Question

Answer

Baba Tee & Co (Chartered Accountants)

Plot 5, Osara Road, Abeokuta

INTERNAL MEMO

Date: …….

From: Tax Manager

To: Managing Director

Subject: Computation of Hydrocarbon Tax and Companies Income Tax Liabilities Payable

I refer to your directive on the above subject and a draft report for your review and further action is hereby presented.

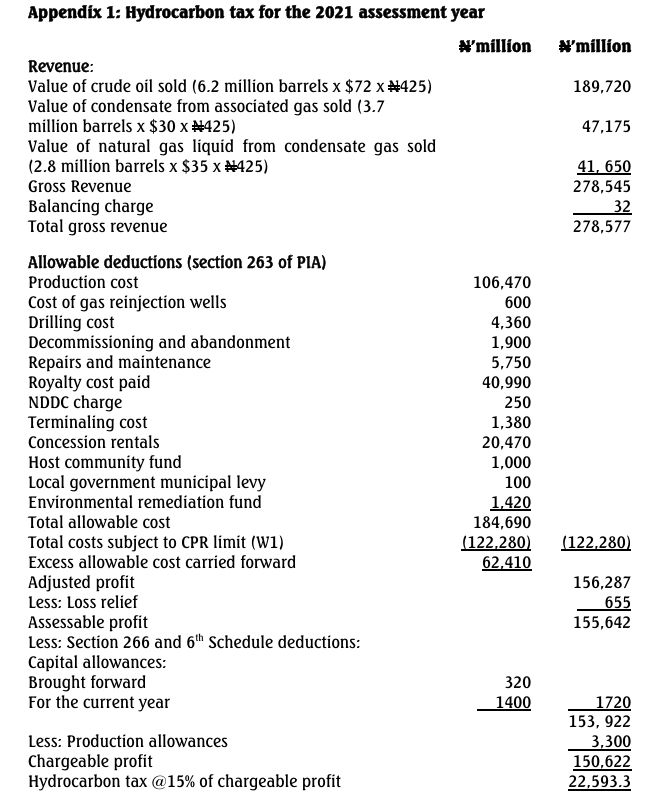

a. Determination of hydrocarbon tax liabilities for the 2021 assessment year

With losses relieved brought forward from last year and the grant of capital allowances and production allowances, the company made a chargeable profit of N150.622 billion. Hydrocarbon tax is at the rate of 15% of chargeable profit, which amounted to N22,593,300,000.

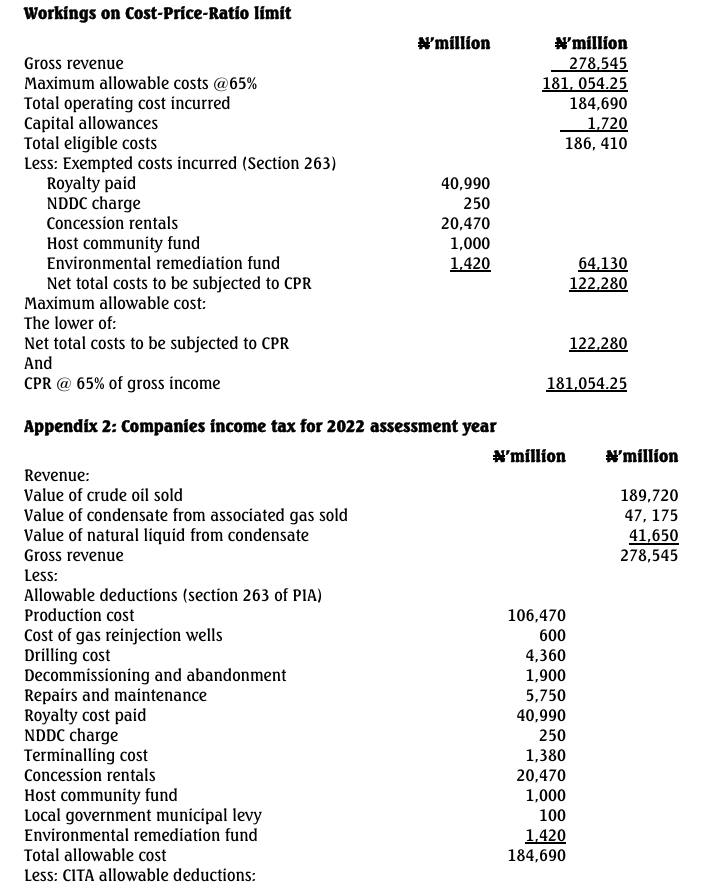

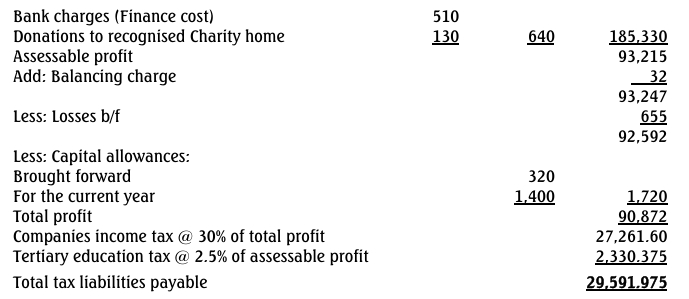

b. Determination of companies income tax liabilities for the 2022 assessment year

The company made a total profit of N90.872 billion. Companies income tax is 30% of total profit, which gives N27,261,600,000. The company is also to pay 2.5% of assessable profit as tertiary education tax (N2,330,375,000).

Thank you.

Tobby Babatolu