Question

Answer

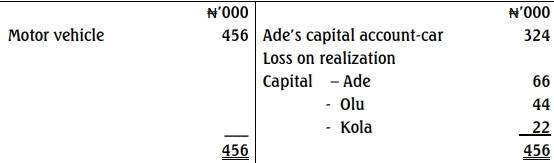

Realisation Account

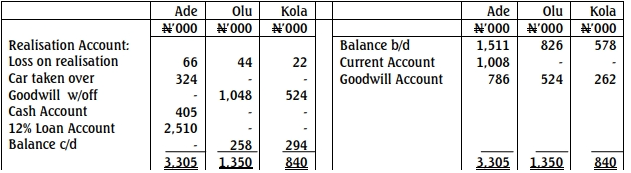

Partners‟ Capital Accounts

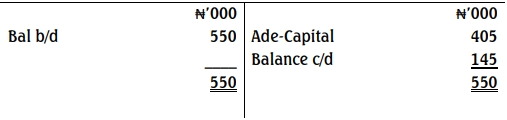

Cash Account

12% Loan Account

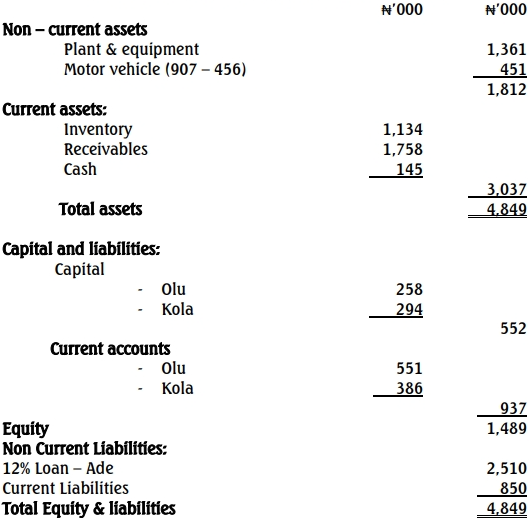

Olu and Ade

Statement of financial position as at April 1, 2016

Realisation Account

Partners‟ Capital Accounts

Cash Account

12% Loan Account

Olu and Ade

Statement of financial position as at April 1, 2016