Question

Answer

a. As regards KutuKutu Plc, the bonus is not cash-settled due to the facts that:

- The performance bonus is to be paid in cash, but the bonus payment is unrelated to the movement in its share price.

Therefore, it must be mentioned that the transactions entered into in (1) do not meet the definition of equity-settled share-based payment transactions within the scope of IFRS 2.

b. According to IFRS 2, share-based payment transactions should be measured at the fair value of the goods or services received. If the fair value of goods and services cannot be measured reliably, then the entity should measure the transaction at the fair value of the equity instruments granted.

This transaction should be accounted for as an equity-settled share-based payment arrangement and falls within the scope of IFRS 2. The postings in the books of KutuKutu Plc will be as follows:

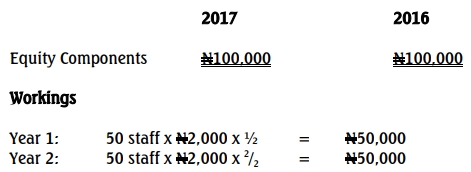

Kutukutu Plc

Statement of financial position as at December 31,

Assumptions:

No employees left the organization (Kutukutu Plc) during the two years in question. Fair value (FV) of each option (N250) is considered constant at the grant date (i.e. date of agreement between employees and Kutukutu Plc)