Question

Tayo Kayode (TK) is a highly successful beverage company listed on the Nigerian stock market. Its products are particularly attractive to the younger generation.

Eko Laboratory (EL) has developed an innovative synthetic, alcoholic beverage – the Younky.

It is believed that the product, if manufactured commercially, will be popular among the youths.

TK has been offered a license to produce the Younky on the condition that it commences production within the next twelve months. In the last board meeting, the Marketing Director, Kehinde Kay, presented the following preliminary evaluation of the project.

Kehinde recommended that the project should thus be rejected.

However, the Finance Director (FD), Ben Okon, argued that conventional NPV analysis undervalues projects with high uncertainty as the value of embedded real options is often ignored. He suggested that the possibility of delaying the project for up to twelve months effectively gives TK a call option on development and that if market forecasts improve over the next year, then the company can benefit. To get the ‘right answer,’ he concluded, option values must be incorporated.

The current long-term government bond yield is 5%. The expected standard deviation of future cash flows is estimated to be 35%.

Required:

a. Comment on the views of the Marketing and Finance Directors. (5 Marks)

b. Using the Black-Scholes option pricing model for a European call option, estimate the value of the option to commercially develop and market the Younky. Provide a recommendation as to whether or not TK should manufacture the Younky. (10 Marks)

c. Comment on modeling the possibility of delay as a European call option. (5 Marks)

(Total 20 Marks)

Answer

a. Comment on the Views of the Marketing and Finance Directors:

The Marketing Director, Kehinde Kay, is correct in their interpretation of the calculated NPV. The NPV can normally be interpreted as showing the impact of a project on shareholder wealth, so a negative NPV would indicate that the investment would erode shareholder value and should thus be rejected.

The Finance Director, Ben Okon, is also correct in pointing out a weakness of conventional NPV analysis. High uncertainty is usually reflected in a higher discount rate, and conventional NPV does not consider the value of management flexibility, such as the ability to delay or abandon a project. The option to delay the investment provides value, particularly if market conditions improve, and real option valuation can better reflect this scenario.

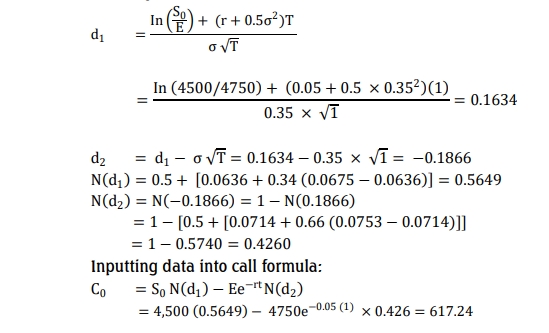

b. Valuation Using Black-Scholes Model:

Inputs for Black-Scholes Model:

- S0 (Present Value of Future Cash Flows): ₦4,500 million

- X (Exercise Price): ₦4,750 million (investment cost of ₦250 million plus a target return of 5%)

- r (Risk-Free Rate): 5%

- σ (Standard Deviation): 35%

- T (Time to Expiration): 1 year

Recommendation: The high value of the call option suggests that the offer to produce Younky should be accepted. By delaying the decision and incorporating the real option value, TK can capitalize on potential improvements in market conditions.

c. Modeling the Possibility of Delay as a European Call Option:

The Black-Scholes model was developed for European options, where the option can only be exercised at maturity. In this case, production could commence at any time during the 1-year period, making the option an American option rather than a European option.

However, where no dividend is payable and time value remains, it is often worthwhile holding an American option to expiry, making the valuation as a European call option still valid. In this context, the valuation as a European call provides a lower limit on the value of the option to delay investment.