Question

Answer

a. Revenue Recognition Principles:

- Stage of Completion Method: This method recognizes revenue as the contract progresses, based on the percentage of completion. The method is appropriate when the outcome of a contract can be reliably measured.

- Cost Recovery Method: This method recognizes revenue only to the extent that recoverable costs are incurred. It is used when the outcome of the contract cannot be measured reliably.

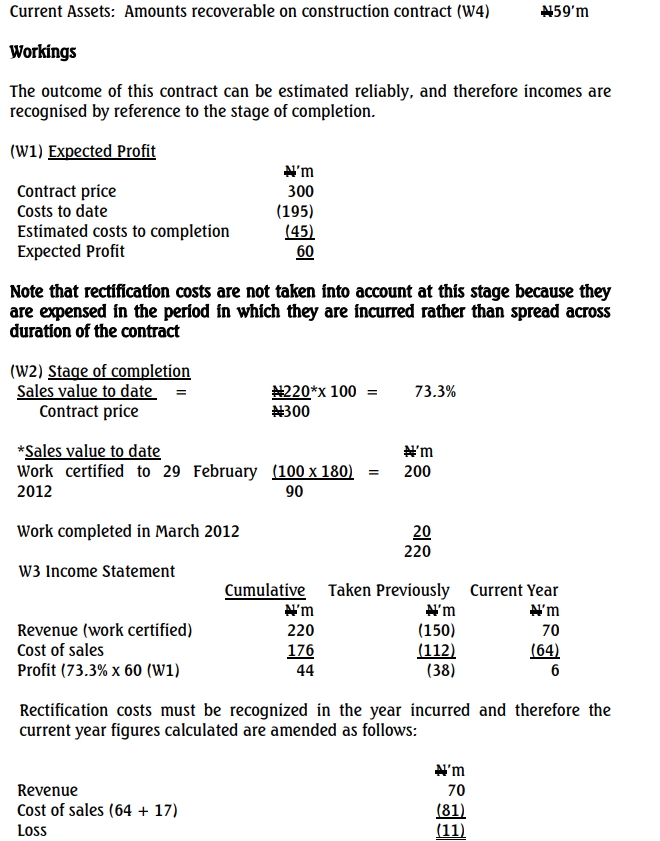

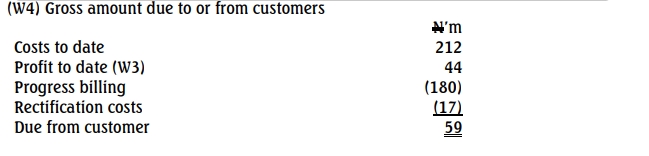

b. Extracts from Financial Statements:

Income Statement: Revenue: N70 million

Cost of Sales: N81 million

Gross Loss: N11 million

Statement of Financial Position of Real Construction Company Plc. for the year ended 31 March 2012.