags: Capital Allowance, Cash Flow, Discount rate, Investment Appraisal, NPV, Project evaluation

- Level: Level 3

- Topic: Investment Appraisal Techniques

- Series: NOV 2023

- Uploader: Dotse