Question

Answer

Scenario I: Revenue Recognition for Consultancy Contract

For revenue to be recognized, the following criteria must be satisfied:

- The entity has transferred to the buyer the significant risks and rewards of ownership.

- The revenue amount can be measured reliably.

- The incurred cost can be measured reliably.

- The transaction’s stage of completion at the reporting date can be measured reliably.

Since these criteria are not met for the consultancy contract, the full amount of ₦1,000,000 should be recognized as liability or non-current liability rather than as revenue.

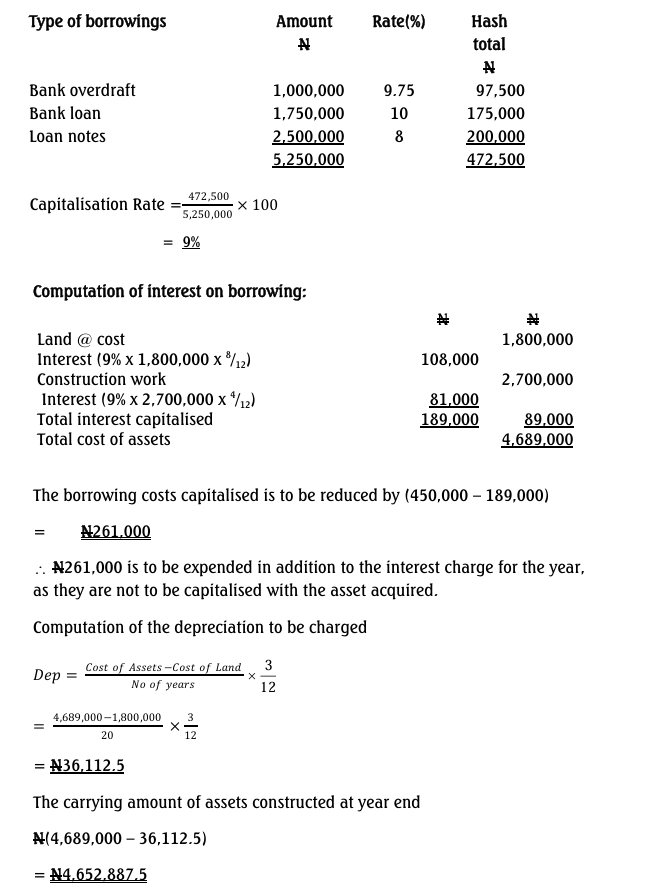

Scenario II: Borrowing Costs for Factory Construction

Borrowing costs directly attributable to constructing an asset requiring an extended period to become operational should be capitalized as part of the asset’s cost. For general borrowings, the capitalization amount is based on the weighted average cost of borrowing.

- Capitalization Rate Calculation:

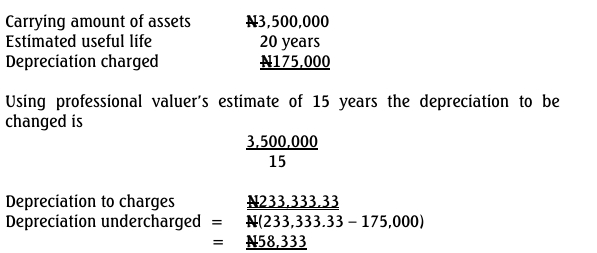

Scenario III: Depreciation of Blast Furnace

The depreciation of the blast furnace was based on a 20-year useful life, contrary to a report by a qualified expert recommending 15 years.

- Depreciation Calculation Based on Valuer’s Estimate

Revised Financial Statements

Statement of Profit or Loss Extract for the Year Ended December 31, 2014:

| Item | ₦’000 |

|---|---|

| Profit Before Tax | 2,500 |

| Less: Consultancy Agreement | (1,000) |

| Overcapitalized Interest | (261) |

| Undercharged Depreciation | (58.33) |

| Revised Profit | 2,180.67 |

Statement of Financial Position as of December 31, 2014:

| Item | Adjustment (₦’000) | Revised Amount (₦’000) |

|---|---|---|

| Property, Plant, Equipment | (319.33) | 11,680.67 |

| Current Assets | – | 3,500 |

| Total Assets | – | 15,181 |

| Share Capital | – | 2,000 |

| Retained Earnings | (1,319.33) | 4,680.67 |

| Equity | – | 6,681 |

| Non-Current Liabilities | 500 | 5,500 |

| Current Liabilities | 500 | 3,000 |

| Total Equity and Liabilities | – | 15,181 |

Ethical Issues

The following are ethical concerns:

- Pressure on the previous Financial Controller to compute depreciation with an extended useful life, possibly leading to the resignation.

- The Managing Director’s pressure to present favorable financial statements for a potential stock listing.

- Threats regarding the Financial Controller’s future for non-compliance.

Possible Courses of Action for Financial Controller:

- Discuss compliance with IFRS standards with the MD.

- Emphasize adherence to professional ethical standards.

- Consider consulting with other directors or the audit committee.

- As a last recourse, resign to maintain professional integrity.