Question

Answer

a. Double Taxation Relief Explanation:

Double Taxation Relief is a mechanism designed to prevent the same income from being taxed twice in different jurisdictions. When a company or individual earns income in one country but is a resident of another, they might be liable for taxes in both countries. Double Taxation Relief, usually established through Double Taxation Agreements (DTAs) between countries, allows the taxpayer to claim a tax credit in one country for the taxes paid in the other. This credit reduces the overall tax burden, encouraging cross-border trade and investment.

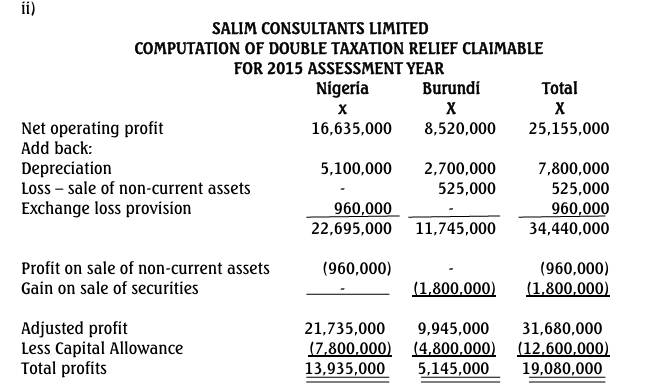

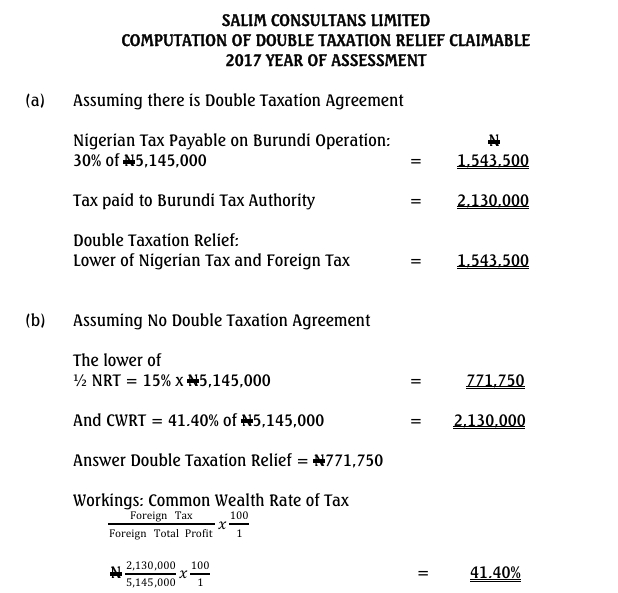

b. Computation of Double Tax Credit:

To compute the Double Tax Credit claimable by the company with a Double Taxation Agreement (DTA) with Burundi, we would apply the following steps based on the income earned and taxes paid in each jurisdiction:

- Determine Taxable Income: Calculate the taxable income that is subject to taxation in both countries.

- Identify Tax Rates: Note the tax rate applied in the resident country (e.g., home country) and the foreign country (Burundi in this case).

- Compute Tax Paid Abroad: Multiply the income earned in Burundi by the Burundi tax rate to get the tax paid in Burundi.

- Compute Tax Liability in Home Country: Calculate the tax liability on the same income in the home country by applying the home country’s tax rate to the taxable income from Burundi.

- Apply the Lower of the Taxes Paid: The Double Tax Credit allowed would typically be the lower of the actual tax paid in Burundi or the tax liability calculated for the same income in the home country.